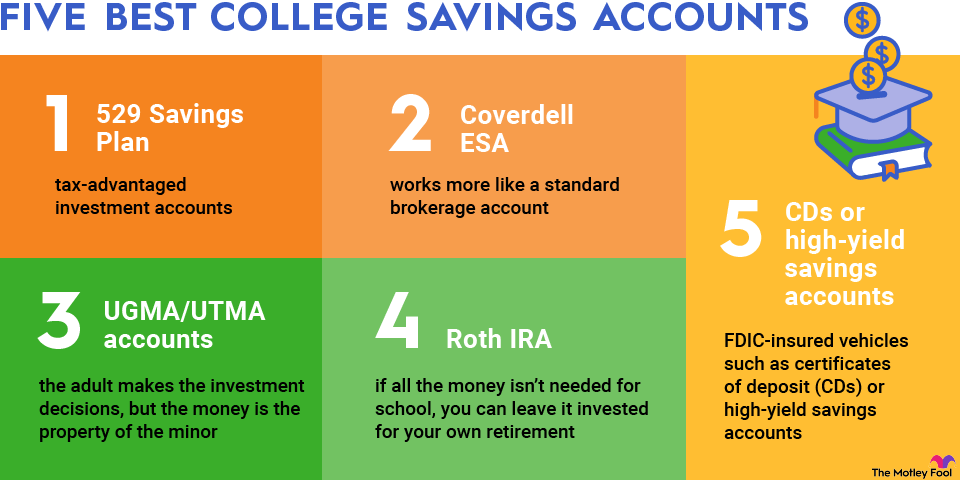

2. Coverdell ESA

A Coverdell Education Savings Account, or Coverdell ESA, is the other major type of education-specific investment account. Unlike a 529, which functions like most workplace retirement plans, a Coverdell works more like a standard brokerage account. You can open a Coverdell through many popular brokers, and you can use money in a Coverdell to invest in stocks, mutual funds, exchange-traded funds (ETFs), bonds, and more.

Coverdell ESAs have a similar tax structure to 529 savings plans. Contributions aren't deductible, but you don't have to pay tax on dividends or capital gains each year, and qualified withdrawals are tax-free.

This investment flexibility is the main advantage of using a Coverdell. With a 529 savings plan, you are limited to the plan's "menu" of investment options. With a Coverdell, if you want to invest some of your college savings in, say, Apple (AAPL +3.52%) stock, you can certainly do it.

The biggest drawback to a Coverdell ESA is the contribution maximum of just $2,000 per year. This limit applies per beneficiary, not per account. In other words, if you and your child's grandparents both open Coverdell accounts for your child, the combined contributions can't exceed $2,000 per year. And, if your income exceeds a certain threshold, the ability to contribute at all phases out -- for 2025 and 2026, the contribution phase-out starts at a modified gross adjusted income of $190,000 for married couples filing jointly and $95,000 for other taxpayers.

Advantages of using a Coverdell ESA

- Money in a Coverdell ESA can be invested in virtually any stock, mutual fund, or ETF you want.

- Coverdell ESAs can be easily opened through most major online brokerages.

- Investments in a Coverdell ESA grow tax-free, and qualifying withdrawals are completely tax-free.

Potential drawbacks of a Coverdell ESA

- Only $2,000 can be contributed to a Coverdell ESA per beneficiary, per year.

- Money in a Coverdell ESA must be used for qualifying educational expenses or face a penalty.

- Contributions to a Coverdell ESA are not deductible on state or federal tax returns.

3. UGMA/UTMA accounts

Two account types that can be especially useful for college savings are Uniform Gift to Minors Act (UGMA) and Uniform Transfer to Minors Act (UTMA) accounts.

These accounts work just like standard brokerage accounts. You can put money in a UGMA or UTMA and invest it just like you would your own investment portfolio, in stocks, bonds, mutual funds, ETFs, etc. But these accounts allow adults to invest on behalf of minors. They are also known as custodial accounts since the adult has the ability to make investment decisions, but the money is technically the property of the minor. Depending on the account terms, the minor is given control of the money when they reach the age of 18 or 21.

This can be both a good thing and a bad thing. Keep in mind that although you may have set aside money specifically for college, your child can choose to use the money for whatever they want after they reach the age of maturity for the account. Furthermore, money in a UGMA or UTMA can have negative implications for financial aid, as assets owned by the child are weighted more heavily in the expected family contribution formula than those owned by the parent.

Advantages of using a UGMA or UTMA account

- Money in a UTMA or UGMA can be invested in virtually any stock, bond, ETF, or mutual fund.

- UGMA or UTMA funds can be used for any purpose the account beneficiary wants, not just education.

- A UGMA or UTMA can be a way to give money to a minor and avoid estate tax implications (up to $19,000 per year in both 2025 and 2026).

Potential drawbacks of a UGMA or UTMA account

- The account beneficiary can choose to use the money in a UGMA or UTMA account for any purpose they desire, not just education.

- Money in a UGMA or UTMA becomes the legal property of the beneficiary, not the person who contributed the funds, and can have negative implications for financial aid eligibility.

- There are no tax advantages associated with a UGMA or UTMA account.

4. Roth IRA

It might sound odd to suggest using a Roth IRA as a college savings account, but it could make more sense than you think.

For starters, there is a special exemption that allows IRA account holders to withdraw money penalty-free to pay for qualified higher education expenses. And a Roth IRA has the same general tax structure as a 529 savings plan or a Coverdell ESA -- money is contributed on an after-tax basis, and investments within the account grow and compound tax-free.

There are several benefits to using a Roth IRA for college savings. For one thing, you have more investment flexibility than a 529 since you can invest in any stocks, ETFs, mutual funds, or bonds you want. And with an annual contribution limit of $7,000 in 2025 and $7,500 in 2026 ($8,000 and $8,600, respectively, if you're 50 or older), you can put more money in than with a Coverdell.

Additionally, one of the significant drawbacks to using a 529 or Coverdell account is that the funds must be used for education, or you'll face a substantial penalty for withdrawing them. And with a UGMA or UTMA, the money becomes your child's property, whether they need it for college or not. By using a Roth IRA to save for college, if your child doesn't need all the money to pay for school, you can simply leave it invested for your own retirement.

Advantages of using a Roth IRA

- Roth IRAs have the same general tax structure as 529 plans and Coverdell ESAs, but the money doesn't have to be used for education.

- If your kids don't need the money for college, you can simply use it for your own retirement.

- Money in a Roth IRA can be invested in virtually any stock, bond, ETF, or mutual fund you want.

Potential drawbacks of a Roth IRA

- No state tax deduction for contributions.

- If not used for college, there are a few ways to withdraw money before retirement age.

- Contributions are limited to $7,000 in 2024 and 2025 ($8,000 if you're 50 or older).

5. CDs or high-yield savings accounts

If you don't like taking risks, you can choose to put some or all of your college savings in risk-free, FDIC-insured vehicles such as certificates of deposit (CDs) or high-yield savings accounts. These can be an especially attractive option when the stock market is volatile, and we're in a relatively high-interest-rate environment.

These aren't just for risk-averse savers. Even if you are a rather aggressive investor, it can make sense to move some of your college savings into CDs or savings accounts as your child gets close to college age. After all, it's one thing to deal with a 25% drawdown in your investments when your child is 5 years old. It's quite another to deal with large investment losses when your child needs tuition paid in a few months.