Average Credit Card Debt in America

KEY POINTS

- Average Debt Per American: As of Q4 2025, the average American credit card debt is $6,715, marking a 2% increase from the previous year.

- Total U.S. Credit Card Debt: U.S. credit card debt reached $1.252 trillion in Q1 2026.

- State Debt Variations: Alaska leads with the highest average state debt at $8,077, while Kansas has the lowest at $5,329.

At first glance, credit card debt numbers in the United States look enormous. Consumers owe an astounding $1.252 trillion on their credit cards, and the average American credit card debt balance is $6,715.

We've reviewed research from government agencies and credit bureaus to get the most up-to-date data on U.S. credit card debt. Keep reading for the latest credit card debt statistics.

How much credit card debt does the average American have? $6,715 as of Q4 2025

The average credit card balance is $6,715 as of the fourth quarter of 2025, according to TransUnion. That's a 2% increase from the previous year.

| Period | Average Credit Card Debt |

|---|---|

| Q4 2025 | $6,715 |

| Q3 2025 | $6,523 |

| Q2 2025 | $6,473 |

| Q1 2025 | $6,371 |

| Q4 2024 | $6,580 |

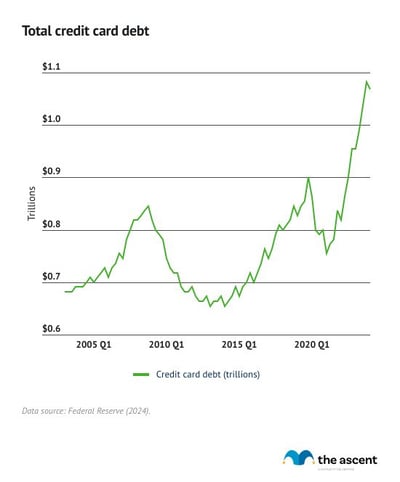

Total credit card debt: $1.25 trillion

Total U.S. credit card debt fell to $1.252 in the first quarter of 2026, from $1.277 trillion in the previous quarter. While credit card debt fluctuated during the pandemic, it began to steadily rise in 2021 as inflation took off.

Over the last decade, credit card debt has typically accounted for between 5.5% to 6.5% of total household debt.

Average credit card debt per household: $9,289

The average American household has about $9,289 in credit card debt, based on the most recent U.S. credit card debt and household data.

Average credit card debt per household was calculated by dividing U.S. credit card debt in the first quarter of 2026 ($1.252 trillion) by the most recent household data (134.790 million as of 2025). This number is higher than the average credit card debt per borrower because multi-person households are more likely to have multiple credit cards.

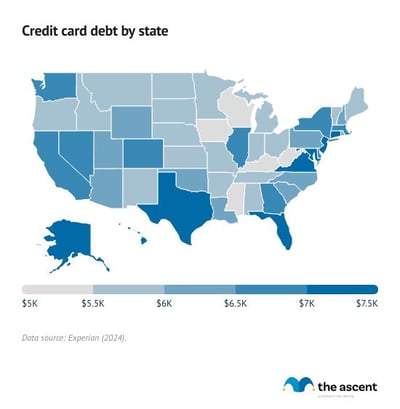

Average credit card debt by state: Alaska leads

Alaska has an average credit card debt of $8,077, more than any other state. Kansas and Wisconsin have the smallest average balances, at $5,329 and $5,370, respectively.

Credit card debt varies widely by state. Here's a full list of each state's average credit card balance as of 2024.

States with the highest credit card debt

- Alaska: $8,077

- Florida: $7,861

- New Mexico: $7,605

- Connecticut: $7,568

- Idaho: $7,560

States with the lowest credit card debt

- Kansas: $5,329

- Wisconsin: $5,370

- Louisiana: $5,399

- West Virginia: $5,427

- Missouri: $5,553

Average credit utilization rate holds at 29%

The average credit utilization rate is 29% as of 2025, level with 2024 and up 1% from 2022.

This metric, also known as a credit utilization ratio, is calculated by dividing a credit card balance by the credit limit. A credit card with a $1,000 balance and a $10,000 credit limit, would have a 10% utilization rate.

| Year | Average Credit Utilization Rate |

|---|---|

| 2020 | 25.4% |

| 2021 | 25.5% |

| 2022 | 28.0% |

| 2023 | 29.0% |

| 2024 | 29.1% |

| 2025 | 29.1% |

Lower credit utilization can improve credit scores. The conventional wisdom is to keep utilization below 30%, and the data suggests consumers are doing well to manage their credit cards.

