The Average Savings Account Balance In The U.S. – Here’s How Much Americans Have in the Bank

KEY POINTS

- The median transaction account balance is $8,000 -- that includes checking, savings, and other accounts.

- 55% of Americans can cover three months of expenses with savings.

- 45% of Americans can afford a $400 expense with funds from their checking or savings account.

The typical American household has $8,000 in their bank account, according to the latest data from the Federal Reserve’s Survey of Consumer Finances. That's the median transaction account balance as of 2022, which includes savings, checking, money market, call accounts, and prepaid debit cards. The average balance in those bank accounts among American households is $62,410.

Despite the median bank account balance being up nearly $2,000 from 2019, just 40% of Americans surveyed by Motley Fool Money feel financially secure. In line with that finding, the Federal Reserve found that only 57% of Americans have savings that could cover three months of expenses and just 44% could cover a $400 expense with money from their checking or savings account.

-

A note on averages, medians, and means

You'll note that we cite both the median and the mean for several statistics in this piece, though we rely more heavily on the median as a representation of what's average. Here's why.

Means are what most people think of as an average -- in this case, it would be the total amount of savings in the United States divided by the number of people who have savings accounts.

But there's a problem with that: very high values skew the mean quite a bit. For example, if we have five people who have $10, $100, $1,000, $10,000, and $100,000 in savings, the mean is over $22,000. Is that a good representation of the average person's savings? Not really.

The median, on the other hand, is the middlemost value. So, in the example above, the median would be $1,000. That's a better representation of what most people in the list have in savings. And the median becomes even more robust as you survey more people.

We do report both the median and the mean, though, so you can compare the two.

The median savings balance in the United States: $8,000

The median bank account balance for American households is $8,000, according to the Federal Reserve’s most recent data. That amount is what people hold in transaction accounts, which includes checking, savings, money market, call accounts, and prepaid debit cards.

That's up from 2019, when the median transaction account amount was $6,140 and much higher than the balance recorded in 2010, $4,780.

The average bank balance in 2022 was $62,410, up from $48,220 in 2019 and $44,050 in 2010.

When a median is much lower than a mean it suggests a larger number of people have less than the mean. To put it simply, the median is more representative than the mean.

Average savings balance by race

White American households have a median of $12,000 of cash on hand, roughly six times the amount that Black and Hispanic Americans hold, according to the Federal Reserve.

The gap in transaction account values between white and non-white is even larger when looking at averages. White Americans have an average transaction account balance of $80,000, while Black American households hold $13,370 and Hispanic American families have $15,710 in the bank.

Bank account balances have hardly changed for Black and Hispanic Americans over the past 30 years when looking at both the median and mean transaction account values for those groups. On the other hand, the median balance for white Americans has nearly doubled and the average balance has more than doubled.

Average savings balance by age

Older Americans tend to have more cash on hand, although the difference among age groups is smaller than expected.

The median balance in all transaction accounts, including savings, for those under 35 is $5,400. That rises to $7,500 for those between 35 and 44, $8,700 for those 45 to 54, $8,000 for those 55 to 64, and $13,400 for those 65 to 74. Median bank account balances drop off to $10,000 for those 75 and older.

The same pattern holds when looking at average transaction account balances by age, although at a wider scale. The average bank account balance for those 65 to 74 years old is $100 thousand. The average account balance drops to just over $70 thousand on average for those aged 45 to 64, and to $21 thousand for Americans 35 and younger.

Average savings balance by net worth

The richest American households -- those in the top 10th percentile of net worth -- have a median transaction account balance of $128,000. That's more than five times the median balance held by those in the 75th to 89th percentile of net worth and 128 times the median balance for those in the bottom 25% of net worth.

39% of Americans have a separate emergency savings account

Thirty-nine percent of Americans surveyed by Motley Fool Money have a separate emergency savings account.

Younger survey respondents were more likely to report having a separate savings account for emergencies. Forty percent of Gen Z and 47% of millennial respondents have a savings account just for emergencies compared to 32% of Gen X and 38% of baby boomers.

