The semiconductor industry has generally not been known for offering great dividend stocks. Although chip designers such as Nvidia have offered a modest payout, such stocks tend to draw more attention from growth investors.

However, both Texas Instruments (TI) (TXN 1.27%) and Broadcom (AVGO 3.84%) have built long track records of annual, double-digit payout hikes. And while both companies have served investors well over the last few years, one appears to have fared significantly better in a head-to-head matchup.

Image source: Getty Images.

How the companies compare

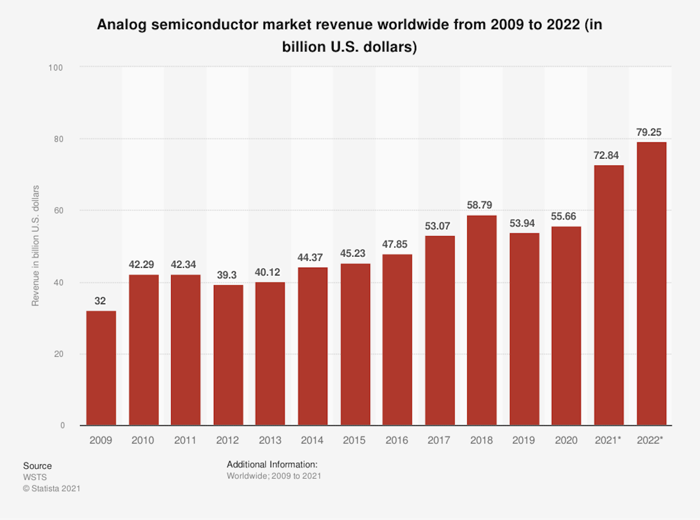

Consumers may know TI best for its calculators. Nonetheless, it leads the analog semiconductor market, making over 80,000 products for more than 100,000 customers. These customers use TI products for applications in industrial, automotive, personal electronics, and many other areas. Additionally, the analog chip market continues to benefit from a long-term growth trend that should keep TI well-positioned within its industry.

Source: WSTS.

Like TI, Broadcom also builds chips for business clients. It spends heavily on research and employs engineers near its most prominent clients to develop products that resolve these customer issues. It has also diversified into the enterprise software business. This software helps enterprises improve their efficiency and secure their networks.

TI has traded on the markets since 1953. While Broadcom claims 50 years of innovation, it only began trading in its current form in August 2009. Since that time, the total returns of both companies outpaced the S&P 500. Still, Broadcom has consistently outperformed TI and has grown to a larger market cap, surpassing $260 billion compared to TI's $175 billion.

TXN Total Return Level data by YCharts.

Additionally, the trend is on track to continue. Analysts believe Broadcom will increase its earnings by 27% this year, well ahead of TI's projected 10% increase.

A closer look at the dividends

Nonetheless, TI has a more extended history, and that also applies to dividends. It paid its first dividend in 1962, but the nature of the dividend changed in 2004 when the company's board began to offer substantial annual increases. Between 2004 and 2021, the dividend grew at a compound annual growth rate (CAGR) of 25%. From a level of just $0.089 per share in 2004, TI's payout has risen to $4.60 per share annually, yielding about 2.5% at current prices.

The company has also built an 18-year track record of annual payout hikes. If TI maintains this record for seven more years, it could achieve Dividend Aristocrat status. And despite the considerable increases, the company can probably continue the double-digit payout hikes. The $6.3 billion it generated in free cash flow in 2021 grew 15% year over year. This kept free cash flow ahead of the $3.9 billion in dividend costs, which amounts to about 62% of free cash flow.

Broadcom began paying dividends in 2010, the year after its IPO. Then known as Avago Technologies, it paid only $0.07 per share that year. However, its payout rose every quarter for almost six years until the company switched to yearly increases in 2016. Today, Broadcom pays its shareholders $16.40 per share annually, an approximate 2.6% yield.

At 11 years, the record of increases has not persisted as long as TI. Still, the quarterly payout has risen 59-fold during that time, beating the 52-fold rise in TI's payout since 2004. Broadcom also generated $13.3 billion in free cash flow in 2021, 15% more than in 2020. Its dividend cost $6.2 billion, about 47% of its free cash flow. This means that the payout hikes can probably continue. It also shows that Broadcom has produced a faster-growth dividend at a comparatively lower cost to its cash flows.

TI vs. Broadcom

In a sense, investors in either company made good choices. Both semiconductor companies outperformed the indexes in terms of both dividends and stock price returns. Nonetheless, considering that Broadcom has delivered a five times higher total return since its IPO, Broadcom looks more like a screaming buy for both income and growth investors.