Oil prices have been on fire this year, surging by more than 25% and recently topping $60 a barrel. This year's surge has pushed crude oil pricing back above its pre-pandemic levels. Meanwhile, oil's run might not be done since OPEC and other producers are keeping a tight lid on supplies at a time when demand is starting to recover.

Given this backdrop, we asked some of our energy contributors which oil stocks they believe are best positioned to benefit if oil prices continue booming. They see some of the sector's best upside potential in contract driller Helmerich & Payne (HP -2.62%), oil and gas producer Devon Energy (DVN -3.01%), and equipment maker Caterpillar (CAT +1.98%). Here's why.

Image source: Getty Images.

The right tools

Reuben Gregg Brewer (Helmerich & Payne): Energy services get roughed up when oil falls because their customers pull back on spending. But when prices start heading higher the trend goes the other direction. Which is why Helmerich & Payne should benefit if oil prices take off (even more than they have already). The company has a couple of important things going for it.

First, it has a really strong balance sheet, with a debt-to-equity ratio of just 15%, and ample liquidity, roughly $1.3 billion. In other words, it has the financial strength to muddle through today's hard times and also the cash to take advantage of the next upturn. That means it can pivot back to growth as soon as demand picks up again.

HP Debt to Equity Ratio data by YCharts

Which brings up point No. 2: It has a large fleet of high-end drilling rigs. Simply put, the best rigs will get put back to work first. To put a number on that, only 80 of its 234 high-end rigs are currently contracted out, leaving a lot of upside potential. It is worth noting, too, that Helmerich & Payne's primary market is the U.S. fracking sector, which can ramp up production relatively quickly compared to other drilling methods.

So, Helmerich & Payne has the strength to survive until demand picks up, the rigs that will most likely get put back to work first, and operates in a market that should be able to ramp up quickly. That sounds like a winning combination.

A gusher of dividends at higher crude prices

Matt DiLallo (Devon Energy): Oil producers have a lousy track record of creating value for shareholders when oil prices are booming. They've usually wasted the cash flow generated at higher oil prices on drilling new wells or buying back their stock, only to have the next oil market bust incinerate that capital.

However, this year's oil market recovery might be different. U.S. producers have promised not to ramp up their drilling programs as oil prices rise. On top of that, oil companies are starting to get creative in how they return cash to their shareholders. Devon Energy is leading that charge by launching an industry-first variable dividend program. The oil producer aims to pay out up to 50% of its excess cash each quarter after funding its sustainable base dividend and maintenance capital program.

Devon's first variable dividend was a gusher at $0.19 per share ($128 million in total), more than double its base quarterly payout of $0.11 per share ($42 million). That payment is likely only a small taste of the variable dividend's potential since Devon's free cash flow rises with oil prices. For example, at $50 oil, Devon could produce more than $1 billion in free cash flow this year. Meanwhile, at the current oil price of more than $60 a barrel, Devon's free cash flow would approach $1.75 billion in 2021. With as much as half of those funds going back to shareholders via its variable dividend program, Devon could be a winning investment this year on booming oil prices.

Image source: Getty Images.

Neha Chamaria (Caterpillar): While my colleagues have prudently picked out oil and gas stocks that should be major beneficiaries from any rise in the price of oil, I'll deviate and recommend a company that doesn't quite belong to the sector but has significant stake in it nonetheless: Caterpillar.

Although Caterpillar is better known for its construction and mining equipment, oil price should matter to the company more than ever now given its increasing exposure to the sector. To put a number to that, consider that energy and transportation (E&T) toppled construction industries to emerge as Caterpillar's largest segment in 2020, accounting for nearly 42% of its total revenue. Sales from the segment, though, declined 21% in the year, dragged largely by a depressed oil and gas market. Oil and gas has been the largest end market for E&T in recent years.

That Caterpillar sees value in the energy markets is further evidenced by its latest acquisition -- that of the oil and gas division from The Weir Group for roughly $375 million. Oil's rebound should help Caterpillar unlock greater value from the acquisition even as higher prices encourage energy companies to revive their capital spending plans and spur demand for equipment like the reciprocating engines Caterpillar specializes in.

