How to Read Your Credit Card Statement

Updated

If you're on a Galaxy Fold, consider unfolding your phone or viewing it in full screen to best optimize your experience.

You probably get at least one credit card statement every month, but how well do you actually understand the information it contains? Yes, they tell you how much you owe and when you have to make a payment, but there's a lot more hidden in those pages than that. Here's a brief guide to how to read your credit card statement so you can get the most out of it.

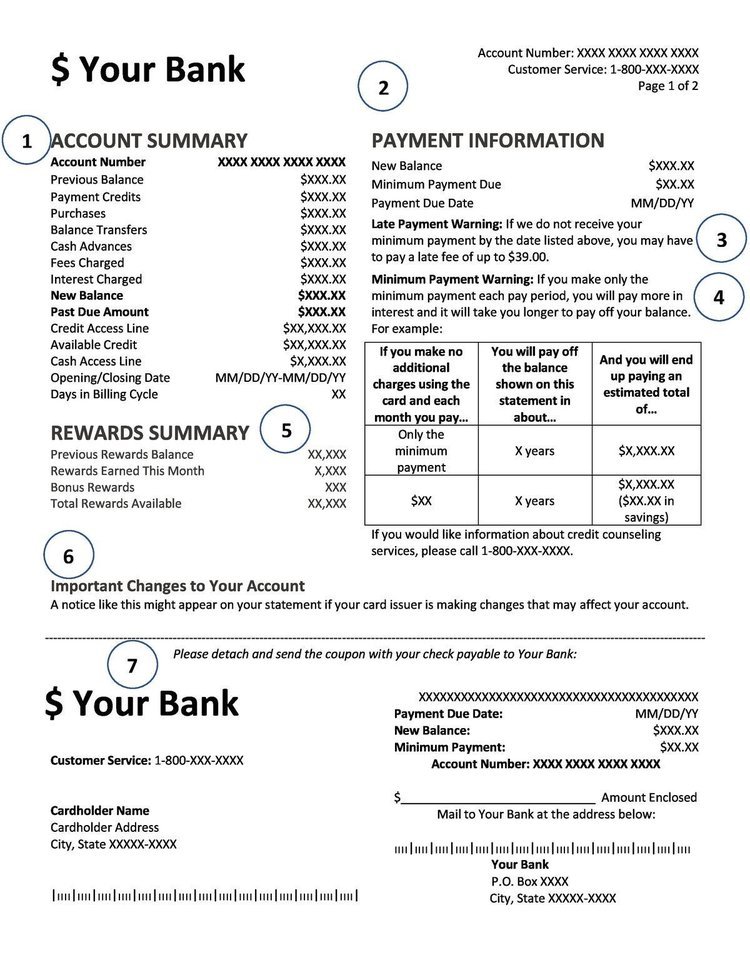

Every credit card statement is laid out a little differently, so yours may not look exactly like the one below. But you can expect to find more or less the same information in any statement, regardless of the card issuer.

Here's what each of the labeled sections in the image above means. For more information on the below items, see our guide on how credit cards work.

Your account summary is an overview of your credit card statement for the month. It tells you all about your monthly usage and how much you owe. Yours may not include all of these things or it may list them in a slightly different order, but usually, an account summary will include:

The payment information section provides you with important information about your new balance and your monthly bill, including:

The late payment warning tells you the maximum dollar amount you could be required to pay if you don't pay your credit card bill on time. Most card issuers won't charge you this much for a first-time offense. Check your cardholder agreement for more information on late payment penalties for your first, and any subsequent, late payments.

TIP

Credit card companies typically can't count your payment as late if they receive it by 5 p.m. on the due date in the time zone on the billing statement. If the due date falls on a Sunday or a holiday, the payment should be treated as on time if it's received by 5 p.m. the following business day.

The minimum payment warning usually includes a table to help you understand how long it will take to pay back your balance if you only make the minimum payment. Often, that period is several years -- and that's if you don't charge any more to your card in the meantime.

It may also include a comparison section showing how much more quickly you could pay off your balance if you paid more than the minimum. Some credit card statements also include a phone number you can call for credit counseling if you're struggling with your credit card debt.

