Meta Platforms (META +10.21%) rose over 11% on July 31 thanks to the incredible results that it posted during the second quarter. Meta also delivered some shocking news that helped propel the stock higher, as its expected growth is far greater than anyone predicted.

But after a large jump in a short time frame, is the stock still worth buying?

Image source: Getty Images.

Q2's growth far exceeded management's expectations

Meta Platforms is better known for the social media platforms that it owns: Facebook, Instagram, Threads, WhatsApp, and Messenger. The key part of these apps is the advertising revenue that they generate. In Q2, advertising generated $46.6 billion in revenue for Meta. Companywide, Meta generated $47.5 billion.

That's nearly all of Meta's revenue, so it's clear that as long as advertising remains strong, Meta will remain strong. In Q2, ad revenue rose 22% year over year. Because the revenue makes up a large chunk of Meta's total, this 22% growth rate is equal to its overall growth rate. The big kicker here is that Meta was only expecting 13% revenue growth at the midpoint for Q2.

NASDAQ: META

Key Data Points

Q2 clearly exceeded all expectations for growth, which is one of the reasons why the stock responded so positively; the other reason was the outlook.

Meta expects to sustain this growth through at least the next quarter

Looking ahead to Q3, Wall Street analysts expected Meta to forecast $46.2 billion in revenue. However, management completely blew that expectation away, guiding for revenue between $47.5 billion and $50 billion. That indicates 20% growth at the midpoint, which shows that this rapid growth is expected to persist.

That's an incredible outlook for Meta and shows that the company isn't just succeeding, it's knocking it out of the park. However, the 11% jump following Q2 earnings may concern investors that all of this success has been pulled forward. So, is Meta a solid buy now?

Meta's stock isn't the cheapest around

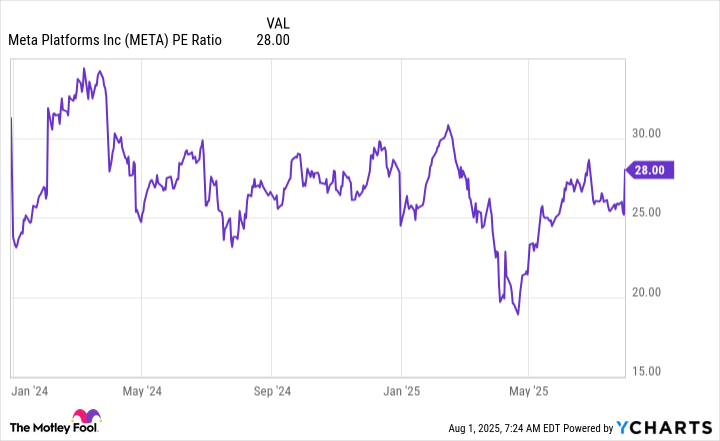

After the one-day jump, Meta trades at 28 times earnings.

META PE Ratio data by YCharts

Besides the decline Meta experienced alongside the broader market in April, this is pretty much in line with where the stock has traded at since 2024. As a result, investors shouldn't be overly concerned with the price that they're paying. Furthermore, the S&P 500 index (^GSPC 0.55%) trades at 24.9 times trailing earnings, which isn't that much cheaper than Meta (although still historically expensive).

With Meta's impressive growth rate and dominant business model, I'm confident that Meta can still deliver market-beating growth moving forward. The Wall Street analyst community was bearish on Meta's stock heading into earnings, as its forward price-to-earnings (P/E) ratio was identical to its trailing P/E ratio, indicating no earnings growth over the next year.

However, Meta delivered 38% diluted earnings per share (EPS) growth in Q2, so this argument has been completely upended. This could cause a wave of analyst upgrades coming in the next few weeks, which could drive Meta's stock even higher.

The price for Meta's stock is fair, and with excellent growth ahead of it, I still think it's a top stock to buy in the market today.