Published April 22, 2024

Corporations are powerful and complex business structures. Find out what it takes to incorporate your small business.

For years, the LLC and S corp have dominated small business startups. But with the corporate tax rate cut to 21%, starting a corporation makes financial sense for more small businesses. What are the advantages of doing so, and how do you file for incorporation?

Overview: What is a corporation?

A corporation is a legal business entity formed by filing articles of incorporation with the state. It is governed by a board of directors and owned by shareholders.

Corporations may be publicly held, with shares sold to the public at large, or privately held, with stocks issued to select individuals. Most small business corporations are private companies.

Incorporating takes your business to the next level, providing permanence, access to investment capital, stability, and legal protections. This article walks you through the steps involved in legally forming a corporation.

How to start a corporation in 14 steps

Starting a business as a corporation takes careful planning and documentation. These 14 steps cover the process from ideation to maintenance.

Step 1: Write a business plan

If you're thinking of incorporating, you may already have a thriving business and a strategic plan. But incorporating requires a different level of planning and even a new way of looking at your business.

Up until now, your business has been yours to direct, finance, and control, whether on your own or as part of a close-knit team. Incorporating means turning over the keys and giving your business a life of its own.

It allows your business to reach new heights, but it requires thoughtful planning.

Before incorporating, you need to consider these questions:

- Who will your initial board of directors and officers be, and what powers will they have?

- What is the equity basis of initial owners and investors?

- Do you need investment capital, and where will you turn for it?

- How will shares be issued, and how will they be divided among your startup team?

- How and when will profits be distributed?

- What is your vision for the future of the corporation in one, five, and ten years?

Once your team agrees on these issues, you can create a unified plan for the next phase of your business's life.

Step 2: Choose a home state

Many businesses choose to incorporate in states with business-friendly laws, regulatory environments, and taxes. Delaware and Nevada are prominent examples. It is simpler, however, to form a corporation in the state where your business is headquartered.

You may want to consult with your legal and financial advisors before deciding where to register your business.

Step 3: Register your name

Before proceeding to business registration, you need to select a business name, known as a "doing business as" (DBA) or fictitious name, that is permitted and available in the state where you plan to register.

States restrict the use of certain words based on your business type. For example, words such as trust and fidelity are often restricted because of their association with banking or insurance.

You'll also need to conduct a name availability search to ensure that your chosen name isn't already taken in your state. You can generally conduct a name search in minutes through your state's online business portal, usually housed under the secretary of state or department of commerce.

Even if your business already has a name, you'll need to conduct research and potentially register a new one. States have rules governing use of corporate designators, suffixes such as Inc. and Corp., that signify your business type.

Be sure to follow your state's naming laws to the letter on all official documents now and in the future. States have been known to reject official documents over something as simple as leaving the period out of Corp.

In most states, you can reserve and register your business name online by submitting a brief form and paying a small fee.

Access your state's online business portal for business registration resources. Image source: Author

Step 4: Appoint directors and officers

Under state laws, you can create a corporation of one, with yourself as board, chief executive officer, and sole stockholder. Most corporations, however, involve multiple owners.

A corporation is governed by a board of directors who have a fiduciary duty to make decisions in the interest of the business and its shareholders. The board of directors elects officers who manage the company, such as a chief executive officer and chief financial officer.

Step 5: Write corporate bylaws

Your corporation's bylaws set forth how your business will be managed. They typically include:

- Company information: Include the name, principal business address, and other identifying information of your company.

- Officers and directors: List your initial officers and board members, including the minimum number required to run the business, if any.

- Annual meetings: Establish the frequency, rules, and purposes of corporate meetings. All corporations must hold a shareholder's meeting and a board of director's meeting at least annually.

- Stock classes: Outline the classes of shares and how they will be issued.

- Voting rules: State how and when votes will be taken and how many members are required to create a quorum (the minimum number of board members who must agree to a decision).

- Board membership: Set terms and conditions of board membership. In most corporations, board members serve for one year, but you can set terms and succession plans to meet your needs as long as they conform to your state's regulations.

- Disputes: Create procedures for how disputes will be resolved. Do you want to require mediation of certain disputes? Who has the power to call ad hoc board meetings, and for what reasons?

- Conflicts of interest: Your company needs a formal policy for addressing instances when a director or officer has private interests that conflict with their duty to the business.

Step 6: Draft a shareholder's agreement

A corporate shareholder's agreement establishes how your business will be owned and financed. It addresses issues such as:

- Sale or transfer of shares: Identify who may become a shareholder and how shares may be transferred or sold.

- Valuation of shares: Spell out initial value of shares and what methods you will use to measure value over time.

- Initial ownership: Confirm the initial owners of the corporation, their shares, and their equity basis in the company.

- Voting rights: Establish the voting rights that accompany shares.

- Succession: Consider how shares will be handled if an officer or director leaves, retires, or dies. Many companies give existing shareholders the right to buy out departing owners.

- Dividends and distributions: Consider how and when profits will be distributed.

Step 7: Appoint a registered agent

As part of business registration, you must appoint a registered agent to accept official documents such as notices of lawsuits (service of process). The agent must be available at a physical office location during regular business hours to sign for documents and forward them to the appropriate person in your company.

Technically, anyone who meets the requirements can serve as your agent, but for a reasonable fee, you can get a professional registered agent service that provides reliable document handling in every state. Attorneys also frequently serve as registered agents.

