The market has gone cold on growth stocks. With high inflation, looming interest rate hikes, Russia's invasion of Ukraine, and other factors creating turbulence, the appetite for risk has changed. Investors want earnings, they want them now, and this has led to a marketwide reappraisal of how software stocks are valued.

While focusing on profitable, predictable businesses trading at low price-to-earnings multiples will make your portfolio sturdier when the market is turbulent, volatility and uncertainty have also historically created some great opportunities to buy top-tier growth stocks. I recently initiated a position in Unity Software (U -2.20%) and believe the stock is primed to be a huge long-term winner. Here's why.

Image source: Getty Images.

Unity has multiple ways to win

With the last specific figures it provided, Unity reported in the fourth quarter of 2020 that 71% of the top 1,000 games in the mobile market were made using its software. The company has also said that more than two-thirds of all virtual reality (VR) and augmented reality (AR) content is made with Unity. With its full-year update for 2021, management reported that the business had increased market share in each of these core categories.

In addition to gaming and metaverse-related applications, Unity also sees growth opportunities in industries including architecture, automotive, and film. Thanks to acquisitions of cloud-based collaboration platforms and visual-effects companies including Weta Digital, Unity is rapidly branching into new content-creation services and says it aims to "democratize access to some of artistry's most exclusive tools and services via the cloud."

To put this opportunity in perspective, think of what Adobe (current market cap: roughly $197 billion) has accomplished with Photoshop, After Effects, Illustrator, and other subscription-based software.

With Unity's market cap having been pushed back down to roughly $23 billion, the company has also been made more attractive as a potential acquisition target. Meta Platforms CEO Mark Zuckerberg is said to have eyed Unity as a potential acquisition target, and Microsoft's $68.7 billion move to buy Activision Blizzard underscores the fact that gaming and metaverse-focused companies are hot targets at present.

My guess, and preference, would be that Unity remains an individual entity through at least the next five years, but it also wouldn't be shocking to see a Big Tech player with big metaverse ambitions buy the company up at a substantial premium.

Shares look expensive -- and cheap

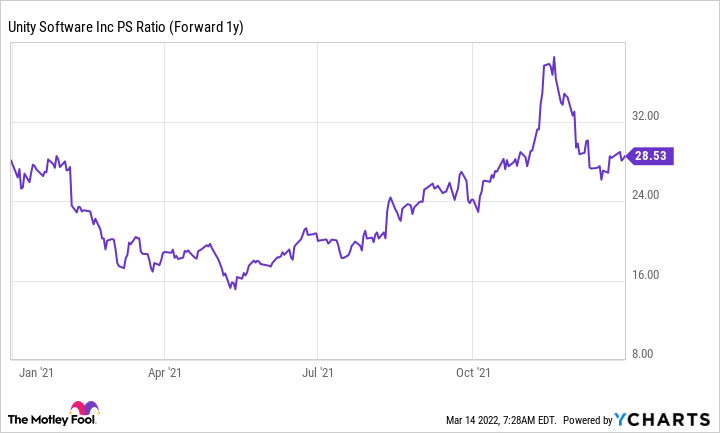

Even after a dramatic stock price pullback, Unity trades at roughly 15 times this year's expected sales. In the current market climate, an unprofitable software stock being valued at that kind of forward-sales multiple may strike some investors as obscene.

However, if someone offered to sell you Unity stock at less than 16 times 2022's expected sales at nearly any time since the beginning of 2021, that would have looked cheap based on the standards of the market at the time.

U P/S ratio (forward 1 year). Data by YCharts.

At its peak, Unity Software was valued at roughly 38 times 2022's expected sales. To put the extent of the recent sentiment shift in perspective, Unity stock now trades down roughly 62% from the lifetime high it hit in November 2021. While a big pullback from a lifetime high isn't necessarily a strong buy indicator in its own right, there are other good reasons to think that the software company's shares offer attractive return potential at current prices.

Unity Software stock is now up just 15% since market close on the day of its initial public offering despite posting very impressive business performance across the stretch and significantly outperforming the market's growth targets. Shortly after the company's IPO, the average analyst estimate was targeting revenue of roughly $1.2 billion for 2022. Today, the company's midpoint guidance calls for revenue of $1.495 billion this year, up about 25% from the early initial analyst target range.

The company's midpoint estimate calls for sales growth of 35% this year, which looks pretty good considering the business is following up explosive expansion over the last two years. Unity Software closed out 2021 with a gross margin of 77.7%, annual sales growth of 44%, and a dollar-based net revenue retention rate of 140%. So, while the company is currently posting substantial losses, it has promising avenues to deliver big earnings down the line as it brings new customers on board, boosts spending from existing clients, and has the flexibility to reduce spending on research and development, sales and marketing, and other expenses as a percentage of overall sales.

Weighing the risks and potential rewards

While I'm very bullish on Unity's long-term prospects, I didn't buy the stock without consideration for the bear case. The company has a commanding leadership position in game-engine services and other offerings for mobile, AR, and VR applications, but that doesn't mean it will be immune to competitive pressures down the line.

The Unreal Engine from Epic Games is currently the market-leading offering for graphically-intensive games in the console and PC space, and it's possible that the company will devote more resources to growing its position in mobile, VR, and AR and curb Unity's growth opportunities in those categories. Microsoft's acquisition of Activision Blizzard could also lead to the development of its own commercial development-engine services for gaming and metaverse applications, and it's within the realm of possibility that other gaming and Big Tech companies could muscle in on Unity's turf.

It's also worth noting that Unity has been relying heavily on stock-based compensation to pay employees. This will likely continue be the case in the near future, so investors should approach an investment in the company with the understanding that there are going to be dilutive effects as the software specialist issues new shares to fund its operations.

So, in addition to the possibility that the market will continue shifting toward assigning lower price-to-sales multiples to software stocks in the near term, there are other meaningful risks for investors to consider. Unity is still a highly growth-dependent stock, but this is a case where the words of famous value investor Benjamin Graham seem resonant: "In the short run, the market is a voting machine, but in the long run, it is a weighing machine." Software stocks are out of favor right now, but I think the long-term weighing will reward investors who buy Unity at current prices.