Published April 22, 2024

A trial balance is designed to ensure that debits and credits in your general ledger are in balance. While accounting software has reduced the need for a trial balance, it can still be useful.

A trial balance is a report that lists the ending balance of all of your general ledger accounts. Used to ensure that debits and credits match, a trial balance serves as a way to check for posting errors and out-of-balance accounts.

Overview: What is a trial balance?

One of many useful accounting tools, particularly for those new to accounting, a trial balance is used in preparation for creating both adjusting entries and closing entries, as well as other financial statements.

The purpose of a trial balance is to ensure that all debit transactions entered into the general ledger equal all of the credit transactions that have been entered.

While a trial balance provides you with the end balance of each account, and will indicate when accounts are not balanced, it does not provide you with the details of any accounting transactions that have been entered during the accounting period.

How the trial balance works

The trial balance is used to ensure that the ending total of all debits recorded in your general ledger equals the ending total of all credits that are recorded.

A trial balance can be run each accounting period, each quarter, or annually, depending on your business needs. Most businesses will prepare an initial trial balance, which is reviewed to spot errors or inconsistencies.

Once adjusting entries (if any) are made, you will need to run an adjusted trial balance, which will display the new ending balances of all of the general ledger accounts.

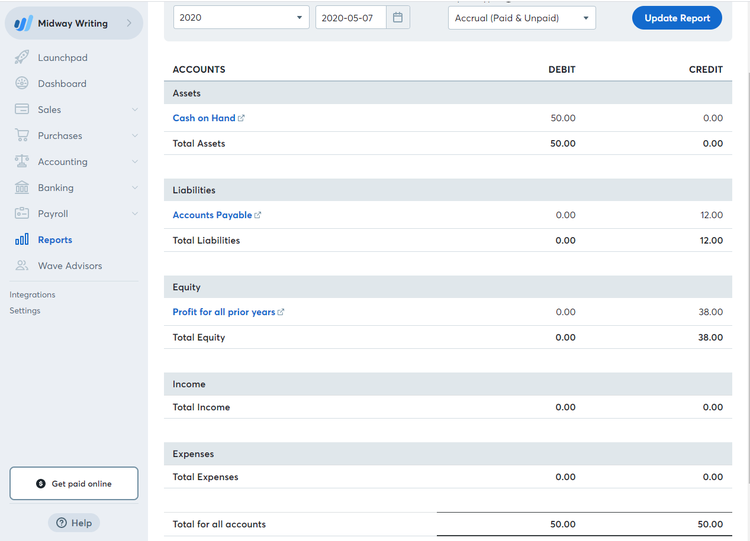

This trial balance from Wave Accounting displays all GL accounts and their ending balance. Image source: Author

Keep in mind that all of the accounts in your general ledger will be included in your trial balance, so the more accounts you have set up, the longer your report will be.

It’s also important to remember that the trial balance is designed to provide ending balances only, and is not used to determine the accuracy of the transactions that are included in the ending balance.

To prepare a trial balance manually using a spreadsheet application such as Microsoft Excel, complete the following steps:

- Prepare a worksheet with four columns for your general ledger account number, account name, debits, and credits.

- Record the totals of all of the ledger accounts that have been used during the period that you’re preparing the trial balance for. Remember each of the five account types; Assets, Liabilities, Income, Expenses, and Revenue, and post the balances accordingly. For example, if you have a positive balance in an asset account, it would be posted in your trial balance as a debit, while a positive revenue balance would be posted as a credit.

- After you finish entering all of the balances from your ledgers, you will need to add them up to ensure that both the debit and credit columns balance.

- If debit and credit totals match, you can move on to analyzing ending balances for discrepancies. For instance, if you know you didn’t have rent expenses in the current month, but the ending balance for the month shows a rent expense in the amount of $500, you will have to research the account to see what was posted erroneously, and make an adjusting entry. If the ending debit and credit balances don’t match, you will need to research what accounts are out of balance and make any corrections.

Some of the more common reasons why your debits and credits may not match include:

- Addition errors

- Forgetting to add an entry from a subsidiary ledger

- Posting an amount in the wrong column

- Completing only part of an entry

Examples of a trial balance

There are three trial balance reports: the unadjusted trial balance, the adjusted trial balance, and the post-closing trial balance. All three of these trial balances use the same format, with the only difference being any adjustments that need to be made prior to closing the accounting period.

The unadjusted trial balance is the first report that you will run. This shows the ending balances in all of your general ledger accounts before any adjusting entries are completed.

