2023 has been a year filled with buzzwords surrounding artificial intelligence. And while the growth prospects around AI are exciting, there are plenty of other investment opportunities for those who may not want the added risk of volatile software businesses in their portfolio.

While the Federal Reserve has worked tirelessly to combat inflation, October's rate of 3.2% is still much higher than the Fed's long-term goal of 2%. The consumer discretionary sector, in particular, has been among the hardest hit during this period of high inflation and elevated borrowing costs. This sector has struggled to generate growth commensurate with prior periods, and not surprisingly, constituent stock prices have fallen.

I'm going to break down three Warren Buffett consumer stocks that could represent unique buying opportunities right now. While the growth may not mimic that of high-flying software businesses, each of the companies is a best-in-class brand and pays a dividend. With some on Wall Street calling for a new bull market, now could be a really opportune time to open or add to positions in the stocks explored below.

1. Coca-Cola

On the surface, investors may think that Coca-Cola's best days are behind it. With weight-loss supplements like Ozempic and Mounjaro more popular than ever, you might think more health-conscious consumers would hurt Coca-Cola's business. It's important to remember, though, that Coca-Cola has an enormous portfolio that spans well beyond soda. The company also owns a number of sports and water brands, as well as coffee and tea products. This diversification has helped the company generate strong revenue and profit growth throughout much of 2023.

Through the first nine months of 2023, Coca-Cola reported total revenue of $34.9 billion which represented 6% growth year over year. While the company's revenue growth rate pales in comparison to technology companies, Coca-Cola operates a massively profitable operation. Through September, Coca-Cola reported net profit of $8.7 billion -- up 16% year over year. Investors can see that even though revenue is only growing in the single digits, Coca-Cola is able to exercise disciplined cost measures and not sacrifice its profitability profile. This is really an incredible feat considering consumers have been scaling back on discretionary items while out shopping given the overall pressures from the macroeconomic environment.

The combination of revenue growth and expanding profits allows Coca-Cola to pass on some of the excess capital to loyal investors in the form of a dividend. Coca-Cola has a long history of not only paying a dividend, but growing it. For this reason, the company has earned an esteemed position as a Dividend King.

The chart below illustrates the total return of Coca-Cola stock against the S&P 500 over the last year. It's easy to see that Coca-Cola stock has vastly underperformed the broader markets. But unlike many of its peers, Coca-Cola raised its financial outlook during the Q3 earnings call. Given the company's upbeat financial guidance coupled with it's impressive liquidity profile and long history of paying a dividend, now looks like an interesting opportunity to scoop up shares in the beverage stock at a bargain price, all while generating some passive income for your portfolio.

KO Total Return Level data by YCharts.

2. McDonald's

It's important to clarify that McDonald's stock is not directly in Buffett's Berkshire Hathaway portfolio. Rather, its position is held in New England Asset Management (NEAM), a subsidiary of Berkshire Hathaway. Nonetheless, just like many of Buffett's holdings, McDonald's also pays a dividend and generates steady growth.

Similar to Coca-Cola, McDonald's has shown some real resiliency this year. Through the nine months ended Sept. 30, McDonald's reported total revenue of $19.1 billion, up 11% year over year. The revenue growth coupled with lower operating expenses has fueled meaningful profit growth for the fast food chain, reporting a 50% increase in net income year over year through September.

Yet despite the company's impressive revenue and profit growth, I'd argue that McDonald's stock is overlooked. The chart below shows the forward price-to-earnings (P/E) for McDonald's benchmarked against a cohort of other fast-food chains. It's easy to see that McDonald's' forward P/E of 23.6 trades in the middle of the comparable companies in this dataset. Moreover, as of the time of this article, McDonald's stock price of $280 is essentially in the middle of its 52-week high and low. At its current stock price, now looks like a terrific opportunity to open a position in McDonald's at a 2% yield.

MCD PE Ratio (Forward) data by YCharts.

Image source: Getty Images.

3. Apple

Buffett was long-known to avoid investing in the technology sector. However, back in 2016 the Oracle of Omaha sent shockwaves around the capital markets after he took a position in Apple. Just like Coca-Cola and McDonald's, Apple is one of the most recognized brands in the world and it pays a dividend. In fact, through subsequent purchases and long-term conviction, Buffett earns nearly $1 billion in passive income per year through Apple's dividend. Given Buffett is known for owning stocks for multiple decades, this figure is set to compound even higher over the years.

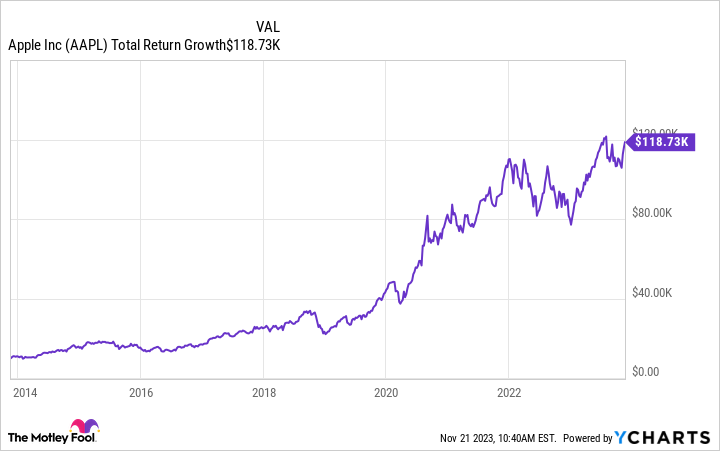

AAPL Total Return Level data by YCharts.

The chart above shows the total return of a $10,000 investment in Apple over the last decade. Total return is an important financial measure as it accounts for the reinvestment of dividends. It's easy for investors to see that this illustrative $10,000 investment in Apple stock has resulted in a multi bagger over the last decade. While this is encouraging to see, there are some risk factors for investors to consider.

Apple has struggled to grow its top line for a couple of years now. Unsurprisingly, during prolonged periods of inflation and high interest rates, consumers aren't necessarily rushing out the door to upgrade their cellphones or hardware devices. In other words, Apple devices could be viewed as more of a luxury than a necessity. Nonetheless, one of the bright spots for Apple right now is its services business. This is one of the only areas of Apple's operation that is currently growing on a consistent basis. The best part about this dynamic is that Services has helped fuel meaningful margin expansion, even when other areas of the business have stalled. Moreover, I believe investors can view Services as the primary thread that stitches together the broader fabric of Apple's ecosystem, and it's largely being overlooked.

The overarching theme here is that holding Apple stock over a long-term horizon has proven to be a good idea. The company continues to find ways to generate growth, and consistently rewards shareholders. While its dividend yield of 0.50% is low, many of Apple's tech cohorts don't pay a dividend at all. To me, the stock is trading at a depressed valuation due to lingering concerns over the company's future growth. But from my purview, I think the sentiment is overblown and the stock is oversold. Inflation should continue to cool down, and interest rates will not remain at current levels in perpetuity. When these things occur, I think Apple will begin to see some more rejuvenated demand. For this reason, I'd dollar-cost average into shares now and plan to hold for the long-term, just like Buffett.