The Ascent Guide to Tax Shields for Small Businesses

When Randy Moss was asked how he would pay a fine for excessive celebration, he responded with a now-famous retort: “Straight cash, homie.” Small business owners should keep his words in mind as they go about their work.

The measure of success for a business is operating cash flow. You can stay within the rules of accounting and make net income whatever you want it to be on paper, but you can’t manipulate cash on your financials in the same way.

However, you can adopt certain strategies to increase or decrease your cash flow. One way to increase cash flow is by using tax shields to reduce the net income you report to the IRS and decrease your tax owed. In this article, we’ll go over why you should use tax shields and several types you can use now.

Overview: What is a tax shield?

Tax shields are any tax deductions that allow a business to avoid taxes. While technically any business expense enables you to reduce your taxable income, in this article, we'll discuss several strategies that allow you to decrease your taxes but that don’t affect your business operations.

Keep in mind we’re talking about tax avoidance, not tax evasion. Tax avoidance means using the existing rules to legally reduce your business's taxable income and avoid certain taxes. Tax evasion is a form of fraud where you lie about your taxable income, and it’s illegal.

The tax shield formula

Before we get started, let’s review the tax shield equation. It shows us the taxes we're avoiding with the shield:

Tax Shield = Expense x Tax Rate

For example, if you have depreciation of $100 and a tax rate of 21%, the tax your business is shielded from by the depreciation is $21.

Benefits of tax shields

Here are a few reasons your business should take advantage of tax shields.

1. Lower taxes now

The most obvious reason is simply to pay lower taxes now. The tax shield approach will decrease taxable income and decrease the tax you owe. Remember, when you use tax shields like depreciation, the taxes are deferred, not avoided, so they'll eventually need to be paid.

2. Cash flow for growth

By avoiding taxes, even if just in the short term, you allow your business to reinvest that cash flow to grow. In a business with consistent growth, it makes sense to defer taxes because, when they come due, revenue has grown, and the tax payment will make a lower impact, relatively speaking.

3. Lower taxes forever

The best benefit is avoiding taxes forever. This can be done with a few of the tax shields below, such as interest and hiring your kids. With these shields, the tax is avoided, but there's no deferral.

Types of tax shields

Here are seven tax shields you can realistically take advantage of in your business.

Type 1: Depreciation

You may have heard of tax shield depreciation in connection with your residence. When you buy capital assets over a certain dollar value (chosen by the business), they cannot be expensed. Instead, the value is depreciated over the useful life of the asset, and that expense is deducted on the tax return.

You can also choose to accelerate depreciation by expensing the entire amount for some items in the first year or using the IRS modified assets cost recovery system to increase the percentage deducted in early years.

Amortization is like depreciation for intangible assets, such as expensive software programs or the expenses to get a patent approved. Amortization can also be deducted on the tax return.

Type 2: Interest

An interest tax shield saves you money by using debt instead of further investment. If you invest in a new project with business cash or a capital contribution, the full amount of return on that investment is taxed.

By using debt, you put less equity into the transaction, and the interest paid on the debt shields the return from taxes.

Type 3: Net operating losses

Nobody wants net operating losses, but they can serve as a tax shield if you carry them forward from year to year. If your business experiences a loss, that loss may be carried over into the future to cancel out the income earned in those years.

Type 4: Charitable donations

You may have heard that a large charitable donation was “just a tax write-off.” This is partially true, since donating to approved charities can be written off of business taxes. However, keep in mind that, based on the tax shield formula, the tax shield is just the donation multiplied by the tax rate.

You shell out the full amount of the donation in cash and shield 21% (the current business tax rate) of that amount from tax.

Type 5: Avoid using a C corporation

C corporations are taxed at the business level, and distributions, or dividends, to owners are taxed at the personal level. This phenomenon is known as double taxation, since the income is taxed twice.

S corporations and general partnerships are not taxed at the business level. Instead, income passes through to the owners and is taxed at their personal tax rate.

Type 6: Use fringe benefits

Some of the fringe benefits you offer to employees increases their total compensation but does not increase your payroll taxes.

