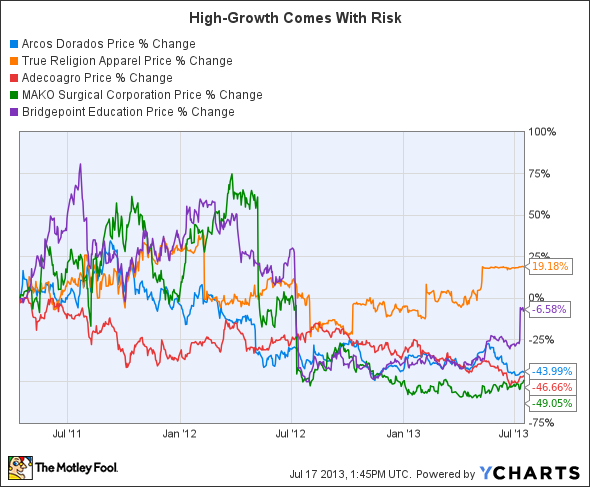

It goes without saying that no investment is completely free of risk. That is especially true of developmental stage companies, which can carry healthy doses of risk for years. Thinking that the growth potential outweighs any possible hiccups or obstacles can be a dangerous trap for investors. Just look at the tumultuous trip through the market taken by high-growth companies such as Arcos Dorados, True Religion, Adecoagro, MAKO, and Bridgepoint Education to see how these "slam-dunk" investments can turn out.

There are examples of companies that pummeled the market after successfully developing their products and brands, too. And of course, the companies presented above could still turn out to be great investments for long-term-minded investors -- although lower entry points may have awaited patient investors for each. With that in mind let's take a humble look at three potential headwinds facing renewable oils producer Solazyme (SZYM +0.00%).

1. Scaling is a two-headed monster

Unfairly or not, the market has decided to take a "show me" approach after initial setbacks in commercializing platforms throughout the industrial biotech industry. The risk here is twofold. First, Solazyme must commercialize each tailored oil independently of each other. Companies targeting one or more building block molecules such as Amyris (AMRS +0.00%) and Gevo (NASDAQ: GEVO) need only scale processes for the chemical precursors and can worry about refining them into value-added products independently of fermentation. For instance, Amryis' Biofene can be converted into thousands of other molecules, but the company can focus on optimizing just one fermentation process to get there.

In the end, even companies focusing on building-block molecules must successfully and efficiently synthesize useful products to penetrate commercial markets. However, failing to commercialize tailored oils (not all of Solazyme's oils are tailored) could take some steam out of production capacity additions and limit the company's product portfolio. Investors got a glimpse of this with the recently failed partnership with Roquette, although the commercialization failure did not stem from technical aspects.

The company isn't necessarily out of the woods yet, however. Solazyme needs to run its process at a consistent schedule in 625,000-liter bioreactors to reach its targeted manufacturing cost floor. The good news is that that volume is down markedly from the 750,000-liter figure quoted in the company's S1 filing. The bad news is that the company has only demonstrated its process with two partial runs at around 500,000-liter volumes and has yet to prove the commercial productivity of its microbes at that volume. It is important to remember that its first two facilities will not utilize the largest-sized bioreactors initially.

2. The World Cup and the Olympics

This may sound like a stretch at first, but it is a real threat. The rush to prepare Brazil's infrastructure for the FIFA World Cup in 2014 and the Summer Olympics in 2016 has exhausted the country's construction industry and overloaded regulatory offices with projects of varying priorities. Construction costs soared 8% from 2011 to 2012 and continued the torrid climb over the past 12 months. A report from the Brazilian Economy Institute found that engineer salaries increased by as much as 2% per month, with taxes and licensing fees rising as high as 5% each month. Total infrastructure investment for the World Cup is (currently) expected to reach $11 billion with new stadiums alone costing nearly $4 billion.

Brazil must really like soccer or something.

The construction of the Arena das Dunas includes an artificial lake, shopping malls, and hotels. Image courtesy of Wikimedia Commons.

Rising costs, equipment scheduling, and personnel shortages are all sizable threats to new construction projects in Brazil's fast-paced economy. Those factors could dampen the prospects of the industrial biotechnology industry's mad dash to the country's cheap sugarcane. Solazyme and Bunge (BG -2.54%) have already confronted the issue head-on with their jointly developed biorefinery in Moema, Brazil, that is expected to deliver product by the end of the year. The company's S1 filing estimated costs to be between $90 million and $110 million. The projected cost as of last May was $146 million -- an increase of 33% from the upper range -- and will likely have an even higher price tag once completed this year.

Unfortunately, that may not be the end of story. The joint venture is planning on adding 200,000 metric tons of renewable oil capacity at "select Bunge facilities worldwide" in the next several years. While the two may decide to look outside of Brazil for potential sites, they may swallow rising costs to get closer to the world's cheapest sugar source. Construction costs for future facilities will be much higher than they were for the one in Moema, even if the situation cools down, which could force the partners to write some pretty big checks.

3. Wall Street

Analysts on Wall Street played a large part in the collapse of the growth companies listed in the opening paragraph by failing to pay enough attention to risks. Unfortunately, I can see a few red flags arising with projections for 2014 revenue. The low estimate and the high estimate are separated by $340 million! The average revenue target calls for $271 million in sales next year, which would be difficult to achieve even in a best-case production scenario. Not all analysts have updated their targets after the failure of Solazyme Roquette Nutritionals, either, so expect that number to trek much lower in the coming weeks and months. Are analysts creating unrealistic expectations for the company?

Foolish bottom line

Out of the handful of the publicly traded industrial biotech companies, Solazyme is certainly on the best financial footing. That can go a long way in commercializing its platform and getting through ramp-up at its first two biorefineries through 2015. It's cash hoard won't last forever, but the company will not have to harm shareholders with dilutive offerings any time soon. Heck, if things go as intended, then shareholders will likely never get rocked with secondary offerings. Just don't forget to give some serious thought to the risk side of the equation.