Older rigs like this jackup have been considered bad for Diamond. That may not be true. Source: Diamond Offshore.

The offshore drilling industry is going through one of the most severe downturns in decades, as oil prices remain well below year-ago levels. And with relatively easy-to-produce onshore supplies in North America that can be increased quickly, the potential for Iran to add more than a half-million daily barrels to an already oversupplied market, and mention significantly more drilling vessels than the market can employ, it's hard to see an improvement in anytime soon.

Diamond Offshore Drilling (DO) reported second-quarter earnings on Aug. 3, and for the most part it was a pretty solid quarter for the company.

But does that make the stock a buy? Let's take a closer look at three reasons Diamond Offshore just may be a buy, as well as the biggest two reasons it might not make sense for your portfolio.

Rough seas ahead

Diamond Offshore CEO Marc Edwards called the current demand environment "the worst in a decade," and it's hard to argue with that assessment. Oil prices are down more than half over the past year, as record onshore oil production in North America coincided with weakening global demand,to create an oversupply that has yet to be fully soaked up. Even as North American producers have slowed drilling, onshore oil production has continued to increase despite predictions that it would level off or even begin falling by now. This continues to feed a market that's just oversupplied with oil.

Offshore drillers are doubly feeling the impact, since drilling companies have ordered record numbers of new vessels over the past several years, spurred by both an aging global fleet, high oil prices, and expectations of increased demand for deepwater and harsh environment exploration and drilling to unlock big offshore reserves.

This double-whammy of too much onshore production and too many offshore vessels could take years to rebalance.

Making the case for Diamond Offshore

Just last quarter, Diamond reported a $256 million loss, good for $2.56 per share in losses. The company took a $319 million impairment ($2.33 per share) on eight vessels, three of which are to be scrapped. Diamond also took a $4 million charge related to restructuring and employee separation costs, probably resulting from the vessels' removal from service. In February, the company suspended the special dividend that it has historically paid each quarter, resulting in an 80% income cut for shareholders as the company tightens its belt.

The combination of the February dividend cut and the big loss reported in May have pushed the stock price down a lot:

And while I'm not going to argue that the stock didn't earn this beat-down, there are three reasons Diamond could be a bargain today:

- A strong balance sheet with low debt.

- Very low downside exposure to newbuilds.

- The ability to stack and scrap more of existing fleet if needed.

Balance sheet and newbuilds

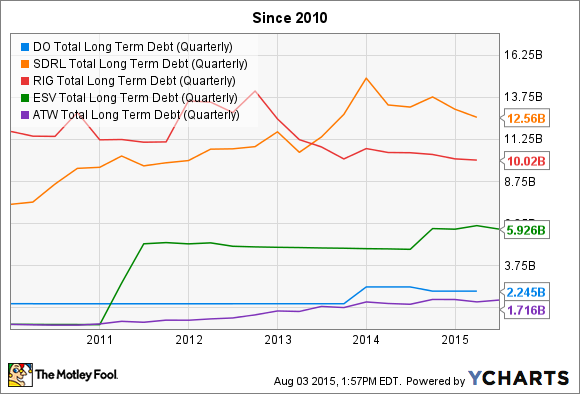

Over the past few years, offshore drillers have ordered significant numbers of new vessels and have used a lot of debt to pay for them:

DO Total Long Term Debt (Quarterly) data by YCharts

Diamond has been incredibly conservative, ordering only five newbuilds to date. Of the five, four have already been delivered, and all are under long-term contracts. The fifth and final vessel is scheduled for delivery in mid-2016 and also already has a contract in place.

At the other extreme, Seadrill, Ltd. (SDRL) has more than a dozen newbuilds on order, with the majority of them scheduled for delivery before the end of next year. That company has more than $3.5 billion in newbuild obligations to meet over the next 16 months, versus a few hundred million for Diamond. Seadrill's debt -- already incredibly high -- is almost guaranteed to increase by billions, while Diamond Offshore's debt is likely to only increase moderately. Think about it this way: Seadrill may have to add more debt than Diamond's total debt over the next year and a half to meet its newbuild obligations.

Yes, Diamond's 24-ship fleet is one of the smaller, while Seadrill, with its 69 vessels, is one of the largest. But if we look at the cost of debt -- measured by interest expense per vessel -- it becomes clearer just how less leveraged Diamond Offshore is:

| Metric | Diamond | Seadrill |

|---|---|---|

| Total Long-term Debt | $2.25 | $12.56 |

| TTM Interest Expense | $66.90 | $403.00 |

| Active Vessels | 23 | 55 |

| Debt Expense Per Active Vessel | $2.91 |

$7.33 |

Long-term debt in billions; interest expense and per-vessel expense in millions. Data source: company filings.

I'm not singling out Seadrill here, but it does provide a strong contrast between how much more leverage its newer fleet has created, versus Diamond's older fleet.

This puts Diamond in a much better position to further reduce its active fleet to cut costs, while still producing enough cash flows to meet its obligations. The company has taken steps in this direction already, stacking 10 rigs and selling off another six over the past year, with plans to stack several more as they come off contract.

Looking forward: Creating opportunity?

On the recent earnings call, management mentioned that the company has been awarded almost 25% of the industry's backlog over the past four quarters, even though its fleet is less than 10% of the market. While this is partly timing of when vessels are available for work, it's some evidence that the company's older fleet is more viable than many have thought.

Furthermore, Diamond may be in a great position over the next year to take advantage of the downturn and pick up attractive assets on the cheap as competitors are forced to deleverage.

Time to buy? Depends on your situation, too

Whether you want to buy probably depends on your current exposure to offshore drilling, your time horizon, and your investing objectives. If you already have significant exposure to offshore drillers or are investing for income, I probably wouldn't invest in the sector at all. The reality is there isn't a clear end in sight, and that could mean more losses, and a further dividend cut that makes the current 2.5% yield no guarantee.

But if you have limited or no exposure to the segment and are willing to ride out maybe a few years of continued volatility, Diamond's balance sheet and limited leverage make it worth consideration. Don't get me wrong -- there's still real risk that demand for offshore drilling is weak for a couple of years. But if you're willing to stomach that risk, Diamond could be a market-crushing investment over the next five years