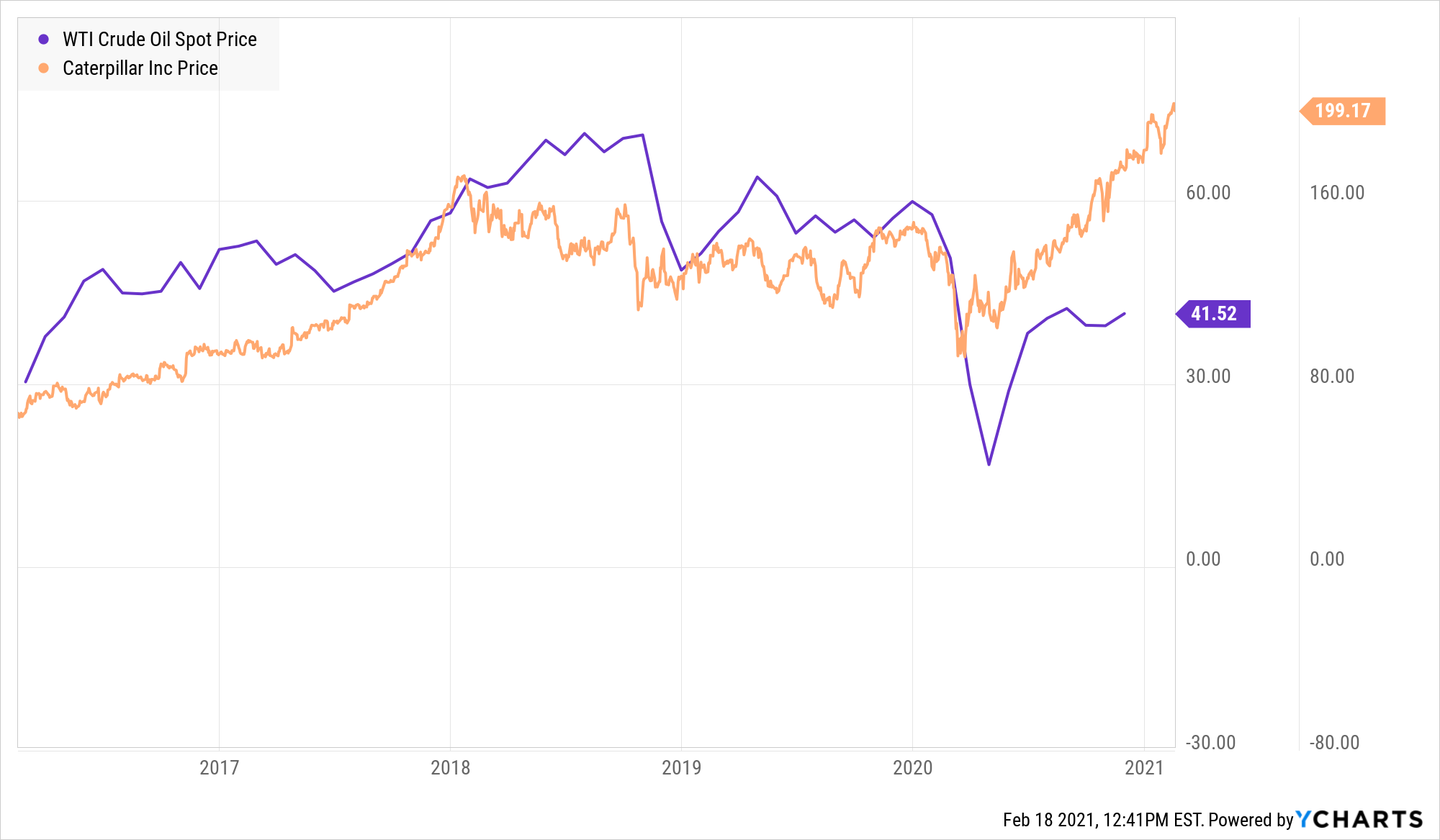

Surging oil, therefore, could be a shot in the arm for E&T and play an important role in the revival of Caterpillar's sales and profits going forward. To back up my argument, I'll leave you with a chart that shows how Caterpillar's stock price performance may not have mirrored but has moved pretty much in tandem with WTI crude oil price movement in recent years, reflecting the strong correlation between the two.

WTI Crude Oil Spot Price data by YCharts