Published April 22, 2024

Everyone knows what a payroll advance is, but do you know the best way to handle them for your small business? We’ll explain how a payroll advance should work and ways to avoid potential problems.

We can all hit a rough patch. A car that suddenly stops working or an unexpected illness can drain our savings quickly. That’s where a payroll advance may come into play.

Are you prepared if your employee requests a payroll advance? Do you have a policy and guidelines in place to prevent abuse and ensure the advance is paid back promptly?

Keep in mind, business owners aren't required to offer a payroll advance to their employees. However, if you’re on board with offering an advance to your employees, you’ll first need to create a sound payroll advance policy so when (not if) an employee does request an advance, you’re prepared.

Overview: What is a payroll advance?

A payroll advance is a short-term loan you give your employees, with the agreement that the loan will be repaid using future wages earned. Depending on the agreement you create with your employee, a payroll advance has specific terms that both you, the employer, and your employee will need to abide by.

How does a payroll advance work

Your employee should request a payroll advance in writing. If an employee does come to you with a request for a payroll advance, the first thing you should do is ask that they put their request in writing, to create a paper trail from the initial request to the agreement and repayment plan.

A written agreement should be a part of any payroll advance, with the agreement signed by you and the employee receiving the payday advance before processing payroll.

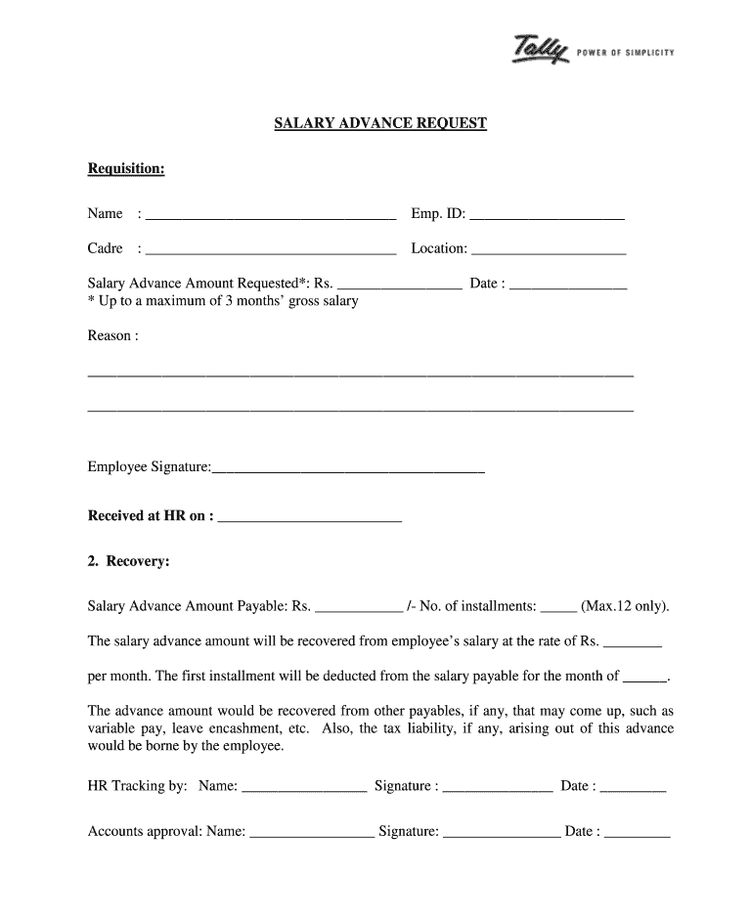

The sample payroll advance request can be customized to suit your needs. Image source: Author

A payroll advance should be processed separately from your regular payroll run, an easy task if using payroll software or a payroll service provider. If you’re handling payroll manually, you’ll need to write your employee a separate check to cover the advance.

You will then need to deduct the agreed-upon payments from your employee’s next paycheck, continuing to do so until the advance has been paid in full. You can easily do this using payroll software or a payroll service.

Always reflect any payroll advance given to an employee in your payroll register, with all repayments reflected as well.

The wrong way to handle a payroll advance

Rachel has three employees. On a Monday morning, Bob, one of Rachel’s employees, approaches her to ask for an advance.

There is nothing in the employee handbook covering employee advances. After a moment’s hesitation, Rachel agrees to a pay advance loan of $350. Rachel and Bob agree he will pay back the advance from his next four checks.

Rachel writes a check advance to Bob for $350 later that day.

The next day, Bob fails to show up for work, and never returns, leaving Rachel out $350. She can deduct some of the money from Bob’s final check, but since he worked only one day, it doesn’t begin to cover the advance, leaving Rachel out more than $300.

The right way to handle a payroll advance

Jim has a staff of five. On a Monday morning, Sara, one of his employees, approaches him, requesting an advance. Jim asks the employee to put the request in writing.

Within an hour, Sara returns with her request in writing. Although she has requested $500, Jim only offers a $250 advance, the maximum advance offered by the company. He presents Sara with an agreement that includes the amount of the advance and the repayment schedule. The agreement contains a section for how any unpaid advances will be handled should an employee quit before paying back the entire advance.

