Average American Credit Card Debt in 2025

KEY POINTS

- Average debt climbs: The average American credit card debt rose to $6,580 in late 2024, a 3% increase from the previous year.

- Household debt insights: The average household carries about $8,940 in credit card debt as of early 2025.

- Utilization remains high: The average credit utilization rate stayed at 29% in 2024, indicating continued reliance on credit.

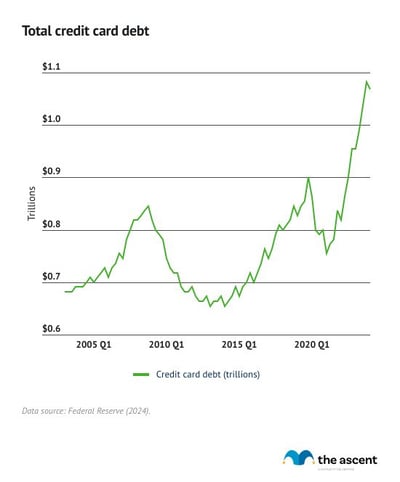

At first glance, credit card debt numbers in the United States look enormous. Consumers owe an astounding $1.182 trillion on their credit cards, and the average American credit card debt balance is $6,580.

We've reviewed research from government agencies and credit bureaus to get the most up-to-date data on U.S. credit card debt. Keep reading for the latest credit card debt statistics.

Average credit card debt

How much credit card debt does the average American have? The average balance is $6,580 as of the fourth quarter of 2024, according to TransUnion. That's a 3% increase from the previous year.

| Quarter-Year | Average Credit Card Debt |

|---|---|

| Q4 2024 | $6,580 |

| Q4 2023 | $6,360 |

| Q4 2022 | $5,805 |

| Q4 2021 | $5,139 |

Total U.S. credit card debt declined to $1.182 in the first quarter of 2025, falling from an all-time high in the previous quarter of $1.211 trillion. While credit card debt fluctuated during the pandemic, it began to steadily rise in 2021 as inflation took off.

Over the last decade, credit card debt has typically accounted for between 5.5% to 6.5% of total household debt.

What is the average American credit card debt per household?

The average American household has about $8,940 in credit card debt, based on the most recent U.S. credit card debt and household data.

Average credit card debt per household was calculated by dividing U.S. credit card debt in the first quarter of 2025 ($1.182 trillion) by the most recent data on the number of households (132.216 million as of 2024). This number is higher than the average credit card debt per borrower because multi-person households are likely to have more than one credit card.

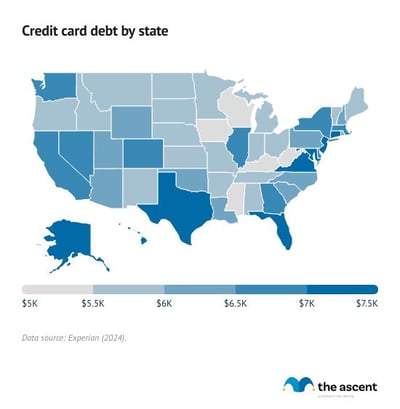

Average credit card debt by state

Alaska has $8,077 in average credit card debt, more than any other state. Kansas and Wisconsin have the smallest average balances at $5,329 and $5,370.

Credit card debt numbers vary quite a bit by state. Here's a full list of each state's average credit card balance as of 2024.

States with the highest credit card debt

- Alaska: $8,077

- Florida: $7,861

- New Mexico: $7,605

- Connecticut: $7,568

- Idaho: $7,560

States with the lowest credit card debt

- Kansas: $5,329

- Wisconsin: $5,370

- Louisiana: $5,399

- West Virginia: $5,427

- Missouri: $5,553

Average credit utilization rate

The average credit utilization rate is 29% as of 2024, level with 2023 and up 1% from 2022.

