AT&T (T 1.02%) and Verizon Communications (VZ 1.17%) have delivered their 2023 results to shareholders. Although investors had differing reactions to both of these stocks, both reported strong growth in their wireless segments, and since these are two of the three nationwide 5G carriers in the U.S. (T-Mobile is the third), they make up most of its telecom industry.

Additionally, both began as landline providers following the breakup of the original AT&T, and they have followed similar paths to spearhead today's wireless industry. The question is: Which telecom stock will better serve today's investors?

Why investors might consider AT&T

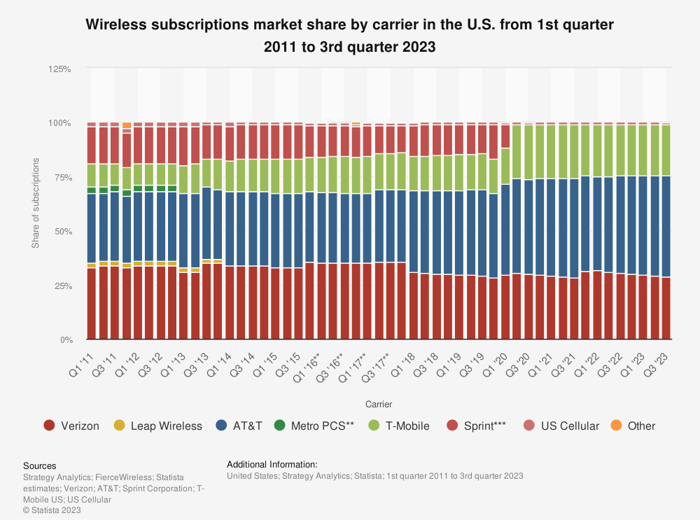

AT&T is the market share leader, and judging by its growth, that lead does not appear to be threatened. In the fourth quarter, AT&T added 526,000 postpaid phone net additions, taking the 2023 total to 1.7 million.

Image sources: AT&T, Verizon, T-Mobile, Sprint, US Cellular, Strategy Analytics, FierceWireless, Statista estimates.

Like its peers, it spends heavily to maintain that business. Capital expenditures amounted to nearly $18 billion in 2023, down slightly from the $20 billion in 2022. That spending, along with some missteps in the cable TV and content businesses, left AT&T with a total debt of $137 billion.

Despite that spending, AT&T generated almost $17 billion in free cash flow. This allowed it to easily cover just over $8 billion in dividend costs. That payout, which amounts to $1.11 per share annually, delivers a 7% dividend yield to shareholders, far above the S&P 500's 1.4% payout. Still, with AT&T walking away from a 35-year streak in dividend increases in 2022, some investors harbor doubts about the payout. The past downtrend in the stock price may also deter some investors.

Nonetheless, AT&T has risen by approximately 25% since its low in July. Additionally, it sells for less than 7 times forward earnings, a likely testament to the high debt levels and the financial challenges it suffered in recent years. But with its discounted valuation and the rapid growth in net additions, investors could finally see a viable growth trajectory.

The case for Verizon

Among the telecom giants, Verizon is seen as the quality leader. It has won the most J.D. Power awards for network quality 32 consecutive times. The telco also reported 449,000 net additions in Q4 and more than 1.7 million broadband customers, meaning it nearly matches AT&T in adding wireless customers.

It also showed its willingness to maintain that quality by spending $53 billion on the C-band spectrum auction in 2021. Since spectrum is the prime real estate of the wireless business, Verizon is well-positioned to maintain that quality lead. Unfortunately, such spending helped leave Verizon with a total debt of almost $151 billion.

Fortunately, despite that burden and $19 billion in capital spending for the year, Verizon generated nearly $19 billion in free cash flow for 2023, enough to fund over $11 billion in dividend costs. That payout, which now stands at $2.66 per share annually, yields around 6.3% and has risen for 17 consecutive years.

Thanks to a dramatic recovery from its October low, Verizon stock rose slightly over the past year. It has increased by over 35% from the low and sells at a forward price-to-earnings (P/E) ratio of 9 even after that gain. Thus, the stock could recover amid robust wireless customer growth and a low valuation.

AT&T or Verizon?

Admittedly, AT&T and Verizon seem to offer few differences. Although both compete for the same customers, they have seen notable growth in mature wireless business. Conversely, both are burdened with heavy debts, and both dividends are likely in danger as the companies look for ways to reduce such obligations.

However, the edge likely belongs to AT&T. Since AT&T has already cut its dividend, it is likely to receive less blowback if it cuts the payout again to reduce debt. Moreover, with its higher market share and lower earnings multiple, it is a less risky choice for prospective buyers.