It might seem like the number of Americans who claim to be vegetarians has grown dramatically in the past decade, but it hasn't. It's only 5%, and that number hasn't changed since 2012.

But the amount of meat consumed -- especially beef -- is on the decline. That should be good news for plant-based meat brands like Beyond Meat (BYND 0.95%). Yet its stock has been in free fall, and Wall Street seems convinced there's more pain ahead.

Image source: Getty Images.

So much for a fast start

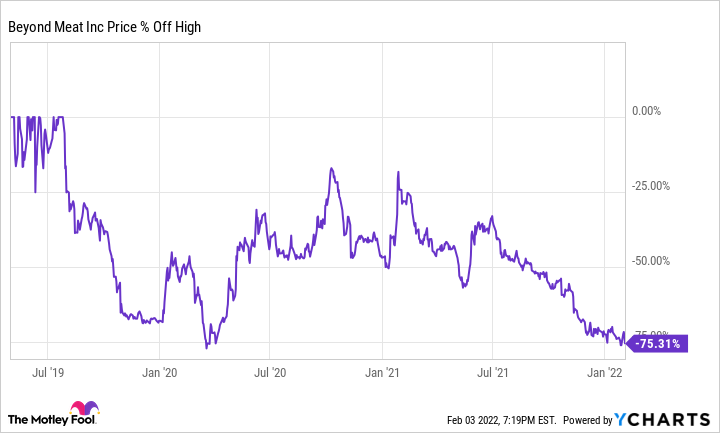

Beyond Meat went public in May 2019. Shares rose 163% on the first day as the company raised capital to increase capacity and expand its product offerings. The number of global outlets selling the product has increased more than 300% since then, but the stock is down 75% from those early days.

Many are expecting the struggles to continue

Despite the huge drawdown since Beyond Meat's initial public offering (IPO), Wall Street is expecting even more pain to come. Short interest has been climbing almost from day one. Currently, an astounding 38% of the float -- shares available to trade publicly -- are sold short. That percentage is twice as high as AMC Entertainment and Gamestop -- two stocks that nearly everyone believes will trade much lower at some point in the future.

BYND Percent of Float Short data by YCharts.

Part of the drop is just where it started. Food is a low-margin business -- Beyond Meat's gross margins are 27% -- and it has negative cash flow from operations. When it came public, the stock traded at more than 60 times sales. That would be rich for a fast-growing software company.

The high-profile wins keep coming

There's a lot of competition in the space. Kellogg's Morningstar Farms brand is the leader in the category with 30% share, according to analytics firm 1010data. However, Beyond Meat is gaining. The latest earnings presentation showed a slight gain in market share over the past year.

Despite Dunkin' Donuts taking their Beyond Sausage sandwich off the menu, Panda Express, Pizza Hut, and fast-food giant McDonald's are expanding their pilots. The product is also in most major grocers including Walmart, Costco, and Whole Foods Market.

Should investors take a bite?

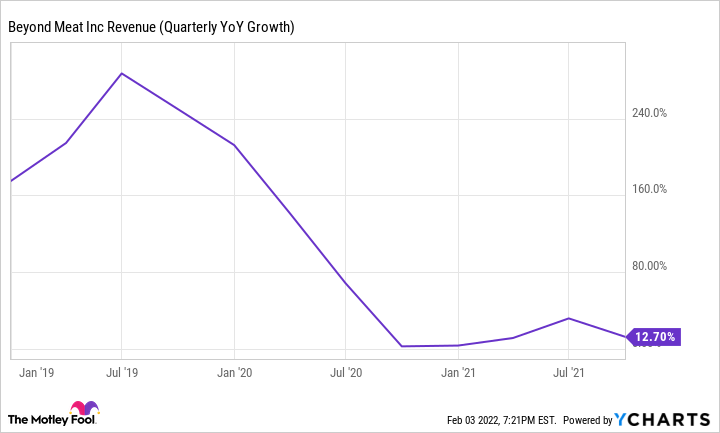

Being in grocery stores was great during the pandemic; grocery sales surged as restaurants were closed. And being distributed in the country's largest stores meant Beyond Meat's sales were surging, too. Now, a year later, the comparisons are difficult as fewer people are eating at home. It's led to a steep drop in year-over-year growth.

BYND Revenue (Quarterly YoY Growth) data by YCharts.

Investors are now asking themselves if the plant-based craze is over or if sales will ramp up again as the worst of the pandemic fades into the rearview mirror. Although no one knows what the future holds, the forecast for long-term growth has been cloudy the last two years. However, looking back to 2019 can help clear it up.

Comparing the first three quarters of 2021 to those of 2019 shows revenue compounding at 35% annually. That's in line with what analysts are expecting in 2022, and it's an impressive number. It just isn't enough to whet my appetite for a low-margin business with negative operating cash flow.

Beyond Meat might be a successful product and find its way into a lot of consumers' stomachs. But shares would have to trade much lower for me to nibble on them.