Your credit card statement should have a rewards summary if you earn credit card rewards. This section contains the following information:

Visit your online credit card account or contact the card issuer by phone to see how much those rewards are worth and what you can spend them on.

This section highlights any significant changes your card issuer plans to make to your account in the near future. These might be changes that specifically apply to you, like triggering a penalty APR because you've made a number of late payments. Or it could be things that apply to all cardholders, like a change to the card's APR.

Your credit card statement should tell you which of your transactions these changes will affect and when they'll go into effect. If you have any questions, contact your card issuer for more information.

If you pay your credit card bill by mail, you must cut off this payment coupon (usually found on the bottom of the first page of your credit card statement) and send it in with your check. There should be a spot on the coupon for you to write the amount of the payment you're making. This helps speed up the payment process and ensures your card issuer applies your payment to the correct account.

If you pay your credit card bill online or have the money automatically debited from your bank account, you don't have to do anything with the payment coupon.

The account activity section of your credit card statement lists all the transactions you made during the current billing cycle, including the date of the transaction, the merchant's name, and the dollar amount. Some credit card issuers also attach a reference number to each purchase. That way, if you have a question about a transaction that's showing up on your statement or you suspect you may be a victim of identity theft, you can quickly tell the card issuer which purchase you're referring to.

If you carry a balance from one month to the next, you did a balance transfer, or you took a cash advance, you'll find a more detailed breakdown of the fees and interest you incurred in this section.

Your credit card statement may include a brief table summarizing how much you've paid in interest and credit card fees for the year to date. Let this serve as motivation for you if you're trying to pay off credit card debt.

The interest charges section gives you a more detailed explanation as to how your credit card issuer calculates the interest you owe. It may have separate sections for purchases, balance transfers, and cash advances if they all have different APRs. You'll also find information about a promotional APR here, if your account has one, including expiration dates.

You might see symbols like (v) or (d) after the interest charges section. These are a sort of mini glossary. Some of the most common terms and symbols you might see include:

If you find a charge you believe is inaccurate, try disputing it with the merchant first. Otherwise, you'll need to notify your credit card in writing within 60 days of the date the charge appeared on your billing statement. The credit card company will have 30 days to respond.

Your letter should include the following information:

While the charge is pending, you won't need to pay the disputed amount or any associated interest or fees. You will, however, be responsible for paying the undisputed balance as usual.

You can view your credit card statement online at any time by logging into your online credit card account and navigating to the statement information. If you've opted into electronic statements, your card issuer should send you an email every month when your new statement is available. It should contain all of the same information as the paper statement detailed above.

If you prefer to receive your credit card statements by mail, you can choose paper statements instead, though you may have to opt into this, as more and more companies are transitioning to online statements to save paper.

You can pay your credit card bill at any point during the billing cycle, even before you receive your monthly statement. On your statement closing date, which is usually at least 21 days before your payment due date, your card issuer will calculate your interest charges for the month and your minimum payment. It also reports your payment to the credit bureaus.

If you pay off your balance before this date, your payment will reduce or eliminate your balance and give you more credit to spend in the second half of the month. Making a payment will also lower your credit utilization ratio because credit bureaus only see what the credit card issuers report once per month. When your credit card bill arrives, it should show all of your purchases for the month, plus your first payment. Your new balance should list your remaining balance for the billing cycle.

If you pay after the statement closing date but before you actually receive your statement, you can calculate what you owe by subtracting what you've already paid from the new balance on your credit card statement when it arrives.

Your credit card statement balance tells you the amount you owe at the end of the billing cycle. However, your current balance tells you how much you owe overall. If you made additional purchases since the end of the billing cycle, your current balance will be higher than the statement balance. If you made payments since the billing cycle ended and didn't make additional purchases, the current balance will be lower.

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. Motley Fool Money does not cover all offers on the market. Motley Fool Money is 100% owned and operated by The Motley Fool. Our knowledgeable team of personal finance editors and analysts are employed by The Motley Fool and held to the same set of publishing standards and editorial integrity while maintaining professional separation from the analysts and editors on other Motley Fool brands. Terms may apply to offers listed on this page.