Deciding where to put your money for the best return can be a daunting task. There are so many different factors to consider, and often various terms for various investments are hard to compare. Knowing how to use the annual percentage yield can help.

What is the annual percentage yield?

What is the annual percentage yield?

When you're looking at investments, there is a huge range of ways that your returns can be expressed. It helps to have a more standard language to use to line these investments up and compare them on more equal terms. That's where the annual percentage yield (APY) comes in.

With the APY, you can calculate the yearly return of an investment with compounding interest, regardless of how frequently that interest is compounded. Say you were considering an investment that compounded weekly and one that compounded monthly; using the APY, you could know beyond a doubt which would have the best return. Keep in mind that fees aren't included in this calculation, so you'll need to subtract those from your final results.

How do you calculate APY?

How do you calculate annual percentage yield?

Calculating the annual percentage yield is surprisingly simple. You just need the interest rate and the number of times your investment will compound in a year to figure out one year's APY.

The formula is:

APY = [(1 + (i / n))^n – 1] x 100

where i is the interest rate expressed as a decimal and n is the number of times it compounds in a year.

So, for example, if your investment was at 5%, compounding quarterly, i would equal 0.05, and n would equal 4, making the equation:

APY = [(1 + (0.05 / 4))^4 – 1] x 100, or APY = 5.09%

Maybe that doesn't seem like much, but let's look at it at different compounding intervals and how the APY compares to the straight interest offered.

| Interval | Interest | APY |

|---|---|---|

| Daily | 5.0% | 5.127% |

| Weekly | 5.0% | 5.125% |

| Monthly | 5.0% | 5.116% |

| Quarterly | 5.0% | 5.094% |

How to use the APY in investing

How to use the APY in investing

When you're looking at investments like zero-coupon bonds or money market accounts, you may find that the return rate is expressed with various compounding frequencies. Sometimes, it's glaringly obvious which one will have the better return, even without getting out the calculator, but it's often less obvious which will be the better place to put your money. That's when the APY formula comes in handy by letting you compare the outcomes on an annual basis, regardless of their actual compounding frequency.

In one year, there may not be a huge difference between an account that compounds 5% weekly vs. one that compounds 5% monthly, but that gap widens dramatically the longer you keep your money invested. And even if you weren't planning on keeping your money tied up for more than a year, wouldn't you rather have the extra few bucks for doing absolutely nothing?

Related investing topics

APY vs. annual percentage rate

Annual percentage yield vs. annual percentage rate

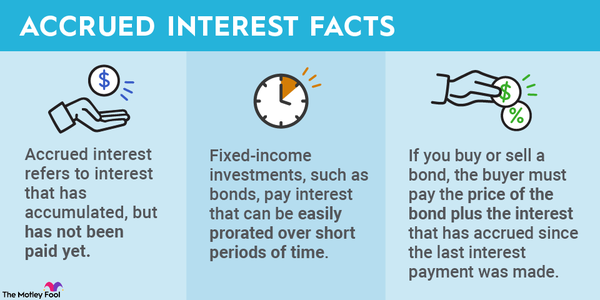

When it comes to investing, annual percentage yield (APY) is a very different concept than annual percentage rate (APR), even though they sound alike. The APY is the amount you stand to earn on an account with a compounding interest rate, although it doesn't include things like fees.

APR, on the other hand, is almost exclusively used to calculate interest on debt. So, if you're looking at the APR of a loan product, that's the cost of borrowing, including lender fees, closing costs, and insurance, divided by the number of years in the loan term.

If you do come across an investment with interest expressed as an APR, remember that it's not a compounding interest calculation; APR is only an expression of simple interest, along with the fees and additional costs associated.

It's unlikely you'll see this. But if you do, make sure to ask enough questions to figure out if the investment uses compounding or simple interest. The extra growth from compounding interest can make a huge difference over time.