GE Aerospace (GE 1.32%) stock has performed exceptionally well since becoming a separate company. A Barclays analyst recently set a $175 price target and an "overweight" rating on the stock, indicating a nearly 19% upside over the next 12 months.

The bullish case for GE Aerospace

The analyst is optimistic about GE Aerospace's long-term profit growth and cash generation potential. The aircraft engine business model involves initially selling engines at a loss, followed by decades of lucrative aftermarket revenue, particularly through customized service agreements (CSAs). It takes time before engines are utilized enough to need servicing and overhauling. As such, there can be periods where aggressively ramping engine production leads to margin pressures while aftermarket revenue from legacy engines starts to slow.

That's why CEO Larry Culp told investors that the guidance for operating profit of $6 billion to $6.5 billion in 2024 "implies flat margins year-over-year, given the growth in LEAP, initial 9X shipments for the 777X platform, and other growth investments." The LEAP engine is the sole engine option on the Boeing 737 MAX, the Comac C919, and one of two options on the Airbus A320 neo family.

The good news is that new engines mean new aftermarket revenue down the line, and the Barclays analyst sees substantial opportunity for margin expansion in the future as lucrative aftermarket revenue kicks in.

I agree with the assessment and point out two things. First, every new engine delivered (GE plans to ramp LEAP deliveries by 20%-25% in 2024 after a 38% increase in 2023) is negative for near-term profit margins, but it builds long-term value. As such, negative engine margin pressure should be welcomed.

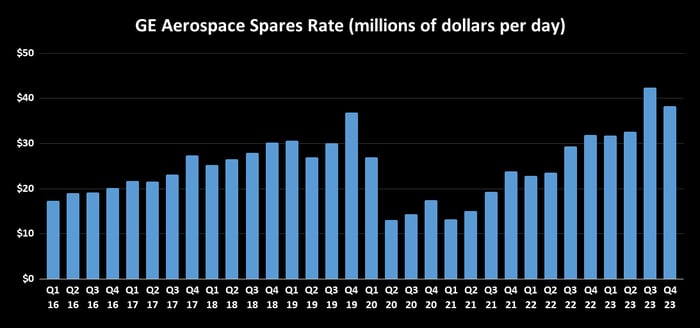

Second, GE Aerospace continues to generate strong growth in its spares rate sales.

Data source: GE Aerospace presentations. Chart by author.

Ongoing growth in spares sales will help offset the margin pressure from more engine deliveries in 2024. When LEAP aftermarket sales start to kick in in a few years, at the same time as engine deliveries begin to slow, there's likely to be a substantive margin expansion opportunity.