Average American Household Debt in 2023: Facts and Figures

KEY POINTS

- RECORD-HIGH DEBT: American households carry $17.503 trillion in total debt as of late 2023.

- MORTGAGES DOMINATE: Mortgages constitute 70% of consumer debt, with the average mortgage debt at $244,498 in 2023.

- CREDIT CARD DEBT PEAKS: Total credit card debt reached a peak of $1.129 trillion in Q4 2023, with an average debt of $6,501 per holder.

As of late 2023, American households carried a total of $17.503 trillion of debt, averaging $104,215 per household.

This analysis from The Motley Fool Ascent cuts through the economic aftermath of inflation and supply chain issues to offer a comprehensive snapshot of where American households stand in terms of their financial obligations.

Drawing on data from Experian, the Federal Reserve, TransUnion, and the U.S. Census Bureau, we break down the most common types of debt including mortgages, auto loans, credit cards, and personal loans.

Key household debt figures

| FIGURE | AMOUNT |

|---|---|

| Total household debt, Q4 2023 | $17.503 trillion |

| Average household debt, 2023 | $104,215 |

| Total credit card debt, Q4 2023 | $1.129 trillion |

| Average credit card debt, Q3 2023 | $6,501 |

| Total mortgage debt, Q4 2023 | $12.252 trillion |

| Average mortgage debt, 2023 | $244,498 |

| Average mortgage payment, 2021 | $1,427 |

| Total home equity revolving debt, Q4 2023 | $360 billion |

| Average HELOC value, 2023 | $42,139 |

| Total auto loan debt, Q4 2023 | $1.607 trillion |

| Average auto loan debt, 2023 | $23,792 |

| Average monthly new car payment, Q3 2023 | $726 |

| Average monthly used car payment, Q3 2023 | $533 |

| Average personal loan debt, Q3 2023 | $11,692 |

Inflation, supply chain issues, and Americans' finances in 2023

The economy has roared back from the COVID-19 pandemic, bringing with it supply chain issues and inflation that have stressed Americans' wallets.

Throughout 2022, inflation reached levels not seen since the late 1970s, adding to the cost of goods already pushed higher by global supply chains snarled by shortages and the ongoing COVID-19 pandemic.

While inflation cooled in 2023, average debt is up in nearly every category compared to 2020. This includes total household debt, credit card debt, mortgage debt, and auto loan debt. Total debt is up by over $2.5 trillion since 2020.

The percentage of personal loans and auto loans in hardship are also above 2020 levels. Credit card and auto loan delinquency rates have been on the rise since the second half of 2022 and are now at levels not seen since the 2008 recession.

Average consumer household debt in 2023

| DEBT TYPE | Total, Q4 2023 unless otherwise specified |

|---|---|

| Total consumer debt (including types not listed below) | $17.503 trillion |

| Average household debt, 2023 | $104,215 |

| Total mortgage debt | $12.252 trillion |

| Total revolving home equity debt | $360 billion |

| Total auto loan debt | $1.607 trillion |

| Total credit card debt | $1.129 trillion |

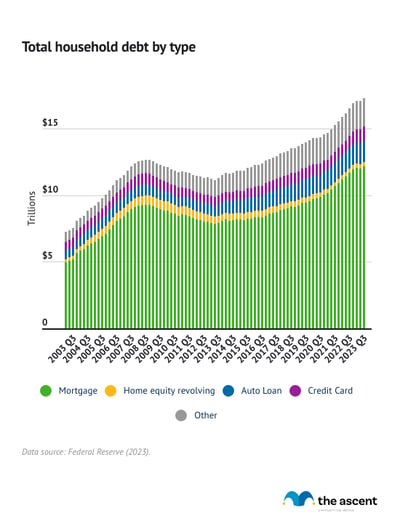

The New York Fed's quarterly Household Debt and Credit Survey (HHDC) shows that total consumer debt stands at $17.503 trillion as of the fourth quarter of 2023. That's a record high.

According to Experian, average total consumer household debt in 2023 is $104,215. That's up 11% from 2020, when average total consumer debt was $92,727.

Average American debt payments in 2023: 9.8% of income

The Federal Reserve tracks the nation's household debt payments as a percentage of disposable income. The most recent debt payment-to-income ratio, from the third quarter of 2023, is 9.8%.

