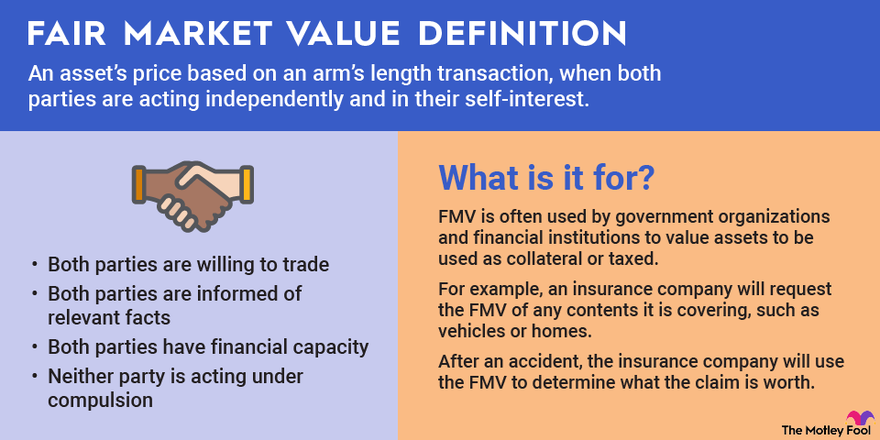

Fair market value (FMV) is the price that an arm's-length buyer would pay in the open market for an asset. FMV is often used by government organizations and financial institutions to value assets to be used as collateral or taxed.

We'll go over how FMV works, how it's calculated, and where you're likely to find it used.

Understanding fair market value (FMV)

You may be familiar with fair market value if you've purchased or sold a house and gotten an appraisal. Technically, appraised value and fair market value aren't the same thing, but they should be close to the same amount.

Appraised value is calculated by a licensed appraiser who uses an inspection, comparables, adjustments, and other market research to calculate an amount. FMV is often a rougher calculation of value done using comparables and a more basic understanding of the market.

Note that this direct difference between FMV and appraised value is the case for real estate sales. For some assets, such as equipment, fair market value will appear alongside orderly liquidation value in an appraisal as the appraised values.

FMV is also different from market value. Market value is the term for assets that trade in incredibly liquid markets. Assets such as stocks have publicly available values (prices) available on hundreds of websites. Likewise, commodities or commonly sold products will be listed for sale at the market value on an open market.

Fair market value is used in some instances by prospective buyers, but it is more common in financial industries, such as banking and insurance, to find the value of assets to be used as collateral or insurance.

It is also common in government-related activities, such as taxation and eminent domain, where the government needs a value for an asset. The IRS uses FMV for charitable donations and non-arm's-length transactions, meaning deals between related parties.

Examples of FMV

Let's go over a few instances where FMV might come into play.

Charity

It's easy to value a cash or stock donation to a charity, but rare art, jewelry, or even furniture can be a bigger challenge. If you donate such items, the IRS may require an appraisal to determine the fair market value of the donation.

Property taxes

The government calculates its own fair market value when it assesses and taxes the value of your property. Tax assessed value is almost always below the actual fair market value of the property, but you can protest the amount if it comes in higher than what you suspect the FMV is.

Insurance claims

Your insurance company will request the fair market value of any contents it is covering. If you make a claim, it may choose to obtain a new appraisal to update the FMV using tools such as the Kelley Blue Book value for a new or used vehicle.

Eminent domain

When the government decides it needs real estate for something like a road or government building, it sometimes has the authority to acquire that property using eminent domain. When this happens, it must pay the fair market value of the property.

Technically, this situation wouldn't meet the IRS definition of fair market value because the property owner may be an unwilling seller. However, the principles of FMV still apply. The government will hire its own experts to determine the FMV, and the owner of the property can hire experts to argue the case as well.

Gifts

The IRS requires any gifts valued at more than $15,000 to be subject to the gift tax. If the gift is valued at more than that amount, a gift tax return would need to be filed. The IRS uses FMV to calculate the value of gifts.

Stock ownership

Owners of private businesses may need to calculate the value of their business. This would be done by a business appraiser who uses techniques such as discounted cash flow to do the valuation.

If you need the FMV of stocks or bonds that you own, the current market value on the stock exchange would be used. You won't need to do any sort of advanced value investing techniques to find the FMV.

Related investing topics

How do you determine FMV?

Fair market value isn't like profit margin or return on equity where you throw in some inputs and come out with a number. It is more art than science. You or the appraiser will need to look at comparable sales, the liquidity of the market, the depreciation status of the asset, and the uniqueness of the asset to come up with a fair market value.

Users will take FMV with a grain of salt because it is not an objective number, meaning the number depends on subjective decisions of the appraiser. Banks apply a discount rate to the number, and businesses likely won't offer the full amount to buy an asset. You probably know this if you've ever tried to sell a car to a dealer for the Kelley Blue Book value.

Keep in mind these limitations, and use all the information that you have on hand. For example, equipment appraisers provide FMV and OLV (orderly liquidation value). The FMV is what the appraiser thinks the equipment is actually worth and should be considered the ceiling value of the equipment. The OLV is what the bank would get for the equipment if it repossessed it and sold it all in a fire sale.

Related: Learn about enterprise value of a company.