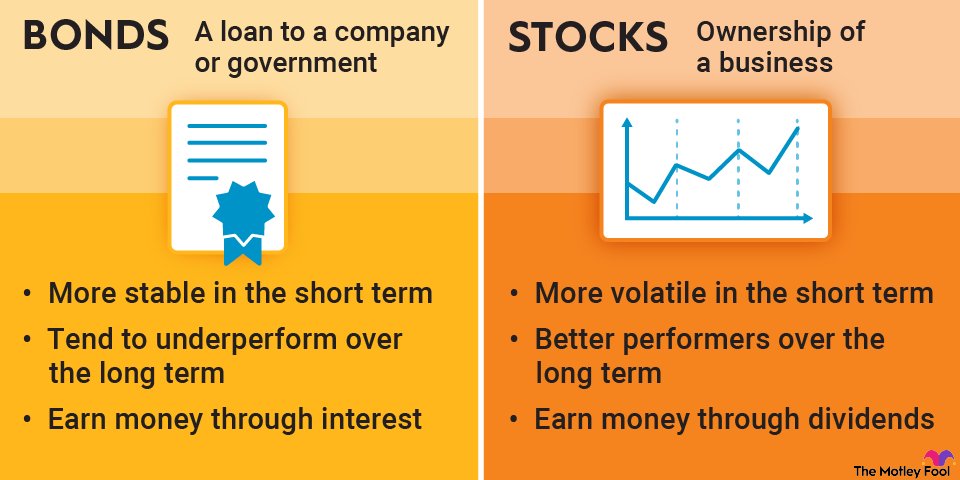

A bond is a debt instrument issued by a government or corporation to raise money. Investors who buy bonds receive a fixed return based on the bond's interest rate. Most of us are used to borrowing money in some capacity, whether it's mortgaging our homes or asking a friend for a few bucks. Similarly, companies, municipalities, and the federal government borrow money, and they use bonds to do it.

How bonds work

Bonds are a way for an organization to raise money. Let's say your town is seeking funding. In exchange, it promises to repay the investments with interest over a specified time period.

For example, you might buy a 10-year, $10,000 bond paying 3% interest. In exchange, your town pays you interest on that $10,000 every six months and returns your $10,000 after 10 years.

How to make money from bonds

There are a few ways to make money by investing in bonds:

- Hold bonds until their maturity dates and collect interest payments on them. Bond interest is usually paid twice a year.

- Buy zero-coupon bonds and hold them until the maturity dates. This type of bond is sold at a discount to its face value, so you receive more than what you paid when the bond matures.

- Sell bonds at a price higher than you initially paid.

Bond prices can fluctuate, enabling bond traders to profit. Prices normally rise if either the bond issuer's credit rating improves, indicating it's more likely to repay the bond, or interest rates on newly issued bonds decrease.

Interest rates and bond prices tend to move in opposite directions. If rates increase, prices for existing bonds are likely to fall because they offer lower rates than newly issued bonds.