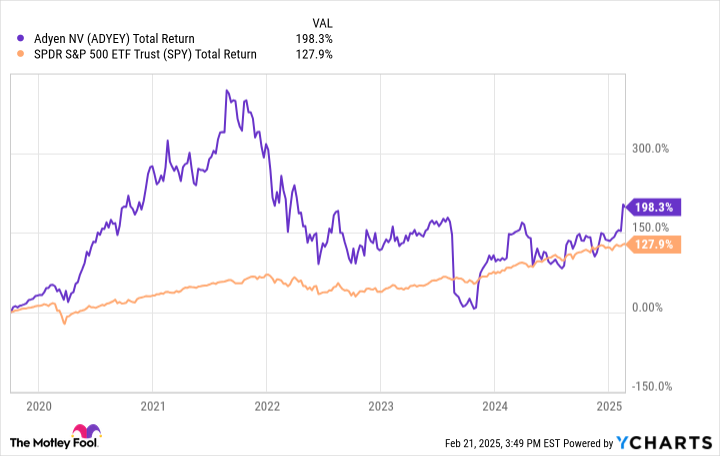

Few European stocks have outperformed their American counterparts over the last five years. Adyen (ADYE.Y +0.09%) is one of these select few. Shares of the Dutch company have beaten the S&P 500 since it went public over five years ago.

That's due to its rapid market share gains in the payments processing business around the world. With a modern solution built from the ground up for 21st-century digital tools, Adyen is able to offer a superior value proposition compared to legacy solutions, which is why it now processes over $1 trillion in payment volume a year.

Now, let's turn to the future. Is there more growth left for this European payments giant? Where will Adyen stock be in five years? Let's take a closer look and find out.

Strong growth at scale

In 2024, Adyen processed $1.33 trillion in payments around the globe. This includes online sales, point-of-sale solutions, and its platform solution for omnichannel merchants and mobile applications. Essentially, if a business wants to process payments digitally, Adyen aims to have whatever solution it wants. This means at any place your customers may want to purchase an item, or with whatever local payment method they prefer. For example, Adyen recently made a direct integration with the popular payments network in Brazil called Pix.

Even though Adyen is already at such a large scale, its growth in payment volume actually accelerated last year. Total payment volume grew 33.7% year over year in 2024 on top of 29.1% growth in 2023 (in U.S. dollar terms). Growth in the second half of 2024 slowed to 22% year over year, but that was due to the ending of a large contract that generated minimal net revenue for Adyen. Excluding this customer, volume grew 28% year over year.

Since Adyen takes a percentage fee on all the money it processes, when volume grows, revenue grows. Adyen's revenue was up 22% year over year in the second half of 2024, with EBITDA (earnings before interest, taxes, depreciation, and amortization) margin of 53%. Adyen is guiding for revenue to grow at least 20% year over year through 2026, which means the next two years.

OTC: ADYE.Y

Key Data Points

A lesson in reinforcing competitive advantages

Large businesses have adopted Adyen's solutions because they are superior to legacy players'. Why? It's simple. Adyen has built a modern payments solution from the ground up that works at a much higher rate than older solutions that are often "duct-taped"-together acquisitions. In fact, Adyen has a rule that it never makes acquisitions, given how hard it is to integrate payments processors together.

Its customers -- such as Spotify and Booking Holdings -- demand almost constant uptime, high payment acceptance rates, and a slew of payment options in hundreds of countries worldwide. Since its founding, Adyen has worked tirelessly to improve on its product, and it now has arguably the best solution out there. This is a reinforcing competitive advantage. As Adyen gets bigger, it can offer better rates to its customers while simultaneously increasing its value proposition versus any upstart competitor. When stealing market share from legacy players, it can simply tell these customers that its solutions work much better (which they do).

This is an enviable position to be in. With the company now processing over $1 trillion in payments a year and generating over $2 billion in net revenue, it can now step on the accelerator and further separate itself from the competition. It is hard to see why these large customers such as Spotify would leave Adyen anytime soon.

ADYEY Total Return Level data by YCharts.

Where will Adyen stock be in five years?

There are multiple tailwinds that can help Adyen keep growing its revenue at 20% year over year and at a double-digit annual rate over the long run. First, there is plenty of the market left to go after and steal share from. It processes $1.33 trillion in annual volume, which may seem large, but is still a small fraction of the overall digital payments pool.

For example, Visa -- the largest credit card network in the world -- processes $16 trillion a year. This is only one of the many payment options Adyen offers for its customers. Global gross domestic product is over $100 trillion.

On top of this, there is still a slow transition around the globe from physical cash to digital payments. This should lift Adyen's business in the coming years. Lastly, Adyen benefits from inflation, which will help grow its payment volumes year after year. If its customers raise prices, a percentage of that will flow to Adyen. It is truly a beautiful business model. Add it all together, and I think it is reasonable for Adyen to expect revenue to grow at a 20% rate in the near future.

But what does that mean for the stock? Adyen's trailing revenue is $2.2 billion. If the company can double this figure over the next five years, revenue will grow to $4.4 billion. With a 55% projected EBITDA margin, that is about $2.4 billion in annual earnings five years from now. Today, Adyen has a market capitalization of $60 billion, giving it a five-year forward price-to-earnings ratio (P/E) of 25, which is not cheap.

So, despite the attractiveness of this business, Adyen stock -- at least, at current levels -- does not look like a bargain right now and will likely underperform over the next five years.