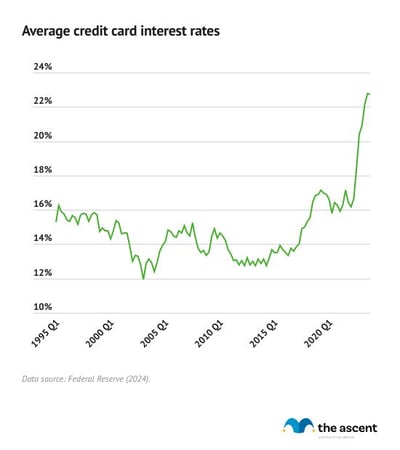

Average credit card interest rate: 22.3%

The average credit card APR on interest-bearing accounts is 22.3% as of Q4 2025. Credit card interest rates rose quickly after 2021, as the Federal Reserve hiked its benchmark interest rate, but moderated somewhat in 2025 and 2026.

Interest-bearing accounts include all credit cards that charge interest. It excludes credit cards that aren't charging interest at that time, so 0% intro APR credit cards don't count until the introductory period ends.

Credit card interest accounts for a significant share of card issuers' earnings. Interest rates have shot up since 2021, from 15.91% in the first quarter of that year.

READ MORE: How Does Credit Card Interest Work?

8.61% of credit card balances flowed into delinquency in Q1 2026

Data from the Federal Reserve shows credit card delinquencies stabilizing.

The 30-day past due delinquency transition rate for credit cards fell to 8.61% in the first quarter of 2026, from 8.69% in the previous quarter. The serious delinquency rate, in which balances are 90 days or more past due, was 7.10%, down slightly from 7.13%.

Overall, 13.12% credit card balances are 90 days or more delinquent, up from 12.7%.

Average credit card debt by income: Middle-income Americans are most likely to carry a balance

Americans in higher income brackets carry higher credit card balances on average.

However, it's the middle and upper-middle classes that are most likely to have credit card debt. Among Americans in the 60th through 79th income percentiles, 54% have credit card debt. Those in the 40th through 59th income percentile are more likely to have credit card debt, with 57% carrying a balance.

It's Americans in the highest (90th to 100th) and lowest (under 20th) income percentiles who are least likely to carry credit card balances. A third of Americans in the lowest income percentile carry credit card debt, while a quarter of those in the highest income percentile do.

| Income Percentile | Median Annual Income | Median Credit Card Debt | Average Credit Card Debt | Percentage With Credit Card Debt |

|---|---|---|---|---|

| Less than 20% | $20,540 | $1,400 | $3,630 | 33.40% |

| 20% to 39% | $43,240 | $1,600 | $3,840 | 46.40% |

| 40% to 59% | $70,260 | $2,500 | $5,950 | 56.90% |

| 60% to 79% | $115,660 | $3,500 | $7,440 | 54.40% |

| 80% to 89% | $189,160 | $5,000 | $8,900 | 44.60% |

| 90% to 100% | $390,210 | $6,000 | $11,210 | 25.40% |

| All families | $70,260 | $2,700 | $6,120 | 45.20% |

Average credit card debt by race: White Americans carry the highest balance

White Americans have an average credit card debt of $6,930 and a median credit card balance of $3,000, the most of any racial identity/ethnicity.

Hispanic Americans have the lowest average credit card debt at $4,150, and both Hispanic and Black Americans share the lowest median credit card debt at $1,700.

| Race/Ethnicity | White, Non-Hispanic | Black, Non-Hispanic | Hispanic | Other | All Families |

|---|---|---|---|---|---|

| Median credit card debt | $3,000 | $1,700 | $1,700 | $2,970 | $2,700 |

| Average credit card debt | $6,930 | $4,360 | $4,150 | $5,910 | $6,120 |

| Percent holding credit card debt | 42.20% | 56.30% | 55.80% | 43.30% | 45.20% |

Average credit card debt by age: Gen X holds the highest balance

Generation X carries the highest average credit card balance at $9,600. That's over $2,500 more than millennials, who have the second-highest average credit card balance of $6,961.

