Oil prices plunged in the last few months of 2018, putting stress on many oil producers' budgets. This led to widespread predictions of reduced capex, idled oil rigs, and a downturn in U.S. oil production in 2019.

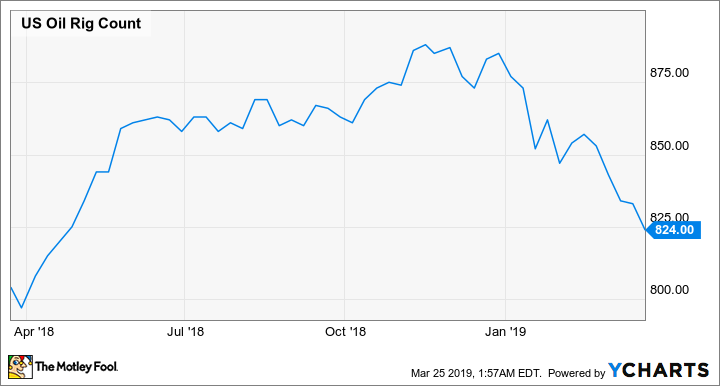

Sure enough, the number of rigs drilling for oil in the U.S. has been falling for most of this year, including declines in each of the past five weeks. The oil rig count is still higher than it was a year ago, but it has fallen by about 60 since late 2018.

U.S. oil rig count, data by YCharts.

However, the widely followed oil rig count statistic doesn't really mean much anymore. Even with fewer rigs at work -- at least for now -- U.S. oil production is likely to continue rising at a rapid clip in 2019 and beyond as oil giants like Chevron (CVX 0.65%) and ExxonMobil (XOM 0.52%) ramp up their shale drilling activities.

There's a huge backlog of uncompleted wells

The most fundamental reason why the rig count has become misleading is that in shale oil plays, drilling an oil well doesn't always lead immediately to starting production. At some point after the well is drilled, hydraulic fracturing (also known as fracking) -- the injection of highly pressurized water and sand -- starts the flow of oil. Fracking sometimes takes place right after the rig is removed, but not always.

There are various reasons for drilling but not immediately completing a well. For example, fracking crews or materials may be in short supply. Some oil leases require drilling within a certain time period, but don't require production to begin -- or require only a token amount of production. That means it might make sense to keep drilling but slow well completion activity when oil prices fall. Shortages of pipeline capacity could also affect well completion activity.

Over the past five years or so, the number of drilled but uncompleted (DUC) wells in the U.S. has soared. At the end of 2013, the DUC well count was 4,199 in the seven major regions tracked by the Energy Information Administration (EIA). That figure reached 8,576 by the end of February 2019.

The Permian Basin (centered in western Texas) accounts for the vast majority of this increase. The Permian DUC well count has surged more than sixfold (from 636 to 4,004) since the end of 2013, whereas the number of DUC wells has risen 28% across the other six regions combined.

The number of wells drilled in the Permian Basin peaked at 622 last October and fell to 574 as of February. However, the number of Permian well completions rose from 444 in October to 486 last month. Not only did the two figures move in opposite directions, but even with the recent reduction in drilling activity, well completion crews still aren't keeping pace with the number of wells being drilled. Factoring in the huge backlog of DUC wells, producers could ramp up well completions by 50% or more without needing to increase drilling activity for at least a year.

Production changes don't necessarily track changes in the rig count anymore. Image source: Getty Images.

The arrival of the oil majors is a game changer

The growing involvement of the oil majors in shale oil production -- particularly in the Permian Basin -- is another reason not to read too much into the recent rig count declines.

Traditionally, the biggest players in shale oil have been smaller independent energy companies. In recent years, those companies have been forced to cut back on drilling activity whenever oil prices fall in order to avoid burning too much cash. (However, they can complete already-drilled wells to keep production steady or growing and to shore up their cash flow.)

By contrast, massive oil giants like Chevron and ExxonMobil have more ability to invest for the long term. Also, both companies have taken a deliberate approach in the Permian Basin, with lots of testing and learning, which should pay off in the form of higher rig productivity in the future. (Productivity improvements are another reason why the rig count can be misleading.)

Chevron and ExxonMobil are now ready to ramp up their activity in the Permian Basin. Chevron plans to more than double its Permian production to 900,000 barrels of oil-equivalent per day (boepd) by the end of 2023, with steady growth over that period. Meanwhile, ExxonMobil is in the midst of dramatically increasing its drilling and fracking activity. It expects to produce more than 1 million BOE/D in the Permian region by 2024, up from just 200,000 BOE/D recently.

Check out the latest earnings call transcripts for Chevron and ExxonMobil.

More pipeline capacity points to higher production

Between the huge number of DUC wells in the Permian Basin and Chevron and ExxonMobil's plans to increase drilling activity dramatically, the recent rig count declines aren't likely to lead to falling production. In fact, growing pipeline capacity in the Permian region is likely to encourage accelerated production growth over the next couple of years.

For most of 2018, the price of crude oil in Midland, Texas -- the heart of the Permian Basin -- traded at a discount to the U.S. benchmark (WTI). In August and September, that discount reached a high of around $18 per barrel, as a shortage of pipeline capacity led to a glut of oil in the Permian region. Extra pipeline capacity has come on line since then, causing Midland crude to trade at a slight premium to WTI recently.

As a result, even though WTI prices are still down by about $10 per barrel relative to last August and September, Permian producers are making more money today. Nevertheless, producers may still be skittish about dramatically increasing well completions in the region, as there is still a delicate balance between oil production and pipeline capacity.

That will change soon, with numerous pipelines under construction that could increase takeaway capacity by 4 million barrels per day or more over the next two years. A big chunk of that capacity will come on line in the second half of 2019.

With pipeline constraints set to ease later this year, oil producers are likely to ramp up output in the most prolific shale region during 2019 and 2020 -- regardless of short-term changes in the rig count. That will likely keep a lid on oil prices for the foreseeable future.