Shares of Lowe's (NYSE: LOW) recently hit a 52-week high. Let's look at how it got here and whether clear skies are ahead.

How it got here

A slow improvement in the economy and the housing market has helped push home improvement stores higher this year as financial results have improved. For Lowe's, revenue grew 11% in the most recent quarter, helping drive earnings per share 24% higher, a vast improvement from when we were in the depths of the recession.

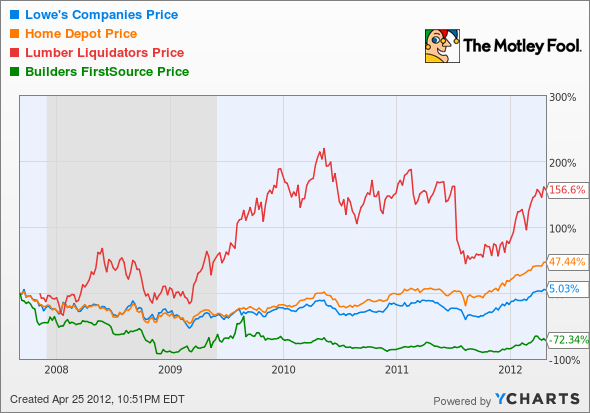

The recent results have been good, but when we take a step back, the performance isn't quite as impressive. Lowe's took a big hit during the recession, like every company tied to housing, and the stock is only up 5% in the past five years. It lags behind Lumber Liquidators (NYSE: LL) and Home Depot (NYSE: HD) in the home improvement space. The company has only outperformed Builders FirstSource (Nasdaq: BLDR) in the comparison below because the new construction market still hasn't picked up yet.

So Lowe's 52-week high is really recovering from a low rather than entering uncharted territory. One of the reasons Lowe's hasn't kept up with competitors over a longer time frame is the return it gets on its investment.

|

Company |

Return on Assets |

Return on Equity |

Operating Margin |

Forward P/E Ratio |

|---|---|---|---|---|

| Lowe's | 7.0% | 10.6% | 7.5% | 14.0 |

| Home Depot | 10.3% | 21.1% | 9.5% | 15.9 |

| Lumber Liquidators | 10.0% | 13.3% | 6.3% | 18.5 |

| Builders FirstSource | (3.6%) | (56.4%) | (3.1%) | N/A |

Source: Yahoo! Finance.

The lower return on assets is particularly concerning when Home Depot and Lumber Liquidators have higher returns.

What's next?

As the economy continues to improve and the housing market picks up, I think Lowe's will continue to profit and should continue to hit new highs. With that said, there are better values in the space, such as Home Depot, which has a better return on assets and equity than Lowe's.

The CAPS community also thinks that Lowe's can outperform the market, giving the stock a four-star rating. I would feel comfortable in the stock because its valuation is fairly low, but I would focus my home improvement dollars on Home Depot because of its better returns.

Interested in reading more about Lowe's? Click here to add it to My Watchlist, and My Watchlist will find all of our Foolish analysis on this stock.