How do tax-free municipal bonds work?

A bond is a debt instrument, and municipal bonds are issued by state, local, and other government entities to raise funds.

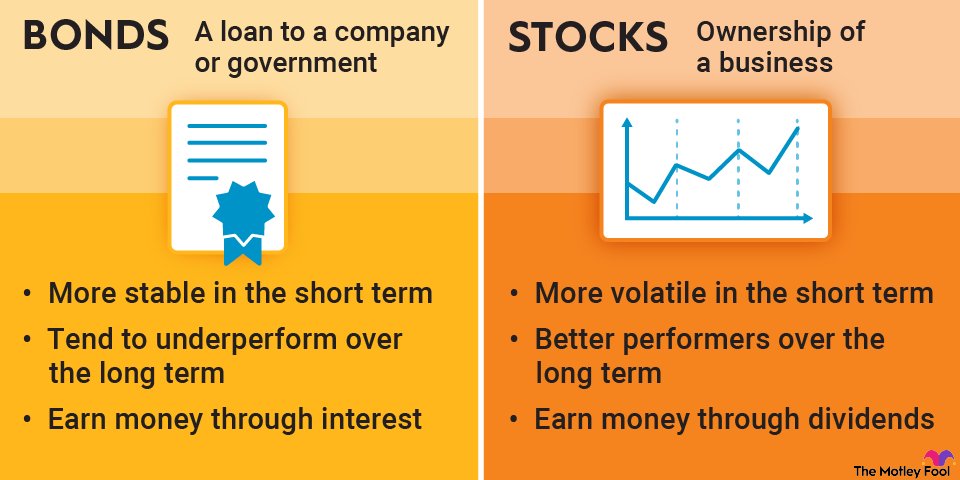

When you invest in bonds, the issuer pays you interest on a fixed schedule and returns the principal to you on the bond's maturity date. Tax-free municipal bonds are normally exempt from federal income taxes, and possibly state and local taxes, as well.

Why are municipal bonds tax-free?

In 1895, the Supreme Court ruled that the federal government had no power to tax interest on municipal bonds issued by state and local governments. The 16th Amendment to the U.S. Constitution, which authorized federal income taxes, included this exemption for municipal bonds.

One reason the exemption has persisted is that it enables states and governments to borrow at a lower cost, making it more economically viable for them to invest in public projects.

Benefits and risks of investing in tax-free municipal bonds

Here are the biggest benefits of investing in tax-free municipal bonds:

- You save on taxes: If you're in a high tax bracket, tax-free munis could reduce your tax burden.

- They're safe: Their default rate from 1970 to 2022 was less than 0.1%, according to Moody's Investor Service.

- They provide predictable income: Tax-free municipal bonds generally pay interest twice a year.

Like any investment, tax-free municipal bonds also have their downsides:

- They have low returns: Municipal bonds tend to pay less than other bonds and have much lower average long-term returns than stocks.

- They have interest rate risk: If interest rates rise, the value of older municipal bonds with lower rates will decline.

- They're not always easy to sell: This can be an issue with smaller municipal bonds, but it probably won't be a problem if you stick to tax-free municipal bond funds.

Criteria for choosing tax-free municipal bonds

If you're looking for tax-free municipal bonds or bond funds, there are a few factors that can help you choose:

- Location of the issuer: If you want to avoid state and local taxes, you typically need to invest in munis issued in your home state.

- Types of bonds: Bond market options include short-, intermediate-, and long-term bonds, as well as investment-grade and high-yield bonds.

- Yield: Bonds with higher yields make you more money but are also more volatile.

- Bond rating: A measure of the safety of the bond issuer. Municipal bonds rarely default, but it's still good to check bond ratings before you invest.