Having two savings accounts can seem like a hassle, but for some it is a useful way to manage finances. Separating savings into different accounts to cover expenses in the event of a job loss and savings for unexpected everyday expenses, like car maintenance or medical bills, can reduce anxiety and make it easier to track financial goals

An emergency fund calculator can help determine how much you might need to save.

63% of Americans can cover a $400 emergency expense with cash on hand

Sixty-three percent of Americans could cover a $400 emergency expense with cash or a credit card paid in full at the next statement, according to the Federal Reserve's 2026 Survey of Household Economics and Decisionmaking, which reflects 2025 data. Forty-three percent could cover that expense with cash alone.

Twelve percent said they could not afford a $400 emergency expense by any means.

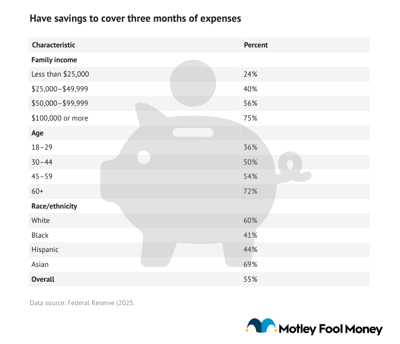

55% of Americans have three months of emergency savings

Fifty-five percent of Americans have three months of emergency savings, per data collected by the Federal Reserve.

That's level with 2024 and down from 59% in 2021.

Three months' worth of living expenses is the minimum our experts recommend to aim for with an emergency fund.

Many people need six or more months' worth of living costs in the bank to feel secure, so it's likely that some people pad their emergency savings for extra peace of mind.

34% have a savings account with an interest rate of at least 4%

Thirty-four percent of Americans surveyed by Motley Fool Money, have a savings account with an interest rate of at least 4%. That's up from 31% among those surveyed in 2023.

High-yield savings accounts -- which offer much higher annual percentage yields (APYs), or interest rates, than the national average -- have become more attractive and widespread as the Federal Reserve has hiked the federal funds rate.

It's important to note that savings account interest rates fluctuate, which is why our experts recommend comparing APYs before opening an account.

Older Americans surveyed by Motley Fool Money are less likely to have a savings account with an interest rate of 4% or more. Millennials are most likely to have a savings account with at least 4% APY.

| Generation | Savings account with interest rate over 4%? |

|---|---|

| Gen Z | 39% |

| Millennials | 43% |

| Gen X | 29% |

| Baby boomers | 28% |

| Total | 34% |

The top reasons people don't choose high yield savings accounts

The top reason more Americans don't have a savings account with an interest rate of 4% or more is that they don't think they have enough savings for a higher interest rate to make a meaningful difference.

The second most cited reason for not opening a savings account with an interest rate of 4% or more is not knowing accounts with those rates are available. Twenty-two percent of respondents said lack of knowledge was the main reason they didn't have that type of account, and baby boomers were least likely to know savings accounts with yields over 4% are offered.

Here are the other reasons Americans surveyed who don't have a savings account with an interest rate of 4% or more haven't opened one:

- Seven percent believe it would take too much effort to open an account with high interest rates and then transfer money to it. Younger generations were slightly more likely than older generations to cite this reason.

- Seven percent don't trust the banks offering savings accounts with high interest rates.

What is the primary obstacle to opening a savings account with an interest rate above 4%?

| Generation | It would take too much effort to open an account and transfer money | I don't have enough savings for a higher interest rate to matter to me | I don't trust the banks offering savings accounts with high interest rates | I didn't know savings accounts with interest rates above 4% are available |

|---|---|---|---|---|

| Gen Z | 13% | 45% | 11% | 31% |

| Millennials | 15% | 47% | 10% | 28% |

| Gen X | 9% | 47% | 13% | 31% |

| Baby boomers | 8% | 40% | 10% | 43% |

| Total | 7% | 29% | 7% | 22% |

Most Americans value a bank's reputation over high interest rates

Another reason Americans surveyed aren't likely to have a savings account with an interest rate of 4% or more is that most (59%) value a bank's reputation more than a high interest rate attached to their savings account.

Older respondents place more value on a bank's reputation than younger Americans.

