The relative strength in the price of oil this year has caught many investors by surprise, and it's worth adding an energy-related stock to a diversified portfolio. If you want to do so, then Baker Hughes (BKR -1.38%) -- a supplier of equipment and services to the oil and natural gas industry -- may fit the bill.

Here's why the company would be an attractive choice now for investors looking for energy exposure.

Capital spending discipline

There's no way of getting away from the fact that the prices of energy commodities impact the prospects for nearly all energy companies -- Baker Hughes among them.

The company operates in two segments: oilfield services and equipment (OFSE), and industrial and energy technology (IET). Its revenue from OFSE, which includes construction, production systems, completions, interventions and measurements, and subsea and surface pressure systems, are tied to directly the capital spending policies of the global onshore and offshore oil exploration and production companies.

CEO Lorenzo Simonelli thinks the current spending upcycle could prove more durable than previous ones, and there's evidence to suggest he might be right. First, exploration and production companies have taken a much more disciplined approach to spending than they have in previous upcycles. You can see this in the chart below by comparing each company's capital spending over the last few years to the prior cycle of high oil prices before the slump in 2014.

WTI Crude Oil Spot Price data by YCharts.

Oil demand is growing more than supply

Despite the slowing growth of the global economy and the negative stances certain polities have adopted toward fossil fuels, the latest oil market report from the International Energy Agency (IEA) forecasts that world oil demand will rise by 2.2 million barrels per day (mb/d) in 2023.

However, world supply is only expected to increase by 1.5 mb/d this year. While the outlook for 2024 calls for a more modest 0.99 mb/d increase in demand, decisions by Saudi Arabia and Russia to cut their oil production will support crude prices at high levels.

The U.S. Strategic Petroleum Reserve

At some point in the next few years, the U.S. will need to replenish the Strategic Petroleum Reserve, which has been drawn down by the Biden administration in its efforts to get more supply on the market and reduce energy prices for consumers. This will increase market demand, potentially at much higher prices than when oil was last added to the SPR.

U.S. Crude Oil in the Strategic Petroleum Reserve Stocks data by YCharts

These factors should support crude oil prices at levels sufficient to sustain investment in developing new production, which in turn will drive more OFSE revenue for Baker Hughes.

More than just oil at Baker Hughes

Oilfield services and equipment generated $1.2 billion in segment operating profit in 2022, but the energy technology segment was only slightly behind with $1.13 billion. This segment -- which sells gas technology equipment and services, condition monitoring, instrumentation and controls, pumps, valves, and gears -- is a benefiting from the growing roles of natural gas and LNG as transitional energy sources while the world is en route to an energy future more reliant on renewable and green sources.

In addition, the consistency of natural gas as a power source (in contrast to renewable energy sources, which tend to be intermittent) and its ready availability in parts of the globe where renewable energy will never be a viable option means it will be part of the global energy mix for decades.

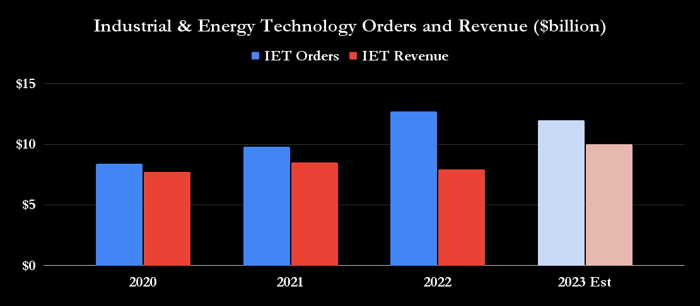

As you can see in the chart below, energy technology orders continue to exceed revenue. Moreover, on the second-quarter earnings call, Simonelli said, "We don't see a material decrease in '24 or in '25" when discussing IET orders." Investors should focus on two areas of particular strength: the company's expected $600 million to $700 million in new energy orders, and its $900 million in LNG orders in the second quarter alone.

Baker Hughes' strength in new energy orders -- carbon capture, carbon compression, hydrogen, storage, utilization -- highlights its potential to profit from the clean energy transition.

Data source: Baker Hughes presentations.

A stock to buy

The combination of upside exposure to oil and Baker Hughes' natural gas technology solutions means it has the long-term potential to continue delivering returns for investors. However, it's probably not a stock that should be held in a concentrated portfolio because the price of oil has historically been volatile.

Still, if you are bullish on the price of oil, or at least think it will stay for some time in the range it has been in this year, and are looking for an investment that gives you exposure to the energy sector, then Baker Hughes is an excellent choice.