That means the average American spends nearly 10% of their monthly income on debt payments. Despite debt increasing overall, Americans are still spending less of their income on debt than in most of the 2000s.

Average credit card debt in 2023

| FIGURE | AMOUNT |

|---|---|

| Total credit card debt, Q4 2023 | $1.129 trillion |

| Average credit card debt, Q3 2023 | $6,501 |

| Average store card balance, Q3 2022 | $1,110 |

| Average revolving credit card balance, 2022 | $5,910 |

| Delinquency rate of all credit card loans from commercial banks, Q3 2023 | 2.98% |

According to the latest Household Debt and Credit survey results from the Fed, Americans owe $1.129 trillion in credit card debt as of the fourth quarter of 2023. That's a record high, up from $1.079 trillion in the third quarter of 2023.

This could be because Americans are relying more on their credit cards due to inflation.

So what does that mean for individual credit card holders?

According to Experian, Americans had an average of $6,501 in credit card debt in the third quarter of 2023.

Average revolving credit card balance: $6,501

A revolving credit card balance is one that persists between payments -- in other words, it's what people pay interest on. It's one of the most important figures when looking at credit card debt.

The average credit card balance is $6,501 as of the third quarter of 2023, per Experian. That's up from $5,910 in 2022.

Based on data from the previous quarter, Gen X carries the highest average credit card balance, $8,870, while Gen Z carries the lowest average credit card balance, with $3,148.

Credit card balance by generation

| Generation | 2022 | 2023 |

|---|---|---|

| Generation Z (18-25) | $2,692 | $3,148 |

| Millennials (26-41) | $5,309 | $6,274 |

| Generation X (42-57) | $7,781 | $8,870 |

| Baby boomers (58-76) | $6,134 | $6,601 |

| Silent Generation (77+) | $3,305 | $3,434 |

Delinquent credit card payments: 2.98%

Americans remained surprisingly steady in paying their credit card bills on time. In the third quarter of 2023, the delinquency rate (at least 30 days past due) of credit card loans from commercial banks was 2.98%, according to the Federal Reserve. That's up from 2.77% in the previous quarter.

After hitting a record low in the third quarter of 2021, the delinquency rate of credit card loans from commercial banks has slowly increased, although it remains well below levels over the past 30 years.

In the third quarter of 2023, 6.36% of existing, non-seriously delinquent credit card debt became delinquent by 90 days or more, which is referred to as "serious" delinquency. That's a significant jump from 5.78% in the previous quarter and 4.01% in the fourth quarter of 2022.

Millennials, low-income borrowers, and to a lesser extent Gen Z, were most responsible for the spike in serious delinquencies due to expensive auto payments and other loans coming due.

Average mortgage and HELOC debt in 2023

| FIGURE | AMOUNT |

|---|---|

| Total mortgage debt, Q4 2023 | $12.252 trillion |

| Average mortgage debt, 2023 | $244,498 |

| Average (mean) mortgage payment, 2021 | $1,427 |

| Average (median) mortgage payment, 2021 | $1,001 |

| Average mortgage rate, Q4 2023 (30-year fixed) | 7.30% |

| Total home equity revolving debt, Q4 2023 | $360 billion |

| Average HELOC value, 2023 | $42,139 |

Mortgages make up 70% of American consumer debt. That number has risen consistently since mid-2013 and has recently accelerated as home prices hit record levels.

How much mortgage debt does the average American have? The average mortgage debt among Americans is $244,498, per Experian's 2023 State of Credit Report.

That's up from the average mortgage debt reported by Experian in 2022: $232,545.

Average mortgage rate in 2023: 7.30%

The average 30-year fixed mortgage rate for the fourth quarter of 2023 is 7.30%, up from 6.51% in the first quarter.

Mortgage rates have been rising since 2022 after hitting lows in 2020 and 2021.

Average mortgage payment: $1,427

According to the U.S. Census Bureau's American Housing Survey, the average (mean) mortgage payment in 2021 was $1,427, while the median was $1,001.

Average HELOC amount: $42,139

Based on data from Experian, the average value of a home equity line of credit in 2023 was $42,139.