Sara reads and signs this agreement before Jim provides her with the advance. Once Sara signs the agreement, Jim signs it, making a copy for himself and placing a copy in Sara’s personnel file, along with her original advance request.

How to avoid problems with a payroll advance

Payroll advances can be a lifesaver for an employee who runs into financial trouble. But without clear guidelines in place, they can also be easily abused, with employers paying the price.

If you offer payroll advances to your employees, it’s important you establish payroll advance guidelines that must be followed by all employees without exception. These policy guidelines should then be incorporated into your payroll management processes and provided to your employees as part of an employee handbook. If you don’t have an employee handbook, the policy guidelines should be distributed as a separate document.

If you’re interested in offering payroll advances to your employees, but want to avoid legal missteps, consider these steps.

1. Specify eligibility

Are all of your employees eligible to receive a payroll advance or do you want to limit eligibility to full-time employees only? What about employees on probation? Can they receive an advance?

It’s important to provide these details when creating your payroll advance policy and apply them equally across the board, no matter the circumstances.

2. Frequency of advances

You may want to limit the number of advances employees can receive. Some businesses limit advances to one every six months, while others may limit the advances to two per year. You may also want to consider adding a clause that prohibits an employee from receiving a second advance if the first has not been repaid in full.

3. Set a cap

It’s important to set a cap for how much an employee can receive, and include that cap in your policy.

4. Don’t bend the rules for an employee

You have rules in place for a reason. If you bend or break those rules for an employee, you’re creating a situation where you can be sued for discrimination.

For example, George approaches his employer, Ben, for a payroll advance. George and Ben are good friends outside of work, so Ben agrees to an advance of $700, even though company policy states that advances top out at $500.

Lucy, who approached Ben a month ago for an advance of $600, and was only given $500, per policy rules, finds out about George’s advance and threatens to sue Ben for discrimination.

The lesson here is that even though it’s your business, if you have a policy in writing, that policy must be adhered to under any circumstance, or you could find yourself in serious legal trouble.

5. Always complete a written agreement

Once you agree to provide a payroll advance, you’ll need to create a written agreement, with all terms and conditions of the advance spelled out in clear terms. The agreement should include the advance amount, the repayment terms, the amount to be deducted each pay period, and when the deductions will start and end.

Both you and your employee need to sign the payroll advance agreement, with a copy of the agreement placed in the employee’s personnel file as well.

6. Don’t tax the advance

Payroll tax deductions should be deferred until your employee starts to repay the paycheck advance they received. Include the amount of the repayment when calculating and accruing payroll for upcoming pay periods.

7. Set up a repayment plan

Setting up a repayment plan in your payroll system guarantees you won’t forget to deduct the loan amount from your employee’s paycheck. If you’re not sure how to add a payroll deduction, your payroll service provider can assist you.

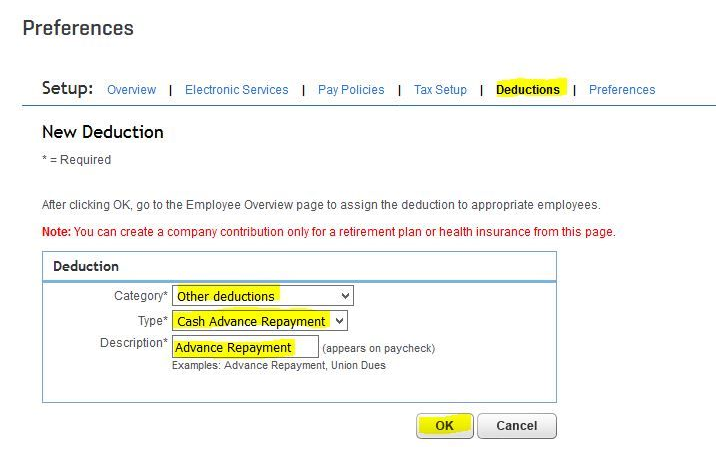

The New Deduction screen in QuickBooks Online Enhanced Payroll allows you to create a new deduction for payroll advances. Image source: Author

Should you offer payroll advances?

Not every small business is in a financial position to offer a salary advance to its employees.

However, if your business can offer payroll advances, it’s imperative you create a clear policy around payroll advances and always adhere to the rules, no matter the employee or the circumstances.

Our Small Business Expert

Mary Girsch-Bock studied accounting and business at UIC. After working as an accountant for many years in various industries, including healthcare and property management, she returned to her first love, writing. She specialized in accounting and business articles, with an emphasis on software reviews, which she wrote for more than 20 years. She continues to write for the first publication she ever wrote for, CPA Practice Advisor, while blogging for several software companies.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent, a Motley Fool service, does not cover all offers on the market. The Ascent has a dedicated team of editors and analysts focused on personal finance, and they follow the same set of publishing standards and editorial integrity while maintaining professional separation from the analysts and editors on other Motley Fool brands.

The Motley Fool has a disclosure policy.