This metric, also known as a credit utilization ratio, is your credit card balances divided by your credit limits. If you have one credit card with a $1,000 balance and a $10,000 credit limit, then your credit utilization would be 10%.

| Year | Average Credit Utilization Rate |

|---|---|

| 2020 | 25.4% |

| 2021 | 25.5% |

| 2022 | 28.0% |

| 2023 | 29.0% |

| 2024 | 29.0% |

Lower credit utilization is better for your credit score. The conventional wisdom is that you should keep it below 30%, so consumers are doing well managing their credit cards.

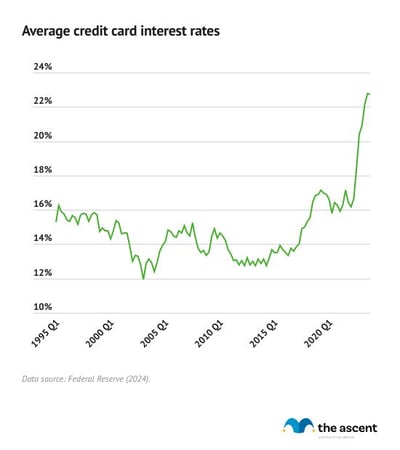

Average credit card interest rates

The average credit card APR on interest-bearing accounts is 21.91% as of the fourth quarter of 2024. Credit card interest rates have risen quickly since 2021, as the Federal Reserve hiked its benchmark interest rate.

Interest-bearing accounts include all credit cards that charge interest. It excludes credit cards that aren't charging interest at that time, so 0% intro APR credit cards don't count until the introductory period ends.

Credit card interest makes up a significant chunk of card issuers' earnings. Interest rates have shot up since 2021 from 15.91% in the first quarter of that year.

READ MORE: How Does Credit Card Interest Work?

Credit card delinquency rates

Data from the Federal Reserve shows credit card delinquencies stabilizing.

The 30-days past due delinquency transition rate for credit cards fell to 8.75% in the first quarter of 2025 from 8.96% in the previous quarter. The serious delinquency rate, in which balances are 90 days or more past due, was 7.04%, down from 7.18%

Overall, 12.31% of credit card balances are 90 days or more delinquent, up from 11.35% in the fourth quarter of 2024. The percentage of outstanding credit card balances that are seriously delinquent has been on the rise since the second quarter of 2022.

Average credit card debt by income

Americans in higher income brackets carry higher credit card balances on average.

However, it's the middle class and the upper-middle class that are more likely to have credit card debt. Among Americans in the 60th through 79th income percentiles, 54% have credit card debt. Those in the 40th through 59th income percentile are more likely to have credit card debt, as 57% carry a balance on their card.

It's the Americans in the highest (90th to 100th) and lowest (under 20th) income percentiles who are least likely to carry balances on their credit cards. A third of Americans in the lowest income percentile carry credit card debt, while a quarter of those in the highest income percentile have credit card debt.

| Income Percentile | Median Annual Income | Median Credit Card Debt | Average Credit Card Debt | Percentage With Credit Card Debt |

|---|---|---|---|---|

| Less than 20% | $20,540 | $1,400 | $3,630 | 33.40% |

| 20% to 39% | $43,240 | $1,600 | $3,840 | 46.40% |

| 40% to 59% | $70,260 | $2,500 | $5,950 | 56.90% |

| 60% to 79% | $115,660 | $3,500 | $7,440 | 54.40% |

| 80% to 89% | $189,160 | $5,000 | $8,900 | 44.60% |

| 90% to 100% | $390,210 | $6,000 | $11,210 | 25.40% |

| All families | $70,260 | $2,700 | $6,120 | 45.20% |

Average credit card debt by race

White Americans have average credit card debt of $6,930 and a median credit card balance of $3,000, the most of any racial identity/ethnicity.

