The market has been on quite a run lately, and if you have cash on the sidelines, you may have been somewhat disappointed in the returns compared to what they could have been if the money were invested. However, I believe there are still several promising opportunities available that are worth taking advantage of right now.

If you have $50,000 ready to invest (or any dollar amount, for that matter), I think these are among the best values on the market right now.

Image source: Getty Images.

Alphabet

Alphabet (GOOG 0.80%) (GOOGL 0.80%) is one of the world's most dominant companies, thanks to its Google ecosystem. However, many investors are concerned that Google may lose market share to generative AI. While that's a valid concern, the reality is that generative AI has been around for several years, and Google Search is still the market leader by far. Furthermore, Google has integrated AI search overviews into its search engine, merging generative AI and a traditional search experience.

NASDAQ: GOOGL

Key Data Points

Management noted that this has become an incredibly popular feature, and it can be monetized at the same rate as traditional searches. This all adds up to an investment thesis that Google Search will remain stable over the long term, and its recent results support that. In Q2, Google Search's revenue rose 12% year over year. It was also boosted by strong growth from Google Cloud, which increased revenue by 32% due to robust demand for AI.

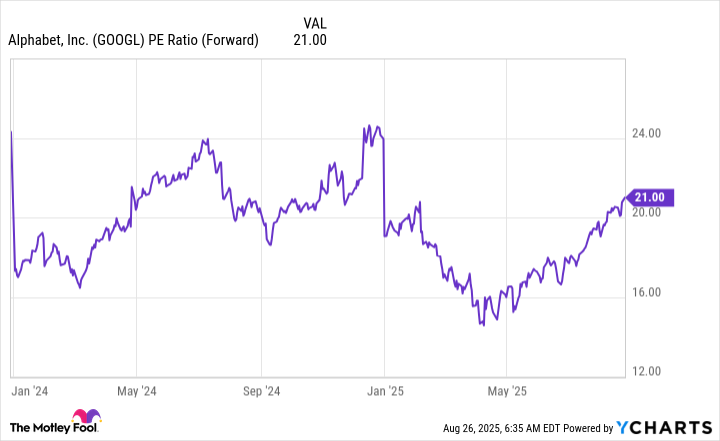

Despite Alphabet's Q2 success, the stock trades at a significant discount to the market and can be purchased at just 21 times forward earnings.

GOOGL PE Ratio (Forward) data by YCharts

Alphabet is one of the biggest bargains in the stock market right now, and investors should consider loading up on shares while it's at a discount.

The Trade Desk

Sticking with companies that generate a significant amount of revenue from advertising, The Trade Desk (TTD 2.03%). The company, which runs an independent digital ad platform, has had an up-and-down year.

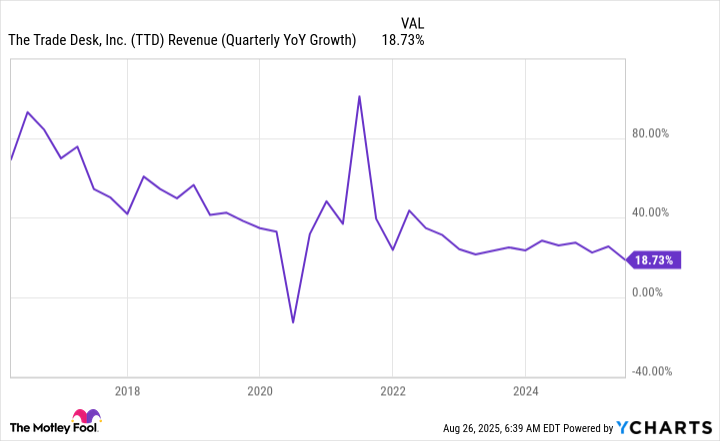

It's working on converting its client base to its new AI-driven platform, and the transition has been far from smooth. This caused The Trade Desk to miss management's guidance for the first time as a public company in last year's fourth quarter. It also forecasts weak growth for Q3 2025, as management only expects 14% growth.

That's the slowest growth rate in the company's history on the public markets outside of one COVID-19-influenced quarter.

TTD Revenue (Quarterly YoY Growth) data by YCharts

As a result, investors panicked and heavily sold off shares. The stock is down over 60% from its highs, but investors are ignoring several key factors. First, Q3 2024 saw heavy political spending, which is acting as an artificial headwind for The Trade Desk's growth rate. Without this, The Trade Desk's growth would have been far greater. Another factor is that we're still in the early ages of connected TV, which is a huge part of The Trade Desk's investment in a long-term growth case.

NASDAQ: TTD

Key Data Points

With The Trade Desk trading for 29 times forward earnings, it's an excellent growth stock to scoop up now while it's trading at a huge discount to its historical levels.

MercadoLibre

Another lesser-known company is MercadoLibre (MELI 1.05%), which is the e-commerce leader in Latin America. MercadoLibre has put up excellent growth year after year, and its latest results are no exception.

NASDAQ: MELI

Key Data Points

In the second quarter, commercial revenue grew 45% while fintech revenue soared 63% on a currency-neutral basis. Currency fluctuations have always been a significant challenge for Latin America, so seeing strong growth after adjusting for these fluctuations is key for investors.

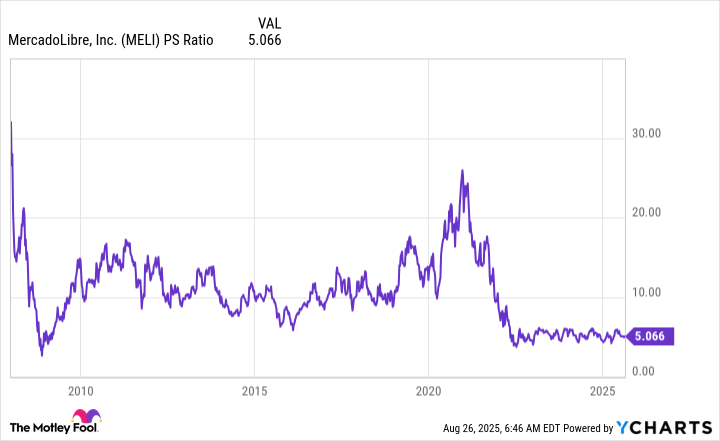

Despite its persistent strong growth, MercadoLibre still trades at the lower end of its valuation range, where it has been for most of the past decade.

MELI PS Ratio data by YCharts

At five times sales, it's valued at nearly half of where it was from 2010 to 2020, and if it could return to that higher valuation threshold, it would result in monster gains for shareholders. Even if it doesn't, there's still significant growth potential remaining in its commerce and fintech platforms in Latin America, making it an excellent stock to buy and hold.