A few weeks ago, we asked the question "What is your investment strategy?" and described the survey Get Rich Slowly did of attitudes toward investing and a few related subjects. In that post, we noted, with a degree of surprise, that over 40 percent of respondents did not invest at all -- and that the youngest respondents were the largest group of non-investors. What follows might help explain why young people are more reluctant to invest at this point.

Recovery from the Great Recession

Economists have taken the view that the economic recovery has been going on for five years or more now. That's because their definition of a recession is simply two consecutive quarters of negative growth in the GDP. However, the survey we conducted in the middle of 2014 also probed opinions about the economy — asking specifically if it has recovered — and it appears that mere mortals like us don't feel it that way. It's probably because it takes a while for the recovery to "trickle down" to us.

So, how did the mere mortals we surveyed feel about the recovery?

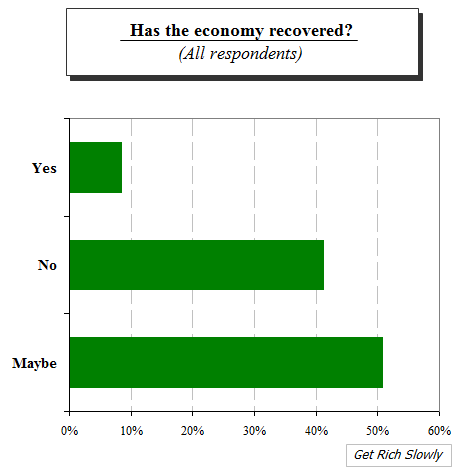

We started by asking: Do you think the economy has recovered from the Great Recession? Here is a summary of the responses:

As of mid 2014, according to our survey, fewer than 10 percent of respondents believed the economy had recovered from the Great Recession. Roughly half the respondents thought the economy may have recovered, but respondents said "no" more than four times as often as "yes." The economy doesn't move that quickly, so even results from six months ago can provide insight into our current situation. From those responses, it's fair to say that respondents may not be quite as convinced of the recovery as economists expect.

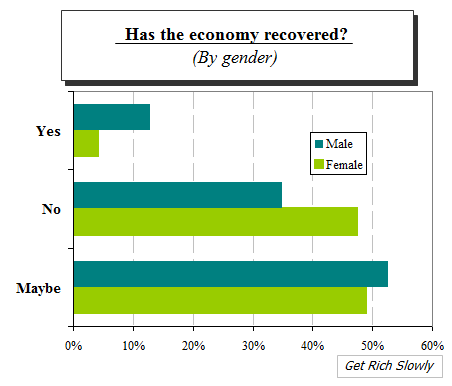

Interestingly, men and women don't view the recovery the same way, as the following chart shows:

I don't have an explanation for these results, but the "no" among men outweighed "yes" more than twice. The results were even more striking among women, who said "no" almost twelve times as often as they said "yes." Furthermore, the "noes" from female respondents were almost as many as the "maybes." Women, it seems, are much less convinced of the economy's recovery than their brethren.

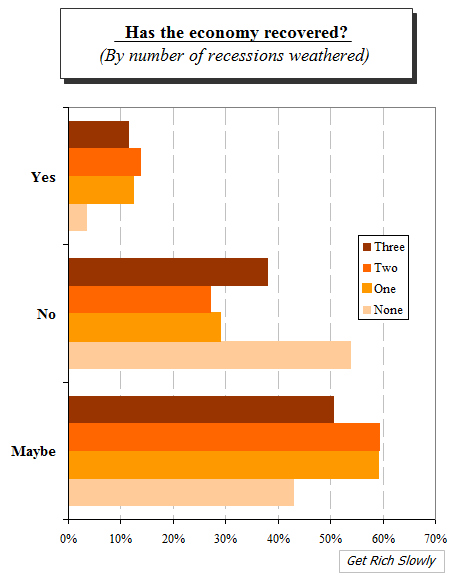

As you might recall, the survey didn't ask for age groups, but it did ask how many recessions respondents have weathered. We used that answer as a proxy for age, because (obviously) the more recessions you've weathered, the older you would be. In the chart below, you can see how these different groups responded. In order to get a better idea of the responses, the bars are colored from light to dark to reflect young to old in age.

It is interesting that the greatest skepticism about the recovery can be found at both ends of the age spectrum. In fact, among the youngest age group, more respondents felt the economy had not recovered than even "maybe." And almost none of them answered "yes."

That response is not surprising, given some of the data.

Troubling data

Economists may pore over abstractions of the economy to determine its health — things like GDP and so forth. However, the face of the economy most of us experience up close and personal is employment and income. For most people, the unemployment rate is a much more tangible indicator of the health of the economy.