Let’s look at the following trial balance examples, with the unadjusted trial balance first:

Unadjusted trial balance for period ending 4-30-2020

| Account Number | Account Name | Debit | Credit |

|---|---|---|---|

| 1000 | Cash | $25,000 | |

| 1010 | Accounts Receivable | $10,000 | |

| 1015 | Prepaid Insurance | $750 | |

| 1020 | Inventory | $1,500 | |

| 1030 | Accumulated Depreciation | $ 2,100 | |

| 2000 | Accounts Payable | $ 5,125 | |

| 2010 | Notes Payable | $4,000 | |

| 3000 | Common Stock | $9,000 | |

| 4000 | Revenue | $21,700 | |

| 5000 | Payroll Expense | $2,000 | |

| 5010 | Insurance Expense | $125 | |

| 5015 | Utilities Expense | $1,250 | |

| 5020 | Postage | $400 | |

| 5030 | Depreciation Expense | $900 | |

| TOTALS | $41,925 | $41,925 |

The unadjusted trial balance reflects ending account balances before any adjusting entries have been made. While the trial balance may be fairly accurate, you know that you need to complete adjusting entries for both insurance and depreciation expenses for the month. Your adjusting entries are as follows:

| Account | Debit | Credit |

|---|---|---|

| Insurance Expense | 125 | 125 |

| Depreciation Expense | 250 | 250 |

After the above entries have been posted to the appropriate general ledger accounts, you are now ready to run an adjusted trial balance, which will reflect the updated balances.

Adjusted trial balance for period ending 4-30-2020

| Account Number | Account Name | Debit | Credit |

|---|---|---|---|

| 1000 | Cash | $25,000 | |

| 1010 | Accounts Receivable | $10,000 | |

| 1015 | Prepaid Insurance | $625 | |

| 1020 | Inventory | $1,500 | |

| 1030 | Accumulated Depreciation | $2,350 | |

| 2000 | Accounts Payable | $5,125 | |

| 2010 | Notes Payable | $4,000 | |

| 3000 | Common Stock | $9,000 | |

| 4000 | Revenue | $21,700 | |

| 5000 | Payroll Expense | $ 2,000 | |

| 5010 | Insurance Expense | $250 | |

| 5015 | Utilities Expense | $1,250 | |

| 5020 | Postage | $400 | |

| 5030 | Depreciation Expense | $1,150 | |

| TOTALS | $42,175 | $42,175 |

If you compare the adjusted trial balance with the unadjusted trial balance, you’ll see that the ending totals have changed, as have your prepaid insurance, depreciation expense, insurance expense, and accumulated depreciation account balances.

The final trial balance, or post-closing trial balance, will be run after closing entries are completed. These will reflect your beginning balances as of 5-1-2020.

Post-closing trial balance as of 5-1-2020

| Account Number | Account Name | Debit | Credit |

|---|---|---|---|

| 1000 | Cash | $25,000 | |

| 1010 | Accounts Receivable | $10,000 | |

| 1015 | Prepaid Insurance | $625 | |

| 1020 | Inventory | $1,500 | |

| 1030 | Accumulated Depreciation | $2,350 | |

| 2000 | Accounts Payable | $5,125 | |

| 2010 | Notes Payable | $4,000 | |

| 3000 | Common Stock | $9,000 | |

| 3010 | Retained Earnings | $16,650 | |

| TOTAL | $37,125 | $37,125 |

You’ll notice that both the revenue and expense accounts have been removed from the post-closing trial balance, and a retained earnings account has been added, which reflects the revenue adjustment minus expenses.

If you’re entering accounting transactions manually or using spreadsheet software, running a trial balance is a must. If you’re using accounting software, you can still run a trial balance at the end of the accounting period to ensure that your ending balances look right.

Your trial balance can tell you a lot

If you’re using a manual accounting system and are worried about accuracy in your accounting, trial balance reports provide you with a handy tool to ensure that your debit and credit transactions are balanced.

While using accounting software drastically reduces the need for the trial balance report, these reports can still be useful in many ways.

If you’re tired of tracking income and expenses using spreadsheet software, be sure to check out The Ascent’s accounting software reviews, and find an application that will work for you.

Our Small Business Expert

Mary Girsch-Bock studied accounting and business at UIC. After working as an accountant for many years in various industries, including healthcare and property management, she returned to her first love, writing. She specialized in accounting and business articles, with an emphasis on software reviews, which she wrote for more than 20 years. She continues to write for the first publication she ever wrote for, CPA Practice Advisor, while blogging for several software companies.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

The Motley Fool has a disclosure policy.