Source: Western Gas Partners.

The midstream MLP industry is now in chaos, with even such blue-chip operators as Kinder Morgan slashing dividends as debt and equity growth funding dries up.

With energy prices threatening to fall to new multi-year lows and no relief in sight, investors in Western Gas Partners (WES 0.14%) and its general partner, Western Gas Equity Partners (NYSE: WGP), may be understandably concerned about the growth and security prospects of both MLPs and their payouts. To see if such concerns are merited, let's look at the two most important factors that will determine their business and distribution growth chances over the next few years.

Good growth prospects safeguard the distribution

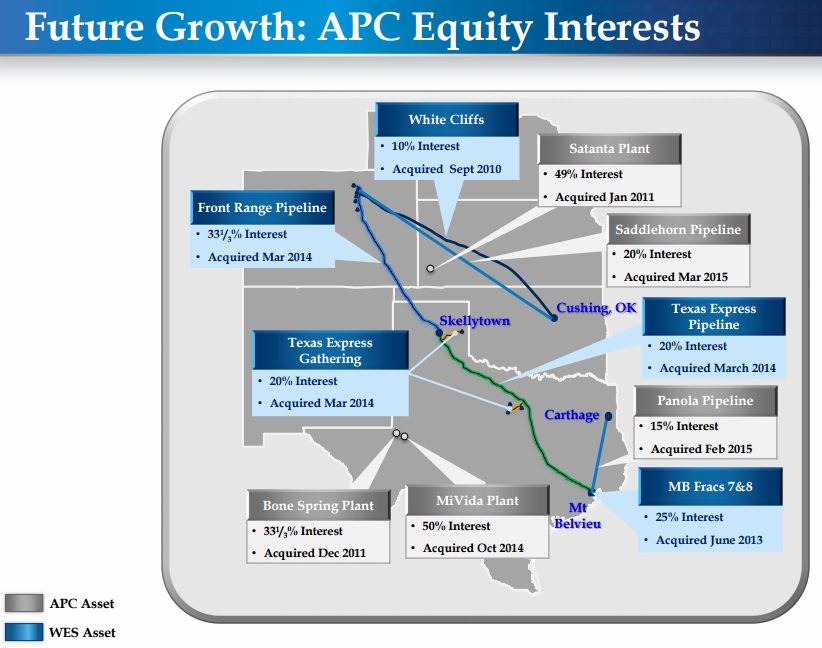

Western Gas Partners' sponsor and majority owner of Western Gas Equity Partners is Anadarko Petroleum (APC +0.00%),which launched the MLP with 14 potential dropdown assets, of which Western Gas has acquired 12 so far at a cost of about $3 billion.

The reason these last two potential dropdowns are so important is that while it's true that 98% of Western Gas's 2015 adjusted gross margin is derived from fixed-fee contracts, as Energy Transfer Partners' (ETP +0.00%) most recent quarter illustrated, fee-based contracts can still have exposure to volatile energy prices if the volumes aren't guaranteed. Only 51% of Energy Transfer Partners' volumes year to date had firm volume commitments, which left the MLP vulnerable to decreasing oil and gas production that made its current distribution coverage ratio fall dangerously low.

Only 68.2% of Western Gas' volumes are ensured by such commitments,and management has already seen decreased volumes from its Marcellus shale assets. Western Gas Partners' best protection against letting declining volumes in 2016 threaten its own payout is to either bring new projects online or acquire new assets whose cash flows can offset falling volumes across some of its systems.

Luckily for Western Gas, the dropdowns it has already bought from Anadarko Petroleum consisted of 10% to 33% interest stakes. Increasing ownership in what it already owns, as well as acquiring and expanding the equity ownership of some of Anadarko Petroleum's other assets, represent substantial options for growing its business over the next year or two.

Source: Western Gas Partners investor presentation.

Another growth option for Western Gas is organic growth projects, of which it has two in the planning stages. The first is the recently announced $115 million expansion of the Ramsey gas processing plant in the Delaware Basin. Then there's the proposed Delaware Basin Express Pipeline. Western Gas is holding a non-binding open season to determine customer interest and potentially lock down firm volume commitments. According to CEO Don Sinclair, "We are very encouraged by the interest shown."

Of course, a midstream MLP can have all the growth prospects in the world, but as Kinder Morgan's recent funding troubles have shown, if you can't raise cheap growth capital, then dividend investors might need to accept a payout cut for management to fund growth using distributable cash flow. Western Gas Partners happens to have a few things working in its favor to help it grow without having to potentially gut its distribution.

Strong balance sheet provides plenty of growth capital

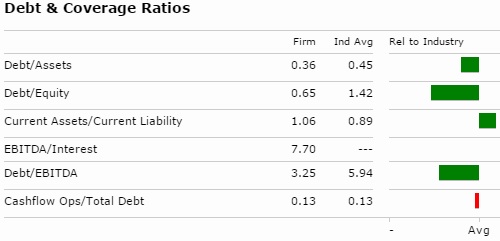

Source: Morningstar.

With a Q3 and year-to-date distribution coverage ratio of 1.05, and 1.13, respectively, Western Gas Partners' payout remains secure for now but isn't generating a substantial amount of excess distributable cash flow with which to internally fund its growth. Thus the MLP will have to turn to debt and equity markets to secure the capital it needs to expand or acquire new assets.

Western Gas Partners' balance sheet is a lot cleaner than most of its peers. The most important metric to focus on is the debt-to-EBITDA ratio, or leverage ratio. The leverage ratio is one of the key things credit rating agencies and lenders use to determine how capable an MLP is of servicing its debt.

Western Gas Partners' current liquidity of $1.073 billion consists of cash and the remaining $1 billion in borrowing power under its revolving credit facility. However, credit revolvers come with debt covenants that need to be complied with. In its case, Western Gas is required to maintain a leverage ratio of 5.0 or less, except for the first nine months following an acquisition, when it's allowed a maximum leverage ratio of 5.5.

Western Gas' low debt levels grant the MLP the ability to take on an additional debt to grow. Thus, Western Gas can utilize all of its credit facility to fund its growth and further secure its distribution.

In addition, unlike Energy Transfer Partners, which currently yields 12.9%, Western Gas Partners' 7.2% yield means it may still be able to tap the equity markets to raise growth capital.

Bottom line: Western Gas is better positioned than many midstream MLPs, but risks still remain

With strong access to liquidity due to its much better than average balance sheet, Western Gas should be able to continue growing its DCF in 2016. However, falling oil and gas production might still hurt its cash flow, so investors need to keep an eye on its distribution coverage ratio in the quarters to come.