Shares of Taiwan Semiconductor Manufacturing (TSM 1.65%), or TSMC for short, climbed higher after the semiconductor contract manufacturer reported strong third-quarter results and offered an upbeat outlook. The stock has now about doubled year to date.

With its strong performance this year and recent jump in share price, investors may be wondering if it is too late to buy the stock.

Let's take a closer look at TSMC's most recent quarter and determine what kind of opportunity there is in the stock.

NYSE: TSM

Key Data Points

Strong growth and improved outlook

For its third quarter, TSMC's revenue jumped 36% year over year to $23.5 billion, while its earnings per American depositary receipt (ADR) came in at $1.94, up from $1.29 a year ago.

The company credited its results to strong growth for chips related to artificial intelligence (AI) and smartphones, while noting high demand for its 3-nanometer and 5-nanometer technologies. CEO C. C. Wei said AI demand is "real", and most AI innovators are working with the company, including those developing their own custom chips.

High-performance computing, which includes AI chips, represented 51% of TSMC's revenue in the quarter and was up 11% quarter over quarter. Smartphone revenue accounted for 33% of its sales and was up 16% sequentially.

Advanced technologies, which include nodes 7nm and under, represented 69% of its revenue. Within that category, 3nm technology accounted for 20% of total wafer revenue, while 5nm made up 32% and 7nm processing technology rounded out the remaining 17%.

The company saw a nice boost to its gross margin, which rose 460 basis points sequentially to 57.8%. This was due largely to higher capacity utilization rates, which speaks to the demand for TSMC's services.

TSMC forecast Q4 revenue to fall between $26.1 billion and $26.9 billion, representing 35% year-over-year growth and 13% growth sequentially (at the midpoint). It is expecting a gross margin of 57% to 59%.

When asked about its pricing and expanding gross margin, the company said it needs a high gross margin given how capital intensive its business is. As long as customers are doing well, it can continue to increase prices. TSMC also said it is not interested in acquiring the foundry businesses of Intel or Samsung.

Image source: Getty Images.

Is it too late to buy the stock?

This was another great quarter with revenue and profits continuing to surge. The company looks poised to continue to ride the AI boom with every major player working with it to make their chips and expand production.

While the company danced around the question of pricing, all indications point to healthy price increases next year. In addition, the company can continue to push its gross margin higher over the long run as a result of increasing capacity utilization, strong pricing, and improved scale with its newest 3nm technology, which is still ramping up.

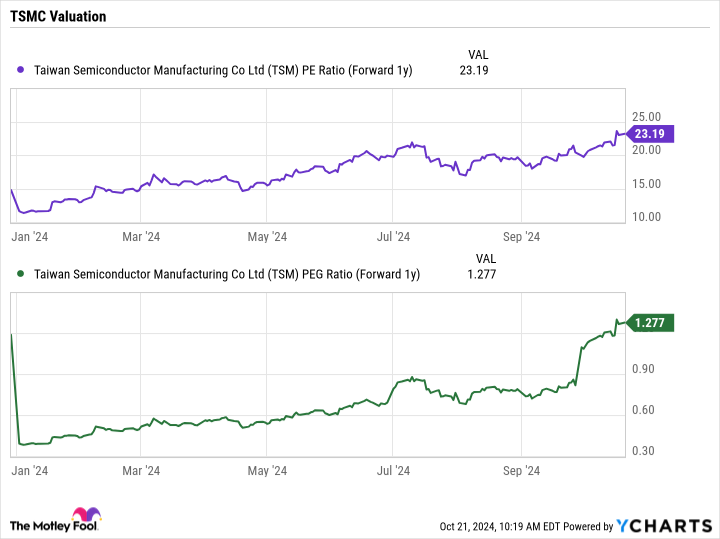

After its jump in price, TSMC stock now trades at a forward price-to-earnings (P/E) ratio of 23 based on analysts' 2025 estimates. It has a price/earnings-to-growth ratio (PEG) about 1.3. A PEG under 1 is generally considered undervalued, but growth stocks often have PEGs well above that level. TSMC's valuation is still attractive given the opportunity in front of it, and analysts' outlooks could be on the rise following its strong report.

Data by YCharts.

Overall, TSMC is one of the best positioned stocks to capitalize on the AI infrastructure buildout, as well as any increased demand for more powerful end products, such as smartphones and personal computers (PCs), needed to run AI applications. The company counts all the major players in the space as customers and has created a huge lead over its competition in terms of technology.

As such, while its valuation and share price continue to rise, it's not too late to buy the stock at current levels. TSMC has the makings of a long-term winner.