Updated

Buying a home in Ohio can be a long and complicated process. Our Ohio mortgage calculator will help you understand what your monthly mortgage payments will be. This tool will also give you a breakdown of your potential mortgage payment.

Buying a home in Ohio can be a long and complicated process. Our Ohio mortgage calculator will help you understand what your monthly mortgage payments will be. This tool will also give you a breakdown of your potential mortgage payment.

Ohio housing market 2022

Like many parts of the country, Ohio home buyers are facing tough times trying to find the house of their dreams. Although the median sales price for a single family home only rose year over year to 3.4% in July 2023 to $250,300, housing supply remains incredibly thin. Ohioians only have about two months of supply to choose between, with the number of homes for sale dropping 24.8% year over year in July 2023 to 32,173.

Although relatively affordable, housing is still selling for above asking price, with the average home selling for 100.3% of the asking price in July 2023. Despite a much more affordable housing market, Ohio is still an incredibly tough one with a lot of stiff competition. In this kind of climate, it's more important than ever to use one of the best rated mortgage lenders to help home sellers see how serious you are about your offer.

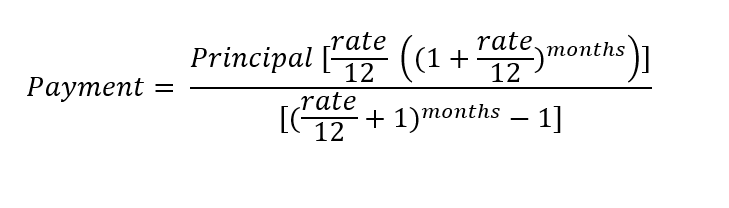

How do I calculate my mortgage payment?

We recommend using a mortgage calculator for Ohio. The formula to calculate by hand is quite complex. It looks like this:

Mortgage rates have risen significantly in the last year, and may continue to rise. It's more important than ever to secure the best mortgage rate possible when you're buying your home. To calculate your monthly mortgage payments in Ohio, you'll need to enter in your estimated mortgage loan amount, the term of your loan, and the rate you think you'll be eligible for.

The term of your loan is the number of years you have to repay your mortgage. Keep in mind the higher your credit score, the more likely you'll be to get the most competitive rate available. The mortgage calculator for Ohio also has an option to enter your down payment amount. The more you put down, the less you will need to borrow and your monthly mortgage costs will be lower.

What other costs do I have to pay?

There are other monthly expenses you'll need to account for, like homeowners insurance and property taxes. When you use our mortgage calculator for Ohio, remember that property taxes paid as a percentage of owner-occupied homes are 1.36% on average. Ohio is ranked 22 out of 50 for property taxes in the country, squarely in the middle. Property taxes may change based on your county.

Homeowners may also be part of a homeowners association (HOA) and have to pay a monthly HOA fee on top of their mortgage payments. HOA fees usually cover the maintenance of common areas, and often include services like trash pickup. To enter these additional costs into the above mortgage calculator for Ohio, just click "Additional inputs" (below "Mortgage type").

You may also need to account for private mortgage insurance (PMI). Homeowners will have to pay PMI if they don't make at least a 20% down payment on their home. With all these potential costs, it is helpful to use our Ohio home loan calculator. Our tool will help break down your costs so you can see what your monthly mortgage payments will look like in different scenarios. If you want to refinance an existing mortgage, our Ohio mortgage calculator can also help you determine your monthly payment -- and you can check out our list of the best refinance lenders to get that process started.

Things to know before buying a house in Ohio

Before you buy a home in Ohio, it's important to make sure you have your finances in order. You will need:

- A good credit score

- A low debt-to-income ratio

- A steady source of income

- A down payment saved

- Additional money outside of your down payment to cover ongoing maintenance, repairs, and other emergencies

There are also some specific issues you should be aware of when buying a home in Ohio. The state has five distinct natural regions: the Lake Plains, Till Plains, Unglaciated Appalachian Plateau, Glaciated Appalachian Plateau, and the Lexington Plain. Due to its proximity to major rivers and being in the Midwest, Ohio is susceptible to flooding and tornadoes.

