AT&T (T -0.17%) has continued on a downward slide. Massive debt levels and the end of a 35-year streak of dividend increases rattled investors, and its dividend yield of 7.7% failed to stem the selling.

However, the stock has attained a low price-to-earnings (P/E) ratio amid a growing customer base. Also, with the stock trading at levels first seen decades ago, it might be time to start adding positions.

The state of AT&T stock

Admittedly, investors have good reasons to hesitate about AT&T. The total debt level, which now tops $143 billion, is a tremendous burden despite the company's $116 billion book value. And even if AT&T allocated its total free cash flow -- which was $5.2 billion in the first half of the year -- to debt repayment, it would barely make a dent in its debt levels.

The same sentiment may apply to revenues. In the first six months of 2023, operating revenues of $60 billion grew by just 1% compared with the same period in 2022. While expense cuts led to an 18% increase in operating income, lower income from non-core sources helped bring about a net income of $9.2 billion in the first half of the year. That's a decline of 5% versus year-ago levels.

Furthermore, the annual dividend of $1.11 per share costs AT&T about $8 billion annually. With rival T-Mobile achieving higher returns by not paying dividends, it should not surprise investors if management reduces or eliminates the payout.

Making a case for AT&T stock amid its challenges

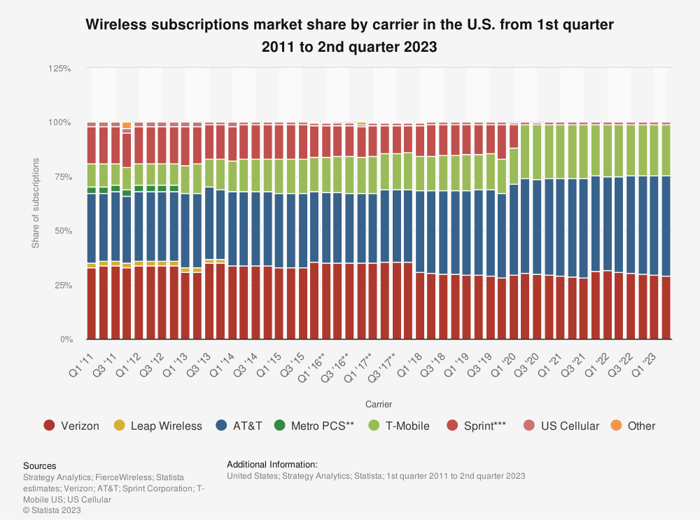

But despite the challenges, investors should start paying attention to significant improvements made in the business. The company claimed 6.2 million in total wireless net adds over the last year. This could bolster its wireless market share, which, at 46%, continues to bring steady gains compared to Verizon and T-Mobile.

Image sources: Strategy Analytics, FierceWireless, Statista estimates, Verizon, AT&T, T-Mobile US, Sprint, and US Cellular.

Also, the 7% increase in broadband revenues helps to negate declines in legacy voice and data services. Although shareholders should not expect double-digit revenue growth, that points to the potential for significant improvements.

Moreover, management forecasts at least $16 billion in free cash flow for 2023. That will mean a significant improvement over free-cash-flow levels in the first half of the year. The higher free cash flow may or may not protect the dividend. Still, it enables AT&T to make more significant debt reductions even if it does not reduce the payout.

Finally, its P/E ratio now stands at 7. One could argue that AT&T stock has become cheap for many valid reasons. However, valuation matters at some point. Low earnings multiples tend to limit the downside, and with customers taking to the company's updated wireless and broadband services, its financial and customer numbers point to ongoing improvement.

Despite challenges, AT&T's 6.2 million wireless net adds, and 7% increase in broadband revenues point to steady gains where it matters most. That's why I see opportunities for ongoing financial and market share improvement in AT&T's business.

Investing in AT&T

AT&T stock continues to suffer as its troubles weigh on investors' minds. Nonetheless, the company leads the wireless industry in market share, and its broadband offerings are growing in popularity as customers move away from legacy services.

Admittedly, investors should not expect rapid growth, and the company could reduce or eliminate its massive dividend in favor of faster debt reduction. Still, with a rock-bottom P/E ratio and more customers choosing AT&T over its main rivals, the telecom stock should eventually turn around.