With artificial intelligence (AI) spending at an all-time high and many top CEOs discussing five-year trajectories for that spending to increase by an incredible amount, it's clear that AI remains a promising industry to invest in. Given all of the bullish language surrounding this massive ongoing infrastructure build-out, it's hard to imagine a stock that's not at or near its all-time high, especially for companies that are slated to make massive profits from this build-out.

And yet, ASML Holding (ASML 0.23%) is down by around 25% from its all-time high despite the fact that it's responsible for producing machines that are vital to the manufacturing of all cutting-edge chips. I don't think it will stay this low for long. Indeed, it could provide investors with impressive returns from here over the next five years.

Image source: Getty Images.

ASML holds a rare technological monopoly in its space

Netherlands-based ASML manufactures the lithography machines that lay down microscopic electrical traces on chips. In particular, its extreme ultra-violet (EUV) machines are the only ones that can handle that part of the production process for the most advanced chips. As it's the only company in the world with this technology, every chip foundry must purchase ASML's machines when they're expanding their high-end chip production capacity.

So, whenever you hear about a new chip factory being built somewhere, you can assume that ASML will benefit.

During Nvidia's (NASDAQ: NVDA) fiscal 2026 second-quarter conference call last month, CEO Jensen Huang commented that the company expects global data center capital expenditures to reach $3 trillion to $4 trillion by 2030. A decent portion of this type of spending goes toward outfitting data centers with computing equipment, and anything that has high-end chips in it, whether those are Broadcom (NASDAQ: AVGO) networking switches or Nvidia GPUs, has chips produced using ASML's equipment.

With demand for data centers skyrocketing, chip foundry operators will need to increase production capacity by building new factories, as top businesses like Taiwan Semiconductor Manufacturing (NYSE: TSM) are already doing. This will give a long-term boost to ASML, and its management forecasts solid growth over the next five years.

To be specific, by 2030, ASML management expects its annual revenue to be between 44 billion euros and 60 billion euros. Over the past four reported quarters, ASML has generated 32.2 billion euros, so if it hits the top end of that projected range, its revenue will almost double in the next five years. Historically, ASML's management has been extremely conservative with the guidance it gives. It was cautious with its 2025 outlook, yet it has so far produced phenomenal results. In Q2, revenue rose 23%.

As a result, I won't be surprised if ASML's revenuesin 2030 comes in at the high end of the guidance range. That sales growth over time should help lift the stock, but that's not the only factor that could assist ASML.

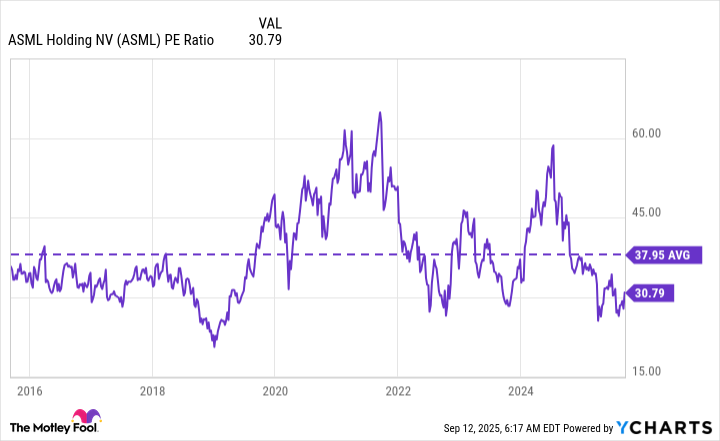

ASML isn't trading at its usual valuation

Over the past decade, ASML has traded at an average of about 38 times trailing earnings. It's cheaper than that right now, so if it rises to its average valuation level, that multiple expansion alone would give shareholders an excellent return.

ASML PE Ratio data by YCharts.

ASML's bottom line generally tracks with its top line. So if its P/E ratio returns to its average level and its 2030 revenue projection comes in at the high end of management's projection, it could be a top growth stock to buy now and hold for the next five years.

The company has several positive tailwinds blowing in its favor, and the AI infrastructure spending spree is chief among them. Because foundry operators need to buy ASML's machines years in advance of when demand is expected to arrive, it's also at a smaller risk of being caught up in a bubble. This makes ASML a great way for investors of all risk tolerances to participate in the AI investment trend.