Snowflake (SNOW 3.69%) is a cloud computing company poised to benefit from growing investments in artificial intelligence (AI). As CEO Frank Slootman said, "There's no AI strategy without a data strategy."

And while that could be the case, Snowflake's business isn't exactly taking off due to AI. In fact, its losses increased this past quarter, and its growth slowed. Despite the supposed catalyst for its business in AI, the company isn't an overwhelming buy. Here are two key reasons I would avoid the stock today.

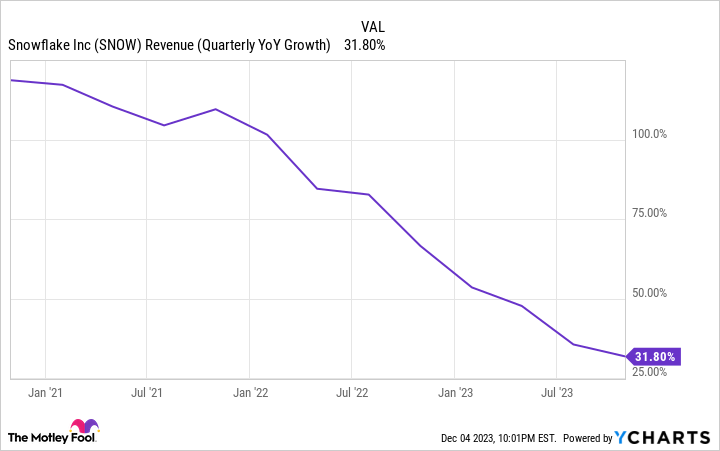

1. Its valuation is way too high

What's hard to get past is the fact the stock trades at an incredibly high valuation: 23 times sales or 12 times book value. While the business is growing, it's not at a fast enough rate, nor is it trending in the right direction, to justify this type of a price tag.

Data by YCharts. YoY = year over year.

In August, the company noted on its earnings call that its largest customers were also expected to be a "growth headwind."

Despite the excitement around AI, large businesses don't appear to be scaling up their operations significantly, which suggests that Snowflake might not get much of a boost from AI, at least not initially. Many companies are still trying to cut costs amid challenging macroeconomic conditions.

What exacerbates the problem for Snowflake is that while its revenue growth slows, costs are ramping up.

2. The company doesn't appear to be on a path to profitability

Two key metrics that growth investors should consider is the company's revenue growth versus its expense growth. If a company's expenses are rising faster than revenue, that suggests there might not be a path to profitability, at least not anytime soon.

In Snowflake's most recent quarter, which ended Oct. 31, revenue totaled $734.2 million, up 32% year over year. Operating expenses of $765.8 million were not only higher than revenue, but they grew at a faster rate: 34%.

The big cost driver was research and development (R&D) where expenses rose 57%. The company's headcount for R&D increased 53%, a key driver behind the increased spending.

The end result is that despite a solid growth rate, the company's net loss of $214.3 million was deeper than the $200.9 million loss it posted in the year-ago quarter. The loss as a percentage of revenue did improve from negative 36% to 29% in the same period, but Snowflake is still nowhere near hitting break even. The slow progress may not be enough for many investors.

Data by YCharts.

Investors shouldn't buy Snowflake stock until the financials improve

Revenue growth alone isn't a good enough reason to invest in Snowflake. Even on that front, the business is slowing down, and the rising popularity of AI has yet to prove itself as a significant growth catalyst for the company. Wall St. analysts have a cautious outlook on the tech stock as well with a consensus price target of less than $195, implying minimal upside from the stock trades as of this writing.

For investors looking to invest in a cloud business or stock that can benefit from AI, there are better companies to consider than Snowflake. Until there's a clear path to profitability and its financials look a whole lot better, investors should avoid the stock.