The lowest average credit card debt by age is the Silent Generation, with $3,445, followed closely by Gen Z, with an average credit card balance of $3,493. Since young adults have lower incomes on average, they also have lower average credit limits, which at least helps them avoid credit card debt.

| Year | Generation Z (18–28) | Millennials (29–44) | Generation X (45–60) | Baby Boomers (61–79) | Silent Generation (80+) |

|---|---|---|---|---|---|

| 2012 | — | $2,974 | $6,434 | $6,872 | $4,076 |

| 2013 | — | $3,119 | $6,621 | $6,905 | $4,089 |

| 2014 | — | $3,286 | $6,790 | $6,892 | $4,068 |

| 2015 | — | $3,499 | $6,981 | $6,862 | $4,023 |

| 2016 | $1,867 | $3,809 | $7,260 | $6,863 | $3,985 |

| 2017 | $1,779 | $4,195 | $7,632 | $6,926 | $3,989 |

| 2018 | $2,000 | $4,539 | $7,921 | $6,943 | $3,954 |

| 2019 | $2,230 | $4,889 | $8,215 | $6,949 | $3,894 |

| 2020 | $1,947 | $4,331 | $7,302 | $6,254 | $3,302 |

| 2021 | $2,135 | $4,350 | $6,937 | $5,836 | $3,223 |

| 2022 | $2,692 | $5,309 | $7,781 | $6,134 | $3,305 |

| 2023 | $3,148 | $6,274 | $8,870 | $6,601 | $3,434 |

| 2024 | $3,266 | $6,642 | $9,255 | $6,648 | $3,375 |

| 2025 | $3,493 | $6,961 | $9,600 | $6,795 | $3,445 |

| Change: 2012-2025 | 87% | 134% | 49% | (1%) | (15%) |

Recent trends in credit card debt

Credit card debt has moderated at $1.252 trillion. Still, credit card debt rose in six out of the last eight quarters and now accounts for 6.7% of all debt held by Americans.

New credit card delinquency rates have begun to stabilize, although the overall outstanding credit card balance that's seriously delinquent continues to grow -- a sign that Americans are still leaning on their credit cards to cope with the lingering effects of inflation.

Even as credit card debt and delinquencies rose in 2023 and 2024, the average FICO® Score remained stable at 714.

Credit card utilization held at 29% -- combined with rising delinquency rates and stubborn inflation, there are some worrisome signs about just how much consumers are relying on credit.

How to get out of credit card debt

As these statistics show, owing money to your credit card issuer is common. Many American credit card holders have high balances that cost them interest each month.

If you're in this situation, here are some methods to consider that can help you get out of credit card debt:

- Keep your credit card charges to a minimum. Either don't use credit or only use it for necessary expenses so you don't add to your debt. Since this is revolving debt, it's hard to get rid of if you continue using your credit cards.

- Cut spending where you can. Look at your recent spending, see where you can cut back, and make a budget you can use going forward. There are several budgeting apps that can help here.

- Consider a balance transfer credit card if you have good credit. Balance transfer credit cards offer a 0% intro APR on transferred credit card debt. Although card issuers cut down on these offers at the start of the pandemic, there are now plenty of quality balance transfer cards available, and they're the best credit card option for paying off debt.

- Look into debt consolidation loans. Debt consolidation loans typically have lower interest rates than most credit cards (excluding the 0% intro APR certain cards offer on purchases and/or balance transfers). They also have a fixed payment amount and length, which can provide the structure needed to eliminate credit card debt.

- Explore other options if you can't make your monthly payments. You may be able to negotiate with your credit card issuer to lower your interest rate or monthly payment amount. Another option is to look into nonprofit organizations that offer credit counseling or a credit card hardship program.

-

Sources

- Experian (2026). "Experian 2025 Consumer Credit Review."

- Experian (2025). "Experian Study: Average U.S. Consumer Debt and Statistics."

- Federal Reserve (2026). "Commercial Bank Interest Rate on Credit Card Plans, Accounts Assessed Interest-Federal Funds Effective Rate."

- Federal Reserve (2026). "Quarterly Report on Household Debt and Credit."

- Federal Reserve (2023). "Survey of Consumer Finances."

- TransUnion (2026). "TransUnion Report Reveals Diverging Credit Risk Trends Among U.S. Consumers."

Our Research Expert

Jack Caporal is the Research Director for The Motley Fool and Motley Fool Money and has worked full-time for the company since 2021. Jack leads efforts to identify and analyze trends shaping investing and personal financial decisions across the United States. His research has appeared in thousands of media outlets including Harvard Business Review, The New York Times, Bloomberg, and CNBC, and has been cited in congressional testimony. He previously covered business and economic trends as a reporter and policy analyst in Washington, D.C. He serves as Chair of the Trade Policy Committee at the World Trade Center in Denver, Colorado. He holds a B.A. degree in International Relations with a concentration in International Economics from Michigan State University.

Motley Fool Stock Disclosures

Jack Caporal has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Avalanche and Target. The Motley Fool recommends Flow. The Motley Fool has a disclosure policy.