Ferrellgas Partners, L.P.'s (FGP +0.00%) primary business is delivering propane. WGL Holdings (WGL +0.00%) provides natural gas to the Washington D.C. area. Both are vital links for the their customers as they look to heat their homes and cook their food, among other things. Ferrellgas' 9.7% yield is far higher than WGL's 2.4% yield, which makes the propane distributor look pretty enticing -- but there's a whole lot more to understand here before you pull the trigger on either name.

The problem with Ferrellgas

In late 2016 Ferrellgas announced it would be cutting its distribution by a massive 80%. The cause of the distribution cut was a failed attempt by the propane partnership to diversify into the midstream oil and natural gas space. Diversification sounded good, but the realization didn't play out as expected after oil prices crumbled in 2014 and stayed low for years thereafter.

Image source: Getty Images

But that damage has been done and priced into the partnership's units, which are down roughly 85% since mid-2014. So there's notable recovery potential here for aggressive investors. And that high yield will reward the bold well, assuming Ferrellgas can turn things around.

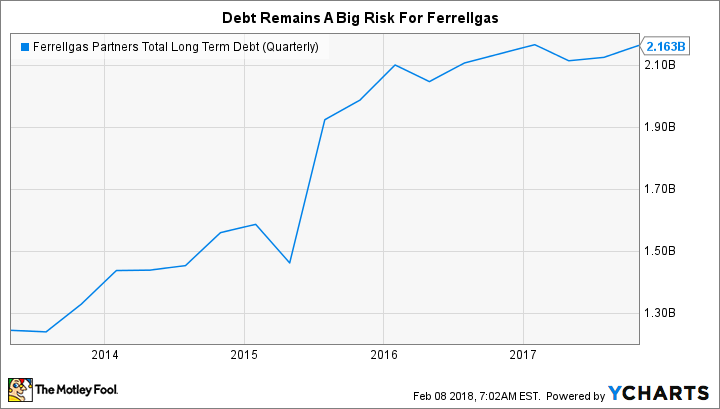

That, however, isn't a slam dunk. Part of the reason for the distribution cut was a massive increase in leverage that went along with the diversification effort. Long-term debt increased by around 80% over the last five fiscal years. When Ferrellgas lost a key customer on the midstream side of the operation it had no choice but to trim the dividend to help cover its interest expenses.

Although the partnership trimmed long-term debt by 10% in the first quarter of fiscal 2018, it still has a long way to go before its balance sheet is on solid financial ground. Note that unitholder equity is negative due to impairment charges related to the midstream investment, which leaves debt at more than 100% of the capital structure.

FGP Total Long Term Debt (Quarterly) data by YCharts

And then there's the issue of the midstream business. Ferrellgas still has to do something with this division. It's begun to take steps to deal with the overhang by selling one of its midstream businesses, but there remains a lot of work to do before it crawls out from under this, in hindsight, ill-advised diversification effort. That could include selling more assets or trying to turn the midstream business around, neither of which will be easily achieved. There's material turnaround potential and a high yield here, but still a great deal of risk and uncertainty.

The problem with WGL

Which is where WGL comes in. This natural gas-focused utility has increased its dividend for an incredible 41 years. Although the utility's 2.4% yield is paltry compared to Ferrellgas' nearly 10% yield, it has proven itself a far more stable business over time. Only there's a caveat here, too: WGL has agreed to be acquired by Canada's AltaGas Ltd.

It's an all-cash deal worth $88.25 per share. The companies agreed to the deal in early 2017, and it's already received shareholder approval. The two companies are now working to clear all of the regulatory hurdles. Utility mergers tend to be slow moving because of the government involvement in setting customer prices for these largely monopolistic businesses; however, it appears to be inching closer to closing.

WGL's shares are currently trading at around $85.41 a share. That means that investors can expect a capital gain of roughly 3%, plus any dividends along the way, when the deal is finally consummated. That, of course, assumes the deal is completed as planned, which sometimes doesn't happen and can lead to share price declines at the company expecting to be acquired. Still, investors are effectively buying a utility that doesn't expect to exist in a relatively short period of time if they step in here. And the upside is 3%, plus dividends -- not an impressive figure.

The takeaway

Ferrellgas has a lot of recovery potential and offers a high yield. Most investors, however, should stay on the sidelines until it has gotten further along in the process of reducing debt and dealing with its midstream assets. Only aggressive investors should be looking at the name.

WGL, meanwhile, isn't a great option either. It's about to be bought out in an all cash deal that will leave investors who buy today with a meager return. That isn't worth the effort unless you are a big fan of merger arbitrage, an investment tactic that requires a great deal of experience to do well.