In the past I've written about why I'm a fan of Williams Companies (WMB 0.96%) and its MLP Williams Partners (NYSE: WPZ), as excellent high-yield long-term investments into America's shale gas boom.

After Williams Companies changed the terms of its merger between Williams Partners and Access Midstream Partners (NYSE: ACMP), I recommended that income investors consider both Williams Companies and Access Midstream for their diversified high-yield portfolios, especially since share prices have slumped thanks to oil prices' worst collapse since the financial crisis.

Charlie Munger -- Warren Buffett's right-hand man at Berkshire Hathaway -- famously said that a key investment principle for investing success is to "Invert, always invert."

In this case that means to ask ourselves not why shares of Williams and Access Midstream are likely to rise in the long term, but why they might fall in the short-medium term. In the spirit of Munger, let's take a look at three things that could go wrong in the near term that might cause shares of these quality energy investments to potentially crash, and what that might mean for investors.

Oil prices could crash further and stay low

While Williams Companies management reiterated its previous payout growth guidance on Oct. 26, since that time, energy prices, oil especially, have declined by 33%, from $83 to $55

While Williams Companies is mostly involved with natural gas, it does currently carry 475,000 barrels of oil per day on its system and has, as part of its $30 billion total project backlog, several projects currently under negotiation that would go online in 2017 to carry oil from the Gulf of Mexico to US refineries on the Gulf coast.

If oil prices remain at depressed levels for a prolonged period of time, there is a chance such projects could be cancelled. This has already occurred with competitor Enterprise Products Partners (EPD 1.69%), which recently cancelled a 1,200-mile oil pipeline that would have carried as much as 700,000 barrels per day from North Dakota's Bakken shale oil fields to Cushing, Oklahoma, where West Texas Intermediate (American oil standard), is priced.

Slowing economic growth depresses natural gas prices and international spreads

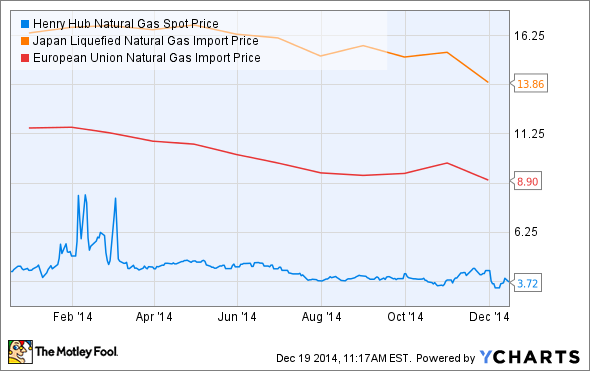

Henry Hub Natural Gas Spot Price data by YCharts

However, a larger threat to Williams is that a decrease in the price differences in Europe and Japan, major liquefied natural gas, or LNG, markets, could threaten U.S. LNG exports, which are expected to be an important growth catalyst for continuing U.S. natural gas production growth. As the above chart shows, natural gas prices in Europe and Japan are currently declining faster than US gas prices. This is compressing the spread (difference between foreign and US gas) which has been a key driver for the demand for US LNG exports. If continued economic weakness in those regions persists over several years, then the demand for U.S. LNG exports could decrease.

For example, Goldman Sachs recently issued a report stating it believes the growth rate of global LNG demand will now be 25% lower through 2025 because of slower economic growth, competition from Chinese shale natural gas production, and Japan restarting its nuclear reactors.

While most U.S. LNG export projects have already secured long-term contracts and should be completed as scheduled, new projects may be put off or cancelled if the foreign prices of natural gas continue to decrease or stabilize for several years below their recent highs. That, in turn, could decrease U.S. gas production growth and decrease the demand for many of Williams Companies and Access Midstream's current and proposed growth projects.

That might result in Williams and Access missing their dividend and distribution growth projections, which might place additional downward pressure on share prices.

How likely are energy prices to remain low?

The current decline in energy prices has a lot to do with fears of slowing demand growth due to a weaker global economy.

For example back in August Germany--Europe's largest economy--announced its worst manufacturing contraction since the financial panic.

The contraction in its export fueled manufacturing sector has resulted in Germany's GDP growth grinding to a halt, with the last two quarter's growth figures coming in at -.2%, and .1%, respectively. France, the Euro zone's second largest economy, reported similarly bleak growth of just -.1% and .3% respectively, for the last two quarters. Meanwhile Japan, the world's third largest economy and a key oil importer, reported its worst second and third quarter GDP growth since the financial panic, of -7.3% and -1.9%, respectively. This was following a 60% increase in its national sales tax, from 5% to 8%.

China, the key oil demand growth catalyst of the last few years, reported its economy grew at its slowest rate in five years, 7.3% last quarter, down from 7.5% growth the quarter previous.

All told, these areas of economic weakness have caused the International Monetary Fund to revise down its 2014 and 2015 global economic growth forecasts by 11%, and 5%, respectively.This in turn has resulted in the International Energy Agency cutting its oil demand growth projections for 2015 by 21%, or 230,000 barrels/day. While that may not sound like much, keep in mind that the recent 50% plunge in oil prices has been a result of an approximately 1.1 million barrel/day (1.2%) oversupply in world oil markets.

With non-OPEC oil production, led by US shale producers, expected to grow by 1.3 million barrels per day in 2015, oil prices may continue to feel pressure unless OPEC decides to cut production during its next meeting on June 5. Due to OPEC nations requiring between $58/barrel and $136/barrel to balance their budgets, I believe such a cut is likely. However, if OPEC decides to maintain production as part of its war for market share with US shale producers, oil prices could remain depressed throughout the rest of the year.

While the recent decline in energy prices have been extremely painful in the short-term, I continue to be optimistic about oil and gas's upwards pricing prospects over the next two decades. Thus I still recommend Williams Companies and Access Midstream Partners as two excellent, high-yield income options for any diversified income portfolio. However, current and potential investors should be aware of the short-medium term risks discussed above and adjust their allocations into these investments accordingly.