Hispanic Americans have the lowest average credit card debt at $4,150, and both Hispanic and Black Americans share the lowest median credit card debt at $1,700.

| Race/Ethnicity | White, Non-Hispanic | Black, Non-Hispanic | Hispanic | Other | All Families |

|---|---|---|---|---|---|

| Median credit card debt | $3,000 | $1,700 | $1,700 | $2,970 | $6,000 |

| Average credit card debt | $6,930 | $4,360 | $4,150 | $5,910 | $11,210 |

| Percent holding credit card debt | 42.20% | 56.30% | 55.80% | 43.30% | 45.20% |

Average credit card debt by age

Generation X carries the highest average credit card balance at $8,870. That's over $1,000 more than baby boomers, who came in second with an average balance of $6,601.

The lowest average credit card debt by age was Generation Z with $3,148. Since young adults have lower incomes on average, they also have a lower average credit limit, which at least helps with avoiding credit card debt.

| Generation | 2022 | 2023 |

|---|---|---|

| Generation Z | $2,692 | $3,148 |

| Millennials | $5,309 | $6,274 |

| Generation X | $7,781 | $8,870 |

| Baby boomers | $6,134 | $6,601 |

| Silent generation | $3,305 | $3,434 |

Recent trends in credit card debt

Credit card debt has fallen off record highs to $1.182 trillion. Credit card debt rose in two out of the last eight quarters and now accounts for nearly 6.5% of all debt held by Americans.

New credit card delinquency rates have begun to stabilize, although the overall outstanding credit card balance that's seriously delinquent continues to grow -- a sign that Americans are still leaning on their credit cards to cope with the lingering effects of inflation.

Even as credit card debt and delinquencies rose in 2023 and 2024, the average FICO® Score remained stable at 715.

Credit card utilization held at 29% -- combined with rising delinquency rates and stubborn inflation, these are worrisome signs about just how much consumers are relying on credit.

How to get out of credit card debt

As we've seen from these statistics, owing money to your credit card issuer is common. Many American credit card holders have expensive balances that are costing them interest charges every month.

If you're in this situation, here are some methods to consider that can help you get out of credit card debt:

- Keep your credit card charges to a minimum. Either don't use credit or only use it for necessary expenses so you don't add to your debt. Since this is revolving debt, it's hard to get rid of if you continue using your credit cards.

- Cut spending where you can. Look at your recent spending, see if there's anywhere you can cut back, and make a budget that you can use going forward. There are several budgeting apps that can help here.

- Consider a balance transfer credit card if you have good credit. Balance transfer credit cards offer a 0% intro APR on credit card debt you transfer over. Although card issuers cut down on these offers at the start of the pandemic, there are now plenty of quality balance transfer cards available, and they're the best credit card option for paying off debt.

- Look into debt consolidation loans. Debt consolidation loans typically have lower interest rates than most credit cards (excluding the 0% intro APR certain cards offer on purchases and/or balance transfers). They also have a fixed payment amount and length, which can provide the structure needed to eliminate credit card debt.

- Explore other options if you can't make your monthly payments. You may be able to negotiate with your credit card issuer to lower your interest rate or monthly payment amount. Another option is to look into nonprofit organizations that offer credit counseling or a credit card hardship program.

-

Sources

- Experian (2023). "Average Credit Card Debt by Age in 2024."

- Experian (2025). "Experian 2024 Consumer Credit Review."

- Federal Reserve (2025). "Commercial Bank Interest Rate on Credit Card Plans, Accounts Assessed Interest-Federal Funds Effective Rate."

- Federal Reserve (2025). "Quarterly Report on Household Debt and Credit."

- Federal Reserve (2023). "Survey of Consumer Finances."

- TransUnion (2025). "Growth in Originations Expected Across Multiple Credit Products in 2025."

Our Research Expert

Jack Caporal is the Research Director for The Motley Fool and Motley Fool Money.

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. Motley Fool Money does not cover all offers on the market. Motley Fool Money is 100% owned and operated by The Motley Fool. Our knowledgeable team of personal finance editors and analysts are employed by The Motley Fool and held to the same set of publishing standards and editorial integrity while maintaining professional separation from the analysts and editors on other Motley Fool brands. Terms may apply to offers listed on this page.