Published April 22, 2024

Manufacturing companies need to track both product costs and period costs. Learn the difference between these two types of costs and why each is important.

If you’re currently in business, you need a good way to manage costs. While using accounting software is the best method for managing costs, even if you’re still recording transactions in a manual ledger or using a spreadsheet application, you can learn to manage business costs properly.

Managing your costs is doubly important if you own a manufacturing business, since you’ll need to manage both product and period costs. Product costs, also known as direct costs or inventoriable costs, are directly related to production output and are used to calculate the cost of goods sold.

On the other hand, period costs are considered indirect costs or overhead costs, and while they play an important role in your business, they are not directly tied to production levels.

Both product costs and period costs directly affect your balance sheet and income statement, but they are handled in different ways. Product costs are always considered variable costs, as they rise and fall according to production levels.

What are product costs?

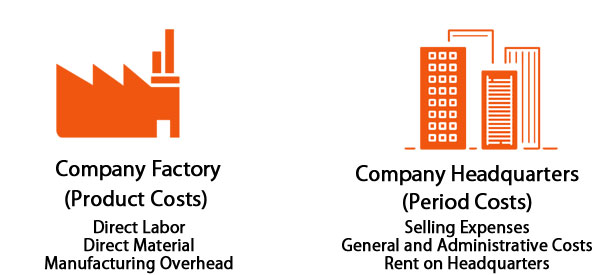

Product costs are the costs incurred during the manufacturing process. Product costs are always related to production, and typically include the following:

- Direct labor cost: If you’re still unclear about direct vs. indirect labor, remember that direct labor is wages and benefits paid to an employee who is directly involved in the production process. Assembly line workers, painters, welders, and other line workers would all be considered direct labor.

- Direct materials cost: Direct materials are the raw materials that are required to manufacture a product. If you’re manufacturing rocking chairs, the wood you purchase to assemble the rocking chairs would be considered a direct material cost.

- Direct supplies cost: Along with purchasing direct materials to manufacture your rocking chairs, you’ll also have to purchase additional items such as glue, nails, and varnish. These are all necessary in order to produce the rocking chair, so they’re considered direct supplies and are always included in product costs.

- Factory overhead: If your production facility is located in a different facility than your administrative headquarters, the cost of maintaining that separate facility should be included in product costs. These costs include rent or a mortgage payment, security used to guard the facility, and even utilities such as gas and electricity. If the manufacturing facility and the administrative building are under one roof, you’ll need to allocate the overhead cost of the manufacturing facility in your product cost.

Accurately calculating product costs also assists with more in-depth analysis, such as per-unit cost. Per-unit cost is calculated by dividing your costs by the number of units produced. It is an important metric, particularly when determining product pricing.

What are period costs?

Period costs are the costs that your business incurs that are not directly related to production levels. These expenses have no relation to the inventory or production process but are incurred on a regular basis, regardless of the level of production.

Period costs are typically divided into two categories: administrative costs and selling costs. Examples of period costs include:

- Office expenses: Office expenses such as rent, cleaning, and office supplies are considered period costs. If both administrative and factory facilities are located under one roof, rent cost must be allocated according to the space used by each.

- Insurance: Insurance expenses are a period cost.

- Advertising: Any advertising or marketing related expense is a period cost.

- Salaries: Salaries paid to non-production employees, such as administrative staff, managers, and other support personnel, are considered indirect labor expenses, which are a period cost.

- Utilities: Expenses such as gas and electric are considered a period cost, unless they directly involve the manufacturing plant. Like rent, if administrative and factory facilities are under one roof, utility costs must be allocated according to the space used by each.

- Insurance: Insurance expenses are a period cost.

- Professional fees: If you hire an attorney, an accountant, or other professional consultant, those fees are considered a period cost.

- Sales: Sales includes any and all costs associated with selling products to your customers. Delivery fees and shipping costs are included in sales. While some may argue that sales costs are directly related to production, it’s only after production is completed and a product is available to sell that the sales department can do its job, making sales a period cost, not a product cost.

The one similarity among the period costs listed above is that these costs are incurred whether production has been halted, whether it’s doubled, or whether it’s running at normal speed.

Most period costs are considered periodic fixed expenses, although in some instances, they can be semi-variable expenses. For example, you receive a utility bill each month that is not directly tied to production levels, but the amount can vary from month to month, making it a semi-variable expense.

Regardless, all period costs, whether fixed or semi-variable, are considered expenses and will be reported on your income statement.

Product vs. period costs: What's the difference?

Product costs are always related to production, with period costs being considered indirect or overhead costs. Think of it like this: If you stop production for a month, no product costs will be incurred.

However, you’ll still have to pay the rent on the building, pay your insurance and property taxes, and pay salespeople that sell the products currently in inventory.

Product costs are directly related to production, while period costs are associated with overhead. Image source: Author

The table below highlights some of the differences between product costs and period costs:

| Product Costs | Period Costs |

|---|---|

| Always related to the manufacturing process | Not affected by production levels |

| Related to volume, such as units produced or labor hours | Related to overhead and indirect costs |

| Always variable, depending on production levels | Usually fixed, but can also be semi-variable |

| Include labor, materials, supplies, and factory overhead | Includes administrative, sales, and distribution costs |

| Are recorded on a balance sheet | Are recorded on an income statement |

Final thoughts on product and period costs

Product and period costs are incurred in the production and selling of a product.

By separating these two very different cost types, you can more easily identify potential problem areas in production, such as inefficient labor, inferior machinery, or outdated procedures, while also reviewing production costs, such as raw materials and direct labor.

You’ll also be able to spot trouble spots or overspending in administrative areas or if overhead has ballooned in recent months.

Though it may be tempting to just lump your expenses together, there are three great reasons why you need to separate product and period costs for your business.

Accurate financial statements

Because product and period costs directly impact your financial statements, you need to properly categorize and record these costs in order to ensure accurate financial statements.

Speaking of financial statements, it’s important that you take the time to review your financial statements on a regular basis. As an owner, you rely on their accuracy to make key management decisions. This can be particularly important for small business owners, who have less room for error. If product and period costs are overstated or understated, or not recorded at all, your financial statements will be wrong as well.

Save time and money

Recording product and period costs may also save you some money come tax time, since many of these expenses are fully deductible. But you won’t be able to deduct them if you don’t know what they are.

Accurate pricing for your products

Finally, managing product and period costs will help you establish more accurate pricing levels for your products. Being aware of the total costs involved in manufacturing an item, including indirect costs, will help to ensure that your products aren’t priced too low or too high, but are priced to earn your business a profit, something every business owner strives to achieve.

Our Small Business Expert

Mary Girsch-Bock studied accounting and business at UIC. After working as an accountant for many years in various industries, including healthcare and property management, she returned to her first love, writing. She specialized in accounting and business articles, with an emphasis on software reviews, which she wrote for more than 20 years. She continues to write for the first publication she ever wrote for, CPA Practice Advisor, while blogging for several software companies.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent, a Motley Fool service, does not cover all offers on the market. The Ascent has a dedicated team of editors and analysts focused on personal finance, and they follow the same set of publishing standards and editorial integrity while maintaining professional separation from the analysts and editors on other Motley Fool brands.

The Motley Fool has a disclosure policy.