Over the last few weeks, several big tech companies have reported earnings for the second calendar quarter of 2025. One of the biggest takeaways from behemoth artificial intelligence (AI) developers like Alphabet, Meta Platforms, Microsoft, and Amazon is that investment in infrastructure continues to surge. Collectively, these companies are expected to spend more than $330 billion on AI infrastructure this year alone.

A large portion of this capital is going to data center buildouts, networking equipment, servers, and more chips, of course. At first glance, these secular tailwinds may appear most favorable for GPU designers such as Nvidia and Advanced Micro Devices.

However, rising GPU acquisition ignites demand for other mission-critical services within the broader semiconductor landscape, too.

Let's dig into why Micron Technology (MU 2.47%) also looks well positioned alongside its chip peers to benefit from rising AI infrastructure spend from the hyperscalers.

Is now a good time to scoop up shares of Micron with earnings scheduled for September? Read on to find out.

NASDAQ: MU

Key Data Points

What does Micron do?

Nvidia and AMD design advanced chipsets called GPUs, which serve as the core architectures on which AI models are trained and inferenced. Micron enters the equation through its high-bandwidth memory (HBM) solutions, which essentially help keep GPUs running at optimal speeds and help prevent bottlenecks during data workload processing.

Outside of data centers, Micron's DRAM and NAND products power applications across Internet of Things (IoT) devices such as smartphones and gaming PCs, as well as cloud infrastructure and more industrial applications such as autonomous automotive systems and robotics.

Image source: Getty Images.

How large of an opportunity is high-bandwidth memory?

According to data compiled by Bloomberg Intelligence, the total addressable market for HBM was estimated to be worth $4 billion in 2023. This figure is expected to grow at a 42% compound annual growth rate through 2033, reaching approximately $130 billion by the early 2030s.

Despite this rapid acceleration, the HBM market remains highly concentrated. Only a few companies such as Micron, Samsung, and SK Hynix are producing HBM solutions at global scale. While competition is intense, I see this industry concentration as the foundation of Micron's high strategic market value.

As hyperscalers expand AI capacity, many will seek to diversify their supply chains for different chip components. This makes sense, as big tech does not want to rely solely on a singular vendor in order to ensure steady access to chip supply, lock in favorable pricing, and access broader manufacturing footprints. With its growing HBM capabilities, Micron is well positioned to acquire additional market share in this environment.

Is Micron stock a buy right now?

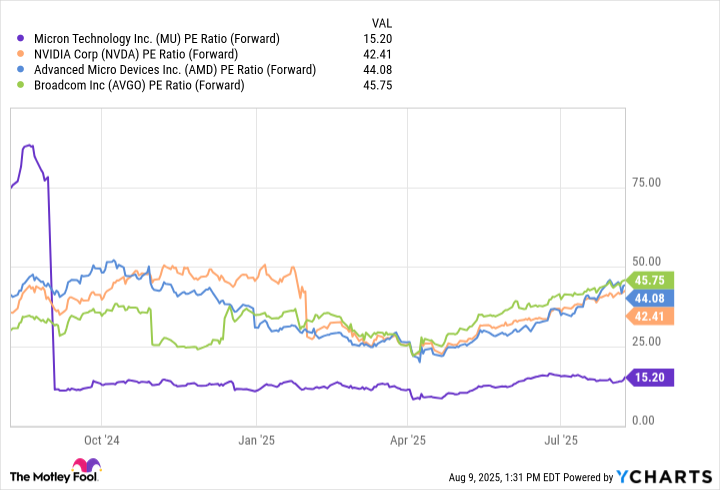

The chart below benchmarks Micron against a small cohort of leading chip stocks on a forward price-to-earnings (P/E) basis.

Data by YCharts.

The obvious thing that sticks out is that Micron's forward P/E experienced notable compression during late 2024. This is due, in part, to the lumpiness in Micron's financial guidance since accurately forecasting demand trends for a still-developing market such as HBM is challenging. Investors tend to shy away from uncertainty, which appears to be weighing on sentiment around Micron at the moment.

The valuation disparity between between Micron and its peers could suggest that investors do not fully understand or appreciate just how important the company's products are to overall AI infrastructure.

Micron's HBM solutions and edge computing products are essential for AI development at scale. As the market begins to connect the dots between Micron's leadership in memory and storage chips to the broader AI narrative, there is significant room for Micron's valuation to expand.

With earnings scheduled for next month and the stock still trading for a steep discount to its peers, Micron looks like a compelling buy right now.