Which do you value more: A savings account with a high interest rate or a savings account from a bank you consider reputable?

| Generation | A savings account with a high interest rate | A savings account from a bank you consider to be reputable |

|---|---|---|

| Gen Z | 48% | 52% |

| Millennials | 44% | 56% |

| Gen X | 40% | 60% |

| Baby boomers | 35% | 65% |

| Total | 41% | 59% |

Additional savings statistics

Our sample set offers a limited snapshot of how people are saving, so additional data is compiled here:

- American households held $14.5 trillion in checkable deposits, savings accounts, and time deposits, such as CDs, as of 2025, according to the Federal Reserve's Financial Accounts of the United States. That's a $715 billion increase from 2024. The growth was driven entirely by checkable deposits, which rose $1.3 trillion from 2024 to 2025, while savings accounts and CDs declined by $574 billion over the same period, suggesting households moved money into more liquid accounts.

- A Transamerica Center for Retirement Studies survey found that Americans have a median emergency savings balance of $5,000.

- The personal saving rate was 2.6% in April 2026, meaning Americans saved that share of their disposable income that month, according to the Bureau of Economic Analysis.

- Forty-two percent of Americans have no personal savings, according to Northwestern Mutual's Planning & Progress Study. The average balance among those who do have savings is $25,000.

- Thirty-three percent of Americans don't have a retirement account, according to the Federal Reserve.

- Thirty-five percent think their retirement savings are on track, level with 2024.

How to boost your savings

Most Americans don't have enough savings to cover three to six months of expenses, based on data from the Federal Reserve, given that the average household spends $6,081 but the median balance across transaction accounts is $8,000.

If you feel that your savings could use some work, Motley Fool Money personal finance expert Joel O’Leary recommends a few simple moves to help your bank account grow:

- Open a high-yield savings account: Not only do the high-yield savings accounts offer interest rates well above the national average, but keeping your savings out of your everyday checking account also makes you less likely to “dip into it” for non-emergencies. Opening a new, dedicated account really does help you save more.

- Automate the process: Arranging for an automatic savings transfer means you won't have to think about moving money yourself and you'll remove the temptation to spend. Your savings grow on auto-pilot.

- Take advantage of cash back: The best credit cards provide cash back and other rewards that can lower your bill, and leave you with more cash to save. Finding a card that fits your spending habits can net serious rewards. For example, some cards offer more competitive rewards for spending on everyday essentials, like gas and groceries, while others provide rewards for travel.

-

Sources

- Bureau of Economic Analysis (2026). "Personal Income."

- Federal Reserve (2026). "Economic Well-Being of U.S. Households in 2025."

- Federal Reserve (2026). "L.6 Assets and Liabilities of the Personal Sector (1)."

- Federal Reserve (2023). "Survey of Consumer Finances."

- Northwestern Mutual (2024). "2024 Planning & Progress Study."

- Transamerica Center for Retirement Studies (2022). "Emerging From the COVID-19 Pandemic: A Compendium About U.S. Workers' Retirement Outlook."

-

Methodology

The Motley Fool surveyed 2,000 American adults via Pollfish on July 8, 2024. Results were post-stratified to generate nationally representative data based on age and gender. Pollfish employs organic random device engagement sampling, a method that recruits respondents through a randomized invitation process across various digital platforms. This technique helps to minimize selection bias and ensure a diverse participant pool.

FAQs

-

How much does the average American have in savings?

The median bank account balance for American households is $8,000, according to the Federal Reserve’s most recent data. The average bank account balance is $62,410.

Our Research Expert

Jack Caporal is the Research Director for The Motley Fool and Motley Fool Money and has worked full-time for the company since 2021. Jack leads efforts to identify and analyze trends shaping investing and personal financial decisions across the United States. His research has appeared in thousands of media outlets including Harvard Business Review, The New York Times, Bloomberg, and CNBC, and has been cited in congressional testimony. He previously covered business and economic trends as a reporter and policy analyst in Washington, D.C. He serves as Chair of the Trade Policy Committee at the World Trade Center in Denver, Colorado. He holds a B.A. degree in International Relations with a concentration in International Economics from Michigan State University.

Motley Fool Stock Disclosures

Jack Caporal has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.