For example, the employer portion of health insurance premiums and 401(k) contributions, education assistance, and even a portion of transportation and meals can be offered to employees tax-free.

If you are a sole proprietor, consider allocating pre-tax profits to a 401(k) plan or a health savings account.

Type 7: Hire your kids

If you have kids under the age of 18 but old enough to work, you can hire them to do menial tasks and pay them a reasonable amount of tax-deductible wages

The key word here is "reasonable" -- if you pay your 15-year-old son $350,000 per year to shred documents on Saturday, the IRS won’t be happy. Another benefit of this strategy is that you won’t have to pay FICA taxes on the child until they turn 18, or FUTA until they turn 21.

An example of using an interest tax shield

Let’s take a look at how a debt tax shield works. Kelsey’s Killer Key Lime Pies is considering buying new equipment to accelerate the key lime pie manufacturing process. Right now, the store can keep up with local demand, but Kelsey’s social media presence has massively increased the amount of online orders.

If she buys the new equipment, Kelsey can make an extra $5,000 per month (that’s a lot of pies). The equipment would cost $75,000, and she has the cash for it. But, Kelsey could also get a loan with a 7% interest rate, 20% down and a seven-year term.

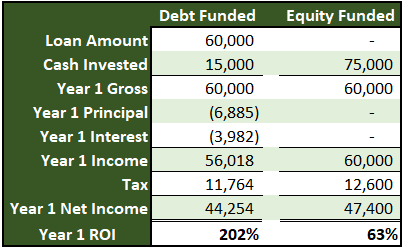

The Year 1 ROI is far higher using debt to fund the purchase. Image source: Author

In this example, the year one ROI for a debt-funded purchase makes the decision look easy. Tax is almost $1,000 less on the year because of the debt shield, and the net income of $44,254 is more than double the cash down payment plus principal.

These numbers don’t tell the whole story, though. We need to see what the numbers look like over the life of the loan.

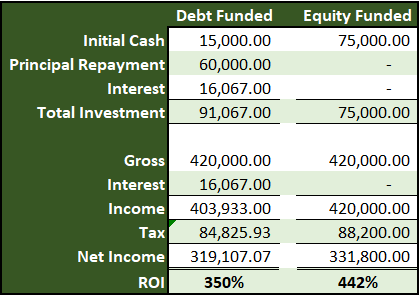

The equity funded alternative has a higher ROI over the life of the loan. Image source: Author

Over the long term, the picture changes. Over the life of the loan, the interest on the debt costs $16,067, which shields Kelsey’s from $3,374 ($88,200 - $84,825.93) in taxes. It's nice to not pay $3,374 in taxes, but that isn’t worth shelling out $16,067 in interest.

While the tax shielding impact of interest is part of the equation, Kelsey needs to make her decision based on multiple factors, the foremost of which is timing. She’ll pay $16,067 more to finance the transaction with debt, but is that worth it if it's over seven years?

If her business is growing, she could have far better uses for the extra $60,000 it would take to pay for the equipment with cash.

To shield or not to shield

Now that you know how to use them, don’t spend all your time calculating tax shields. Most require significant expenses that need to be considered along with other factors. If you use good tax software, it will automatically prompt you to use the best deductions and strategies.

Alert: our top-rated cash back card now has 0% intro APR until 2025

This credit card is not just good – it’s so exceptional that our experts use it personally. It features a lengthy 0% intro APR period, a cash back rate of up to 5%, and all somehow for no annual fee! Click here to read our full review for free and apply in just 2 minutes.

Our Research Expert

Mike Price is an SMB accounting expert writing for The Ascent and The Motley Fool.

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent, a Motley Fool service, does not cover all offers on the market. The Ascent has a dedicated team of editors and analysts focused on personal finance, and they follow the same set of publishing standards and editorial integrity while maintaining professional separation from the analysts and editors on other Motley Fool brands.

Related Articles

View All ArticlesBy: Ben Gran | Published on Jan. 26, 2024

By: Steven Porrello | Published on Feb. 28, 2024

By: Ben Gran | Published on Feb. 27, 2024

By: Maurie Backman | Published on Feb. 27, 2024

By: Chris Neiger | Published on March 2, 2024