Average auto loan debt in 2023

| FIGURE | AMOUNT |

|---|---|

| Total auto loan debt, Q4 2023 | $1.607 trillion |

| Average auto loan debt, 2023 | $23,792 |

| Average monthly new car payment, Q3 2023 | $726 |

| Average monthly used car payment, Q3 2023 | $533 |

Auto loan debt has been creeping up over the past several years and hit $1.607 trillion in the fourth quarter of 2023.

The average auto loan debt is $23,792 as of the third quarter of 2023.

The average car payment for both new and used vehicles has stabilized over the course of the year, with little change in the last three quarters of 2023, according to data from Experian.

Average new car payment: $726

The average monthly payment on a loan for a new car was $726 in the fourth quarter of 2023, according to Experian. Monthly payments on loans for new cars, by credit score, are as follows for the fourth quarter of 2023:

- Deep subprime (300-500): $737

- Subprime (501-600): $769

- Nonprime (601-660): $769

- Prime (661-780): $733

- Super prime (781-850): $693

- All: $726

Average used car payment: $533

The average monthly payment on a loan for a used car was $533 in the fourth quarter of 2023, according to Experian. Monthly payments on loans for used cars, by credit score, are as follows for the fourth quarter of 2023:

- Deep subprime (300-500): $535

- Subprime (501-600): $552

- Nonprime (601-660): $551

- Prime (661-780): $527

- Super prime (781-850): $544

- All: $533

Auto loans in hardship in 2023: 4.33%

According to TransUnion, 4.33% of auto loans were in hardship in December 2023, up from 3.83% the previous year.

TransUnion says that a loan is in hardship if the borrower has a deferred payment, forbearance program, frozen account, or frozen past-due payment.

Rising vehicle prices and overall inflation through 2022 and the start of 2023 may be responsible for a higher percentage of auto loans being in hardship compared to previous years.

Average personal loan debt in 2023: $11,925

| FIGURE | AMOUNT | Previous year |

|---|---|---|

| Average unsecured personal loan amount, October 2023 | $7,608 | $7,934 |

| Average unsecured personal loan balance per consumer, December 2023 | $11,925 | $11,241 |

| Average finance rate on 24-month personal loans from commercial banks, January 2024 | 12.35% | 11.48% |

| Personal loans in hardship, December 2023 | 3.40% | 3.70% |

Personal loans are versatile financial products. They can be used for a variety of financial needs, including weddings, renovations, vacations, or debt consolidation

According to TransUnion, the average unsecured personal loan amount in October 2023 was $7,608, down from $7,934 in October 2022.

The average balance per consumer as of December 2023, however, is $11,925, indicating that many people who have one unsecured personal loan have at least one more. That's higher than the level recorded per consumer in December 2022, which was $11,241.

Average personal loan interest rate in 2023: 12.35%

The St. Louis Federal Reserve tracks the average unsecured personal loan interest rate. In November 2023, the average interest rate for a 24-month personal loan was 12.357%, the highest since November 2007.

Personal loans in hardship in 2023: 3.4%

In December 2023, 3.4% of unsecured personal loans were in hardship. That's down from the same month in 2022, when 3.7% of unsecured personal loans were in hardship, according to TransUnion.

TransUnion says that a loan is in hardship if the borrower has a deferred payment, forbearance program, frozen account, or frozen past-due payment.

American medical debt

Medical debt can be difficult to track. However, it's clear that it's a growing problem.

According to The Urban Institute, 13% of Americans -- over 43 million people -- had medical debt in collections in 2022. That number is higher in communities of color, at 15%.

Some states have significantly higher numbers, too. For example, 24% of West Virginians have medical debt in collections.

The median debt also varies quite a bit. In the United States overall, the median medical debt in collections is $703. In Wyoming, Utah, Wisconsin, and Florida, that number is over $900.

While statistics are scarce, it seems likely that rising healthcare costs -- especially during a global pandemic -- have pushed these numbers higher in recent years.

Bankruptcy, delinquencies, charge-offs, and foreclosures

When Americans can't handle their debts, we see foreclosures, bankruptcies, delinquencies, and charge-offs. When those numbers go up, it's clear that Americans' personal finances are in trouble.

So what happened this year?

Personal bankruptcy statistics

According to the American Bankruptcy Institute's most recent release, there were 89,224 declarations of bankruptcy in the United States by the end of March 2022.

