The last couple of years have been rough on the cloud software sector. A combination of sky-high valuations coming out of the pandemic and a slowdown in demand resulting from a broader tech recession caused much of the sector to crash.

Among the victims has been Amplitude (AMPL +0.62%), a cloud software company focused on digital analytics. Amplitude went public in September 2021, shortly before the Nasdaq peaked, and then crashed in 2022. The company's software gives businesses the ability to better understand their customers and improve their digital products.

For example, Amplitude helped Peloton Interactive recognize the value of social interactions in its workouts and guided Burger King's "Whopper Detour" campaign where the fast food chain offered a deal to customers who downloaded the app near a McDonald's location.

Amplitude stock soared out of the gate in 2021 as the company delivered blowout growth, but its growth rate has slowed dramatically like many of its software peers and the stock has gradually lost most of its value along the way. Following its first-quarter earnings report last Thursday, the stock edged down 1.5%, meaning it's now down 89% below its peak in 2021.

However, there are signs that Amplitude stock could finally be ready to return to growth after a long wait for investors.

Image source: Getty Images.

The pandemic hangover is fading

There's a straightforward reason for the company's sluggish growth over the last several quarters. As CEO Spenser Skates said in an interview with the Motley Fool, a number of Amplitude's customers overbought its products in 2021 and 2022, estimating that the strong growth in the tech sector during the pandemic would continue. With its customers on annual contracts, it's also taken a while for that correction to play out.

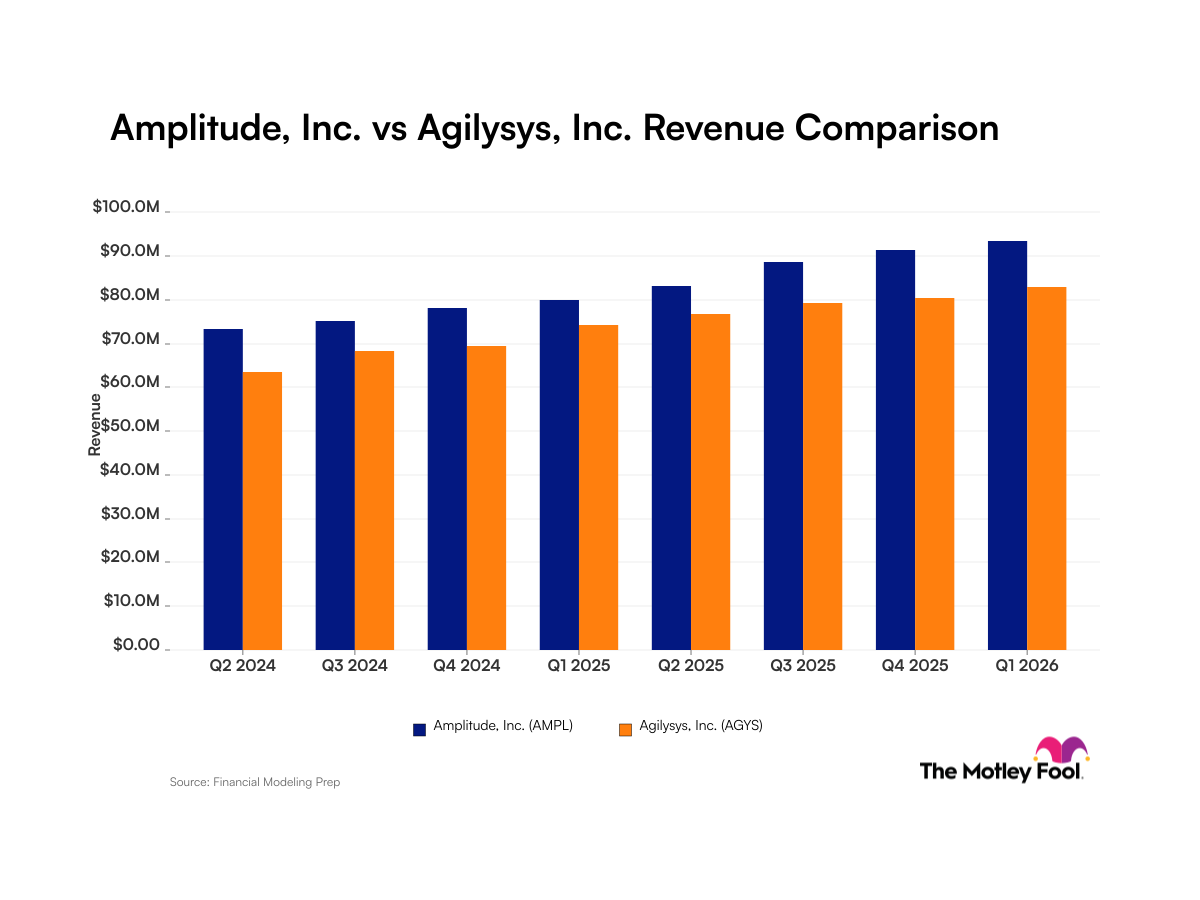

While the company has continued to bring on new customers since then, the corrections from existing customers who have been rightsizing their needs and workforces have affected results. Amplitude's revenue in the first quarter increased 9% to $72.6 million, and annual recurring revenue also rose 9% to $285 million. As the chart below shows, revenue growth has steadily trended downward since it went public.

That chart certainly looks scary, but those headwinds are expected to be mostly done with by the second half of the year. Amplitude's full-year revenue guidance of $292.5-$295.5 million implies growth of 6.4% at the midpoint, indicating that a recovery may have to wait until 2025. Skates said that he expects revenue growth to accelerate in the future as those headwinds fade.

Amplitude continues to innovate

Even while it faces those headwinds, the company isn't sitting still. Amplitude continues to innovate, rolling out its self-serve Plus tier for $49/month that has attracted thousands of new customers, some of whom have already moved up to higher-value tiers.

The company also just launched session replay, a new tool that allows users to see every step of the customer's digital interaction, where and when customers clicked to get a better idea of how the buying process works for the customer and how it can be improved. Skates noted that session replay had helped Amplitude attract customers away from point solutions as it now offers a more complete product, serving more of its customers' digital analytics needs.

NASDAQ: AMPL

Key Data Points

Is Amplitude stock a buy?

Based on the first-quarter numbers alone and the guidance, it seems like investors will need more patience with the software stock. However, the company continues to roll out new products and its bottom line has stabilized. It's targeting an adjusted per-share profit of $0.07-$0.09 this year, and it generated a free cash flow of $22.4 million last year.

It's hard to call Amplitude stock a buy until it starts showing momentum in revenue acceleration, but it also seems like a mistake to give up on the stock at this point. The business is stable, and Amplitude remains the leader in an emerging industry. If it can bounce back from the recent headwinds, the stock should have substantial upside ahead of it.