Step 8: File articles of incorporation

Once you've created those founding corporate documents, you're ready to create your business entity by filing articles of incorporation with the secretary of state. The articles contain basic information such as:

- The name, address, and purpose of your business.

- Names and contact information for directors and officers or the people filing for incorporation (incorporators).

- The name and address of your registered agent.

- The corporation's duration.

- The value, number, and classes of shares to be issued.

In many states, you can submit the application through your state's online business portal along with required founding documents and a filing fee. In some, you must mail or deliver paper documents, including multiple copies. Read the filing instructions carefully to avoid rejection.

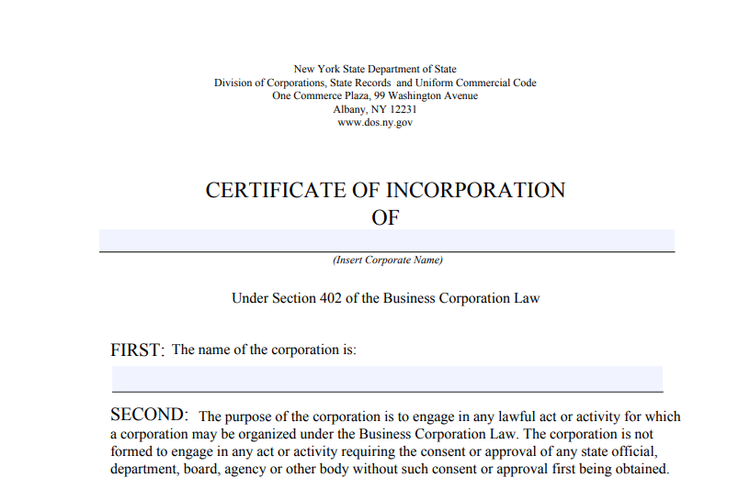

Fees for incorporation generally range from $50 to $200. When your application is approved, the state will send you a certificate of incorporation for your permanent corporate records.

Once your application is approved, the state will issue a certificate of incorporation such as this one from New York. Image source: Author

Step 9: Get tax identification (ID) numbers

Your business will need an Employer Identification Number (EIN). This is your federal identification number for taxes and other government documents. You can apply for one for free using the official IRS EIN tool.

Your corporation may also need to apply for state and local tax IDs for managing sales, franchise, payroll, and other taxes.

Step 10: Hold an initial board meeting

Corporations are required to hold annual shareholder and board of directors meetings and keep meeting minutes in their permanent corporate records.

At the initial meeting, the incorporators usually elect the initial board of directors and turn over control of the company to them. They also ratify the company's shareholder agreement and bylaws.

Step 11: Issue stock

In your founding documents, you outlined the number of shares your corporation would issue and their face (par) values. You now need to issue them according to your agreement.

Some companies issue paper stock certificates, which may be provided as part of a corporate records kit or purchased from an office supply store. Other companies rely on electronic ledgers to issue and track shares.

Step 12: Open a bank account

A corporation is a separate legal entity with assets, debts, and liabilities of its own. Even if you're a corporation of one, all corporate transactions should be managed through the corporation's bank account.

To open an account, you will need much of the documentation you've assembled, including your EIN and certificate of incorporation.

Step 13: Obtain licenses and permits

If your business is a regulated profession such as architecture or construction, or if you will engage in regulated activities such as selling alcohol, you may need to apply for licenses or permits.

You may encounter different requirements at the state, county, and municipal levels, so be sure to check the requirements thoroughly.

Generally, you can apply for business licenses and pay required fees online. Many licenses and permits must be renewed periodically.

Step 14: Create a compliance program

Corporations have continual compliance requirements beyond conducting annual meetings. To ensure that tasks don't fall through the cracks, it's best to appoint one person in your company who is responsible for managing compliance.

Examples of corporate compliance duties include:

- Conducting meetings as required

- Keeping accurate meeting minutes

- Completing corporate tax returns and paying all required taxes

- Filing annual reports with the secretary of state to keep the state apprised of any changes in your business

- Renewing business licenses

- Maintaining corporate records required by state and federal laws

- Maintaining your registered agent

Benefits and disadvantages of starting a corporation

Does incorporation make sense for your business? Consider these benefits and drawbacks:

Benefits of forming a corporation

- Investor capital: The ability to issue shares, and the gravitas that comes with incorporation, make it easier to access capital.

- Permanence: Corporations are structured to endure for generations.

- Formal structure: All that added setup means you have an infrastructure of support and stability to carry your plans forward.

- Legal protection: Your liability for a corporation is limited to the amount you have invested in it.

Disadvantages of forming a corporation

- Complexity: Their robust management and ownership structures also make corporations complicated to create and maintain.

- Double taxation: Corporate profits are taxed at the corporate level, and then taxed again at the personal level when distributed to shareholders.

- Expensive: It takes substantial legal and financial support to create and run a corporation, which can be costly.

- Dispersed control: By incorporating, owners cede power to board members and shareholders.

Built to last

For all their complexity, corporations are a powerful structure built to support endless growth and sustain an enduring legacy. If you're envisioning big things for your small business, incorporation is an exciting and worthwhile milestone in your entrepreneurial journey.

Our Small Business Expert

Elizabeth Gonzalez is a legal and regulatory writer with more than seven years of experience as a contributing editor for HR Specialist and BLR’s HR Insights. She is also a content strategist, web copywriter, and fiction writer with publications ranging from Engineering News-Record and Construction Business Owner to Best American Nonrequired Reading.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

The Motley Fool has a disclosure policy.