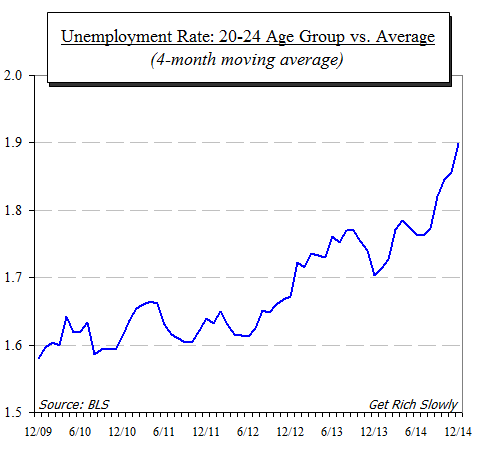

He who brushes his teeth in the White House every morning was correct to point out last week in his State of the Union address how the unemployment rate has fallen to the lowest point since the onset of the Great Recession. However, when you look deeper into the data, something troubling emerges: Although the overall unemployment rate has dropped to its lowest point in that period, the picture looks nowhere near as rosy for the younger members of the workforce.

You can see that the unemployment rate among the 20-to-24-year age group ...

- ... is much higher than the overall average, but

- ... has really not declined significantly at all in the past five years.

We can look at that another way: Historically, the unemployment rate for the 20-to-24 age group has always been higher than the overall rate, averaging about 1.6 times the overall unemployment rate. However, in the past five years since the official end of the Great Recession, their relative unemployment rate has skyrocketed to 1.9 — almost double the overall rate.

That is why it isn't surprising to see younger respondents feeling (quite strongly) that the recession of 2009 has not ended yet — the recovery, it would seem, does indeed look as if it is passing them by. Nobody knows exactly why this is happening. Some have speculated that more kids are going to college (which, they say, also accounts for the ballooning student debt problem), but the studies that have been done have not been able to confirm this.

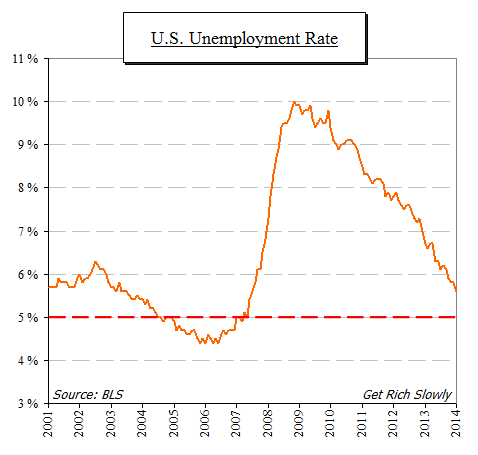

This recovery, it seems, has not produced high-quality jobs over as broad a range as in the recoveries we have experienced from earlier recessions. However, it has produced what the country's leaders have been hoping for, and touting: a drop in the unemployment rate. Here is the chart you'll see on the front page of the Bureau of Labor Statistics (BLS):

Some of you might be thinking: Those numbers are as fake as Dolly Parton's bosom (as she famously claimed last summer at Glastonbury). Whether you think the numbers are real or not is not the point. The point is that people with a tremendous influence over your economic life believe them and, most importantly, do things that impact your life.

See that dotted red line? That is the target the Federal Reserve Board has set (or, to be more accurate, one of the targets) before they begin to raise interest rates. When exactly the Fed will begin to raise interest rates nobody knows for sure, but they have been warning us for more than a year that the move is imminent.

The next thing we don't know is how long it will be before interest rates drop again after that. It's been more than 30 years that interest rates have been steadily dropping. Nobody is suggesting rates will rise for 30 years before dropping again, but it could be a while. If inflation takes off and becomes a problem, interest rates can go higher than many people have seen in their lifetimes.

How does that matter to you?

1. The debt factor

As interest rates rise, debt becomes more expensive — that's obvious. Also obvious is that having no debt is the best way to handle a period of rising interest rates. It is also easy to deduce that, if you are going to have any debt, like a home mortgage, do what you can to make it fixed-rate.

2. The investment factor

This is a little more tricky. For the past 30 years, bond funds have done well. You would think that in a climate of dropping interest rates that wouldn't happen; but as interest rates drop, the market value of the bonds in a fund rises. Therefore, the overall value of bond funds have risen to record levels.

When interest rates rise, that stops. Bond values drop when interest rates rise. (You can Google that if you find it odd, but it is true.) In the coming years, you will need to keep this in mind when you make decisions on rebalancing your investment portfolio -- what you did for the past 30 years might not work the same way when it comes to your bond funds. Of course, experts have been predicting rising interest rates for several years, and it still hasn't happened.

If you are able to buy bonds and hold them till maturity, the drop in market value will leave you unaffected, and you will continue to collect interest until the bond is paid off. However, few of us can afford to buy bonds "straight," which is why bond mutual funds are the investment vehicle most people use to invest in bonds. And bond fund values are very much affected by changes in the market prices of the bonds.

Does this mean you have to bail out of your bond funds? No. What I am saying is that you need to be aware that a climate of rising interest rates usually causes the value of bond funds to decline.

The other thing to keep in mind is that simple short-term investments will begin yielding "real" returns again. Getting, say, 5 percent on your savings account sounds like pie in the sky today; but when interest rates rise, that is a distinct possibility. This is not going to happen overnight; but when you think long-term, keep in mind that the day may not be far off when things like CDs and high-yield savings accounts will become even more viable components of a balanced investment portfolio once again.

This article originally appeared on getrichslowly.org.

You may also enjoy these financial articles: