The oil and natural gas midstream industry is filled with high yields. But not all high yields are created equal, as the 40% distribution cut at Enbridge Energy Partners in 2017 and the 75% dividend cut at Kinder Morgan Inc in 2016 show. Here's why the high yields at Enterprise Products Partners L.P. (EPD 0.05%), Magellan Midstream Partners, L.P. (MMP +0.00%), and ONEOK, Inc. (OKE +0.47%) are here to stay.

1. A conservative giant

Enterprise is one of the largest and most diversified midstream companies in the industry. It has a 20-year history of increasing its distribution annually. The rate of increase has averaged around 5% a year over time, which is probably all you should expect in the future at this slow and steady payer. Its yield is an eye-catching 6.4% -- the highest of this trio.

Image source: Getty Images.

To support that distribution growth in the future, Enterprise has around $9 billion in growth projects lined up. It also has a penchant for acquisitions -- it's completed $26 billion worth of acquisitions since its IPO in 1998 (that's over and above the $38 billion it's spent on organic growth projects). In fact, it used the energy downturn that started in mid-2014 to opportunistically buy three companies, spending roughly $8 billion.

And it has a strong financial foundation backing its largely fee-based business. For example, even during the worst of the oil downturn Enterprise managed to keep growing distributable cash flow and maintain distribution coverage of at least 1.2 times. This high-yielding industry giant is basically a tortoise, but there's no reason to worry about its distribution.

2. Yield with growth potential

Magellan Midstream partners is about a third the size of Enterprise. Its yield, at roughly 5%, is also smaller. However, it's managed to grow its distribution at a roughly 11% annualized clip over the past decade -- around twice as fast as Enterprise. Magellan's annual streak of increases is up to 17 years.

Magellan has roughly $1 billion in growth projects on the books to keep that growth streak alive. It has another $500 million worth of projects in the wings. And, like Enterprise, Magellan is eager when it comes to acquisitions. The difference, however, is that Magellan's smaller size allows it to consider more modest deals that wouldn't be on Enterprise's radar. Its relatively small size is an advantage in that regard.

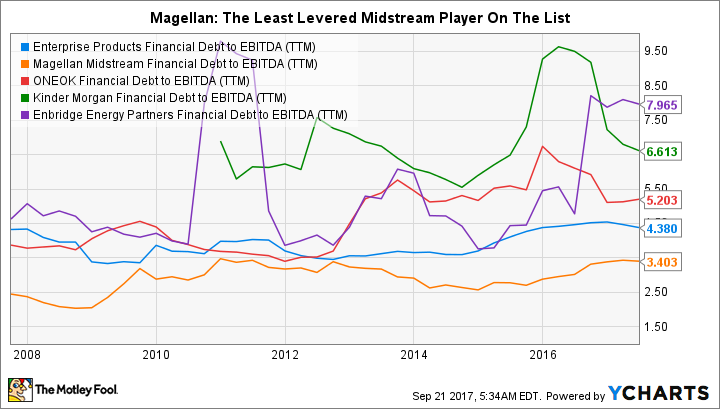

EPD Financial Debt to EBITDA (TTM) data by YCharts.

One more important differentiator here is that Magellan is even more conservative than Enterprise, with a debt-to-EBITDA ratio of roughly 3.4 compared to Enterprise's roughly 4.4. Lower leverage allows more cash to flow through to unitholders and helps support the partnership's higher distribution growth rate. It also provides a solid foundation for the continued growth of the partnership's largely fee-based business. Distribution coverage, meanwhile, is roughly 1.2 times, providing an ample margin of safety.

3. A giant going through a transformation

ONEOK is a slightly different story. It offers up a 5.3% yield backed by 15 years of consecutive annual dividend hikes. The dividend growth rate over the past 10 years was an annualized 16.5%. That's impressive, but this is where things start to get a little interesting at this $21 billion market cap midstream player. As of July, the dividend had only been increased 1.2% over the trailing 12 months, a big drop in the growth rate. But don't write the company off; there's been a lot going on.

The biggest news was the company's acquisition of ONEOK Midstream Partners in late June. That gives it total control of its assets and is expected to help ONEOK reduce its debt load (the goal is to move its debt-to-EBITDA levels below 4, closer to those of Magellan). Bringing the partnership in-house will also lower ONEOK's cost of capital, which will help the company grow its business in the future. And, as promised, ONEOK upped its dividend by a massive 21% in August, following the completion of the deal.

OKE Financial Debt to EBITDA (TTM) data by YCharts.

Right now ONEOK is probably a riskier play than the other two midstream companies here because of all of the moving parts. But it's making these changes to become a much more boring company. With dividend coverage of roughly 1.2 times, in line with both Enterprise and Magellan, there's no particular reason to worry about the payout. If you are interested in a mix of yield and dividend growth, ONEOK is worth a deep dive.

Yields you can count on

All three of the midstream players here have long histories of rewarding investors with regular annual distribution increases. Enterprise is a giant with plans to continue its slow and steady growth. Magellan, meanwhile, is smaller and more financially conservativ but has rewarded investors with a higher distribution growth rate. ONOEK is a little different in that it's made a notable strategic shift in its business. But if you take the time to understand what's going on, it looks like the move was a good call. At this point, I think the high yields offered by this trio are not only here to stay, but the distributions are likely to keep growing, as well.