Interestingly, that's 17% less than the number we saw at the same point in 2021.

Personal bankruptcies by state

Here are the 2022 bankruptcy filings through March per capita of all 50 states and D.C. The total number of year-to-date (YTD) personal bankruptcy filings per capita in the country as a whole is 1.38.

Charge-off and delinquency rates on consumer loans in 2023: 2.36%

The Federal Reserve Board collects statistics on charge-offs and delinquencies by loan type. Here's how they've changed since 2010:

Charge-offs and delinquencies for consumer loans, credit cards, and real estate loans were up in the first quarter of 2023 compared to the previous quarter.

The delinquency and charge-off rate for consumer loans (which includes credit cards) was 2.36% in the second quarter of 2023, while the overall rate, which includes real estate and commercial loans, was 1.26%.

Foreclosures in 2023

There were 20,490 foreclosures in December 2023, according to ATTOM. That's down 3% from December 2022.

Average buy now, pay later monthly payment

The average monthly buy now, pay later (BNPL) payment made in 2023 is between $1 and $100, according to a survey from The Ascent, a Motley Fool service.

| Average total monthly BNPL payment | Percentage of respondents |

|---|---|

| $50 or less | 25% |

| $51 to $100 | 26% |

| $101 to $250 | 21% |

| $251 to $500 | 15% |

| $501 to $1,000 | 8% |

| Over $1,000 | 4% |

Using buy now, pay later financing is akin to taking out a loan. While most BNPL providers say they don't charge interest, some do, and late fees can be steep while negatively impacting your credit score. And unlike using a credit card, making BNPL payments on time doesn't boost your credit score.

Fifty percent of Americans surveyed have used BNPL and, worryingly, a third of those users have made a late payment or incurred a late fee.

The popularity of buy now, pay later took off between 2020 and 2021, but has since declined.

Americans are using buy now, pay later to finance a range of purchases. Forty-six percent of respondents surveyed say they've used BNPL to buy electronics and another 46% say they've financed clothing and fashion buys with BNPL. Nineteen percent used BNPL to pay for groceries.

Paying off debt

It may seem like Americans are swimming in too much debt to get out of, but there are ways to pay off debt.

The first step towards paying off debt is understanding the total amount of debt you have. From there you can determine what type of debt you hold, like credit card debt, a mortgage, or auto loan. Then it is important to note how much you owe, what the interest rate is, and what the minimum payment amount is for each type of debt you own.

With that information, you should be able to figure out how you can fit paying off debt into your personal budget. Our debt snowball calculator can help you organize your debts and explore repayment options.

Debt payoff apps can help you keep track of all those numbers, plus offer useful budgeting features like debt calculators and expense tracking.

Sources

- American Bankruptcy Institute (2022). "Bankruptcy Statistics."

- The Ascent (2023). "Study: Buy Now, Pay Later Use Declines for Third Straight Year."

- ATTOM (2024). "U.S. Foreclosure Activity Increases From 2022 But Still Below Pre-Pandemic Levels."

- Braga, Breno, Signe-Mary McKernan, and Caleb Quakenbush (2022). Urban Institute "Debt in America: An Interactive Map."

- Debt.org (n.d.). "Medical Debt Relief."

- Experian (2024). "Experian Study: Average U.S. Consumer Debt and Statistics."

- Experian (2024). "Experian 2023 Consumer Credit Review."

- Experian (2024). "Experian State of Automotive Finance Market Q4 2023."

- Experian (2023). "Average Credit Card Balances up 13.2% to $5,910 in 2022."

- Federal Reserve (2024). "Household Debt and Credit."

- Federal Reserve (2024). "30-Year Fixed Rate Mortgage Average in the United States."

- Federal Reserve (2024). "Delinquency Rate on Credit Card Loans, All Commercial Banks."

- Federal Reserve (2024). "Finance Rate on Personal Loans at Commercial Banks, 24 Month Loan."

- Federal Reserve (2024). "Household Debt Service Payments as a Percent of Disposable Personal Income."

- Federal Reserve (2024). "Charge-Off and Delinquency Rates on Loans and Leases at Commercial Banks."

- TransUnion (2024). "Credit Industry Snapshot.

Our Research Expert

Jack Caporal is the Research Director for The Motley Fool and The Motley Fool Ascent.

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.