Amgen Inc. (AMGN 0.19%) and Gilead Sciences Inc. (GILD 0.57%) have both delivered monstrous gains in past years, but investors buying stocks today need to focus on tomorrow's opportunities and threats. Both of these biotechs are in the middle of some major changes, which makes it a perfect time to stack the two side by side to see which comes out on top.

These drugmakers generate huge profits that they distribute generously, so let's begin this comparison from an income investor's perspective.

Image source: Getty Images.

Dividends in focus

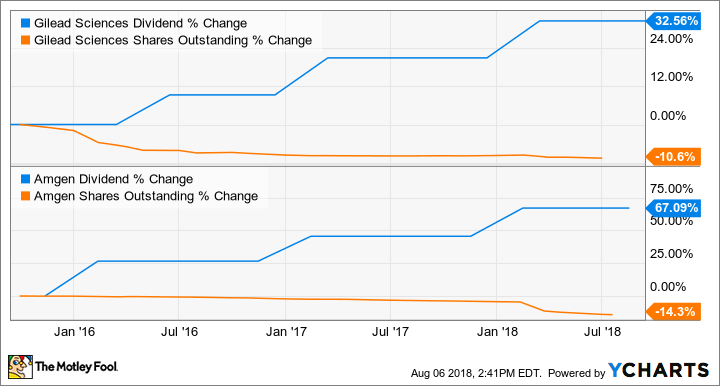

At the moment, shares of Gilead Sciences offer a better-than-average 2.9% yield that also tops the 2.6% yield that you'd receive from Amgen. Both of these companies generated an impressive $10.6 billion in free cash flow over the past year. Amgen used only 33% of FCF to make dividend payments over the period, and at around 26%, Gilead appears to have even more room to run.

Although Gilead's dividend looks superior on the surface, income investors should know that Amgen completed a massive $10 billion share repurchase earlier this year, which lowered its outstanding share count by 7.2% practically overnight. That means the profits this company generates from now on will spread even further.

GILD Dividend data by YCharts.

A few years ago, when Gilead's hepatitis C virus (HCV) treatments were bringing down 10 figures annually, the company made some dramatic share repurchases as well. Unfortunately, fierce competition in the HCV space has also limited the company's ability to reward shareholders in recent years.

Some of Amgen's top-selling products are also losing ground in their old age, but the company's managed to keep the entire needle-moving forward fast enough to outpace Gilead in terms of share repurchases and dividend growth over the past few years.

On the way down

Gilead's hepatitis C franchise can continue swirling toward oblivion without putting too much pressure on overall sales because those drugs now make up just 18% of the company's total haul. Amgen's former lead drugs aren't fading as fast as Gilead's have, but Enbrel, an anti-inflammation injection that's been around since 1998, and Neulasta, a white blood cell booster the Food and Drug Administration first approved in 2002, could lead to some sleepless nights in the quarters ahead. Amgen still leans on its former top products for 44% of total revenue.

During the second quarter, Enbrel sales fell by 11% and Neulasta sales rose by just 1 percentage point. As long as they both don't come crashing down at the same time, Amgen can probably keep the entire needle moving in the right direction, but investors could face losses if these key products slide quickly in the quarters ahead.

On the way up

Amgen's old cash cows may be on the way down, but the biotech has a line of younger products that are offsetting the losses. A cholesterol-reducing injection called Repatha got off to a slow start when it launched in 2015, mainly because it was really expensive. An aggressive lower-price-higher-volume approach pushed second-quarter sales 78% higher to $148 million, which could be the beginning of a long climb to several billion annually at its peak.

Amgen could have a first-in-class blood cancer blockbuster on its hands called Blincyto. This unique bispecific antibody hits two cancer targets at the same time with impressive results. If the recently launched blood cancer drug takes flight, it bodes well for a few related candidates Amgen has in late-stage development at the moment.

Earlier this year Gilead launched Biktarvy, a tiny HIV pill with some big advantages that convinced market research firm EvaluatePharma it can rack up at $5 billion in annual sales by 2022, and it's not the only iron Gilead has in the fire. The biotech's recently acquired cell-based cancer therapy division could give investors plenty to look forward to in the years ahead.

In the second quarter, Gilead's Yescarta racked up $68 million in sales. That's not necessarily impressive for a cancer drug, but significant sales for this unusual class of therapy were far from guaranteed. Selling Yescarta is a lot more involved than filling a bottle with pills as the therapy requires the removal of a patient's immune cells, which are trained offsite to recognize and attack cancer before they're shipped back to the patient's healthcare provider to be reinfused. Yescarta's relative success suggests lucrative launches are also possible for several candidates advancing through Gilead's pipeline at the moment.

The better buy?

Income-minded investors can find a lot to like about both of these stocks but Gilead Sciences squeaks ahead for a key reason: The headwinds it faces aren't as severe as Amgen's. As Enbrel and Neulasta fade, pushing the needle forward at a satisfying pace is going to be an uphill battle for Amgen. Gilead's hepatitis sales just don't have much further to fall anymore.

With fewer losses to offset in the years ahead, Gilead's shares could climb by double digits again if just one of its new cancer therapies becomes a top seller. That's more than you can say for Amgen -- and enough to make Gilead the better buy right now.