Most of us are used to borrowing money in some capacity, whether it's mortgaging our homes or bumming a few bucks off a friend. Similarly, companies, municipalities, and the federal government borrow money, too. How? By issuing bonds.

How bonds work

How bonds work

Bonds are a way for an organization to raise money. Let's say your town asks you for a certain investment of money. In exchange, your town promises to pay you back that investment, plus interest, over a specified period of time.

For example, you might buy a 10-year, $10,000 bond paying 3% interest. In exchange, your town will promise to pay you interest on that $10,000 every six months and then return your $10,000 after 10 years.

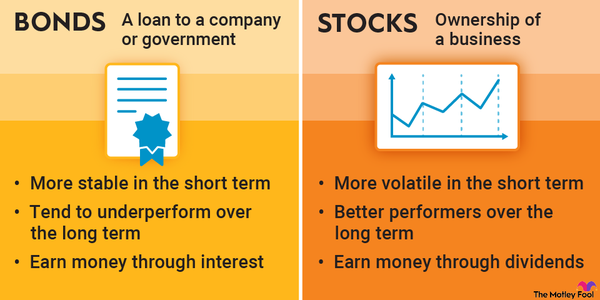

Bonds

How to make money from bonds

How to make money from bonds

There are two ways to make money by investing in bonds. The first is to hold those bonds until their maturity date and collect interest payments on them. Bond interest is usually paid twice a year.

The second way to profit from bonds is to sell them at a price that's higher than you initially paid.

For example, if you buy $10,000 worth of bonds at face value -- meaning you paid $10,000 -- and then sell them for $11,000 when their market value increases, you can pocket the $1,000 difference.

Bond prices can rise for two main reasons. If the borrower's credit risk profile improves so that they’re more likely to be able to repay the bond at maturity, then the price of the bond typically rises. Also, if prevailing interest rates on newly issued bonds go down, then the value of an existing bond at a higher rate goes up.

Yields, or the interest rate a bond pays, and bond prices tend to have an inverse relationship, meaning they move in opposite directions. If prevailing interest rates increase, prices for existing bonds are likely to fall because the coupon it offers is less valuable compared to new bonds.

With the Federal Reserve aggressively hiking interest rates in 2022, yields have gone up, which means that bond prices have generally gone down.

Not all bonds pay interest. Some bonds, known as zero-coupon bonds, offer a return once they’ve matured. Because these bonds don’t pay interest, they are usually sold for a deep discount to their face value.

Bond funds

Investing in bond funds

Bond funds take money from many different investors and pool it for a fund manager to handle. Usually, this means the fund manager uses the money to buy an assortment of individual bonds. Investing in bond funds is even safer than owning individual bonds.

Types of bonds

Types of bonds

Bonds come in a variety of forms, each with its own set of benefits and drawbacks:

- Corporate bonds: These tend to offer higher interest rates than other types of bonds, but the companies that issue them are more likely to default than government entities.

- Municipal bonds: Also called muni bonds, these are issued by states, cities, and other local government entities to finance public projects or offer public services. For example, a city might issue municipal bonds to build a new bridge or redo a neighborhood park.

- Treasury bonds: Nicknamed T-bonds, these are issued by the U.S. government. Because of the lack of default risk, they don't have to offer the same (higher) interest rates as corporate bonds.

How to buy bonds

How to buy bonds

Unlike stocks, most bonds aren't traded publicly but trade over the counter, which means you must use a broker. Treasury bonds, however, are an exception. You can buy those directly from the U.S. government without going through a middleman.

The problem with this system is that investors have a harder time knowing whether they're getting a fair price because bond transactions don't occur in a centralized location. A broker, for example, might sell a certain bond at a premium (meaning above its face value). Thankfully, the Financial Industry Regulatory Authority (FINRA) regulates the bond market to some extent by posting transaction prices as that data becomes available.

Pros and Cons of Investing in Bonds

Pros & Cons of Investing in Bonds

Pros of investing in bonds

- Safety: One advantage of buying bonds is that they're a relatively safe investment. Bond values don't fluctuate as much as stock prices.

- Income: Bonds offer a predictable income stream, paying you a fixed amount of interest twice a year.

- Community: When you invest in a municipal bond, you might help improve a local school system, build a hospital, or develop a public garden.

- Diversification: Perhaps the biggest benefit of investing in bonds is the diversification bonds bring to your portfolio. Over the long run, stocks have outperformed bonds, but having a mix of both reduces your financial risk. Investors tend to allocate a greater percentage of their funds to bonds as they get older and want to trade growth for safety.

Cons of investing in bonds

- Less cash: Bonds require you to lock your money away for extended periods of time.

- Interest rate risk: Because bonds are a relatively long-term investment, you'll face the risk of interest rate changes. For example, if you buy a 10-year bond paying 3% interest, and, a month later, that same issuer offers bonds at 4% interest, then your bond drops in value. If you hold it, you'll lose out on potential earnings by getting stuck with that lower rate.

- Issuer default: This is uncommon, but if an issuer defaults on its obligations, you risk losing out on interest payments, getting your principal repaid, or both.

- Transparency: There's less transparency in the bond market than in the stock market, so brokers can sometimes get away with charging higher prices. You might have a harder time determining whether the price you're quoted for a given bond is fair.

- Smaller returns: The return on investment you'll get from bonds is substantially lower than what you'll get with stocks.

Related investing topics

Should you invest in bonds?

Should you invest in bonds?

The only person who can answer that question is you. Here are some scenarios to consider as you decide:

If you're the risk-averse type who truly can't bear the thought of losing money, bonds might be a more suitable investment for you than stocks.

If you're heavily invested in stocks, bonds are a good way to diversify your portfolio and protect yourself from market volatility.

If you're near retirement or already retired, you may not have the time to ride out stock market downturns, in which case bonds are a safer place for your money. In fact, most people are advised to shift away from stocks and into bonds as they get older. It's not terrible advice provided you don't make the mistake of dumping your stocks completely in retirement.

FAQs

Bond FAQs

What are municipal bonds?

A municipal bond is a debt issued by a state or municipality to fund public works. Like other bonds, investors lend money to the issuer for a predetermined period of time. The issuer promises to pay the investor interest over the term of the bond (usually twice a year), and then return the principal back to the investor when the bond matures.

What are treasury bonds?

A Treasury bond is debt issued by the U.S. government to raise money. Technically speaking, every kind of debt issued by the federal government is a bond, but the U.S. Treasury defines the Treasury bond as the 30-year note. Generally considered the safest investment in the world, U.S. Treasury securities of all lengths provide a nearly guaranteed source of income and hold their value in just about every economic environment.

What are corporate bonds?

A corporate bond is a debt instrument issued by a business to raise money. Unlike a stock offering, with which investors buy a stake in the company itself, a bond is a loan with a fixed term and an interest yield that investors will earn. When it matures, or reaches the end of the term, the company repays the bond holder.