Ohio also boasts four of Realtor.com's top 25 housing markets for 2023: Toledo (No. 10), Columbus (No. 14), Cincinnati (No. 19), and Dayton (No. 23). These markets are ranked by sales and price growth.

Tips for first-time home buyers in Ohio

Here are some important tips for first-time home buyers to help them navigate the process. There are several programs available for first-time home buyers through the Ohio Housing Finance Agency (OHFA). OHFA offers conventional mortgage loans designed especially for home buyers with low- and moderate-incomes.

OHFA allows home buyers to choose either a 2.5% or 5% down payment of the home's purchase price. Assistance can be applied toward down payments, closing costs, or other pre-closing expenses. This assistance is forgiven after seven years.

To qualify for the OHFA Your Choice! Down Payment Assistance program, home buyers will need a minimum credit score of 640, meet income and purchase price limits, and meet debt-to-income ratios for the loan type.

First-time home buyer loans and programs

Here are other first-time home buyers programs to consider and explore:

- FHA loans are mortgages back by the Federal Housing Authority and require a 3.5% down payment.

- VA loans are for military service members and require a 0% down payment.

- USDA loans are government-backed loans for eligible properties and require a 0% down payment.

- Fannie Mae and Freddie Mac are conventional loans that require a 3% down payment.

Decide on a home-buying budget

Once you have decided on the best mortgage program and have shopped around with different lenders, it is important to decide on a home-buying budget. Many experts recommend that your monthly house payment (including additional costs) be no more than 30% of your monthly income.

It is also important to maintain a good credit score, so don't apply for any credit cards or other loans right before your house search. Credit report inquiries will impact your credit score. You should also have enough money saved for closing costs. Other fees such as loan fees, inspections, and processing costs are not usually covered by the loan.

Read more: Best mortgage lenders for first-time home buyers

Still have questions?

Here are some other questions we've answered:

FAQs

-

If you qualify for down payment assistance through OHFA, you won't need to come up with a down payment at all. Similarly, if you get a VA or USDA loan, you can often do so with no down payment required. Otherwise, you'll need a minimum of 3% down for a conventional mortgage loan, or 3.5% for an FHA mortgage.

-

If you're buying a home that's new to you in Ohio, you can expect to pay an average of $4,223 to close it. However, if you're simply refinancing, the average drops to $2,091.

Our Mortgages Experts

David S. Chang, ChFC®, CLU® is an award-winning entrepreneur, keynote speaker, author, and consultant. He has over two decades of experience in the wealth management space and has been featured in dozens of news, radio, and podcast programs nationwide. He currently works as Head of IoT for the West Region of a Fortune 200 company. He is a graduate of the United States Military Academy at West Point and currently a Lieutenant Colonel in the California Army National Guard. He is an East-West Graduate Degree Fellow and has an MBA from the UCLA Anderson School of Management.

Kristi Waterworth has been a writer since 1995, when words were on paper and card catalogs were cool. She's owned and operated a number of small businesses and developed expertise in digital (and paper) marketing, personal finance, and a hundred other things SMB owners have to know to survive. When she's not banging the keys, Kristi hangs out in her kitchen with her dogs, dropping cheese randomly on the floor.

Eric McWhinnie has been writing and editing digital content since 2010. He specializes in personal finance and investing. He also holds a bachelor’s degree in Finance.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent, a Motley Fool service, does not cover all offers on the market. The Ascent has a dedicated team of editors and analysts focused on personal finance, and they follow the same set of publishing standards and editorial integrity while maintaining professional separation from the analysts and editors on other Motley Fool brands.

Please note that this calculator is not personalized financial advice and should not be considered or used as such. Nor are we promising that by use of this calculator, will you be able to save more money, preserve wealth, or otherwise.

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Kristi Waterworth has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.