Source: PACCAR.

PACCAR (PCAR -0.98%), one of the largest makers of heavy-duty trucks in the world, reported its fourth-quarter and 2014 full-year financial results on Jan. 30, exceeding analyst expectations across the board. Here are the highlights:

- Record revenue of $18.99 billion -- a 9.4% increase from the year before

- Earnings per share of $3.82 -- up 16% from the year before

- Paid out $1.86 per share in dividends in 2014; 73 straight years of paying a dividend.

Let's take a closer look at the details.

Sales by region

Class 8 retail truck sales reached 250,000 units in 2014, the most since 2006 and a big rebound from years of terrible results following the 2008 financial meltdown. PACCAR's market share for 2014 sales was nearly 28%, an indicator of the strength in the Peterbilt and Kenworth brands.

Furthermore, PACCAR's MX-13 engine is beginning to grow in popularity in North America, and was sold with 37% of Peterbilt and Kenworth trucks delivered in the fourth quarter. This bodes well as a boost to PACCAR's profitability if the company can continue to grow sales of its own engine.

PACCAR's DAF brand has a commanding market share in Europe, with some 13.8% in 2014. South American sales are growing, with 3,600 trucks sold in the continent in 2014, a 37% year-over-year increase.

Sales in 2015 face challenges

There is some potential concern for Europe and South America heading into 2015: Total trucks sold in Europe were 227,000, but the forecast for 2015 ranges from a low of 200,000 to a high of 240,000. At this point, Europe's poor economy has created some uncertainty around sales for the year. South American sales look destined to fall, with the high end of the forecast only representing an increase of less than 1%, and the low end representing a 15% decline.

PACCAR's best bet to grow in South America and Europe in 2015 is by increasing market share. The company is growing its dealer network in South America, but it already has the largest market share in several European countries, and faces stiff competition from domestic competitors like Volvo AB. However, truck sales in the U.S. and Canada are expected to grow, with estimates between 250,000 and 280,000 units as the economy continues to strengthen. If consolidated sales are to grow this year, it will probably be due to growth in North America.

Capital position, shareholder-friendly actions

Cash and short-term investments of $2.9 billion is essentially the same as it was one year ago, and provides a strong safety net and source of capital for short-term opportunities. One of the ways the company uses this capital is for share buybacks. The company spent a modest $42.7 million to repurchase shares in 2014, and has roughly $65 million in authorized funds for repurchases. Over the past decade, the company has reduced shares outstanding almost 10% with its program.

Debt, however, has increased, but at a slower rate than sales have grown:

PCAR Total Long Term Debt (Quarterly) data by YCharts.

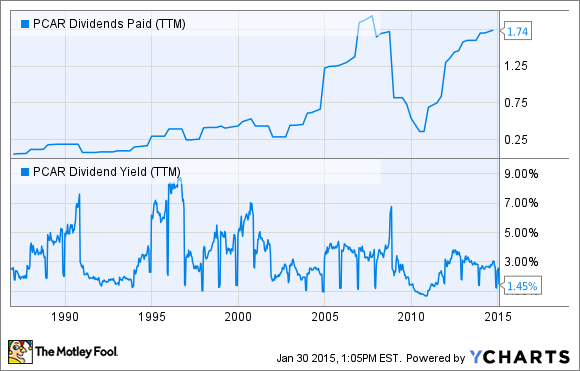

The company has also been steadily growing the dividend, but it still trails the pre-recession peak:

PCAR Dividends Paid (TTM) data by YCharts.

Furthermore, the current yield is still near the low end of the historical average. But this shouldn't be a surprise, as truck sales are only just now returning to sustained growth after a half-decade malaise. It's probably a reasonable expectation that PACCAR will be able to increase its dividend further in coming years.

Looking ahead

As of this writing, PACCAR's stock is down more than 5%, most likely on concerns over the potential for a weakening global economy impacting international sales in 2015. However, PACCAR's earnings tell a good story of strength for the long term. And while that doesn't really tell us much about what the stock will do in the next year, it should serve as a reminder that investors are best served focusing on quality businesses, and not stock market prognosticating.

By most accounts, PACCAR measures up: great management, an industry-leading position, and a strong track record of profitability and market outperformance.