You need the money before the maturity date

Ideally, you should only buy bonds if you won't need the money until the maturity date. But in a worst-case scenario, you might need to sell a bond early.

Let's say you lose your job and run out of money in your emergency fund. Your only options are to sell your bonds or take on credit card debt at a 20% rate. Credit card interest will cost you much more than you'd earn from bonds, so selling would be the better choice.

The borrower is financially unstable

Bonds are generally considered low-risk investments, but this depends on the issuer. Treasury bonds issued by the U.S. government are as safe as it gets. Corporate bonds, on the other hand, come with more risk in exchange for higher interest payments.

If the borrower that issues a bond starts to experience financial problems, it can affect your bond's market value and risk level. For example, if you buy a corporate bond and the company goes bankrupt, you probably won't get the full value of your bond. Situations like this are rare, but they're still worth watching out for and a sign that selling bonds could be the best move.

You want to rebalance your portfolio

The right mix of investment assets depends on your risk tolerance, goals, and age. As these change, you'll need to rebalance your portfolio accordingly. In some cases, this could mean selling bonds.

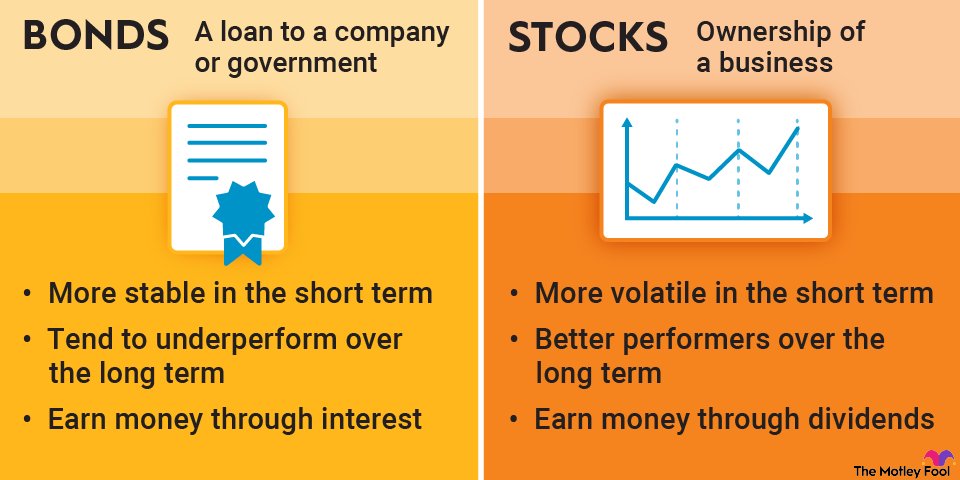

Generally, you'd sell bonds if you're willing to take on more risk and aim for higher returns from your portfolio. You could then use the proceeds to invest in stocks. The stock market is riskier and more volatile, but it has historically delivered average returns that are much higher than those of bonds.