Nvidia's (NVDA 0.56%) AI dominance has come into question over the past few weeks. OpenAI just announced a monster deal with Advanced Micro Devices (AMD +0.89%), making it seem as if AMD could be catching up to the king of AI investing to date. However, I don't think that's a valid argument, as AMD cut OpenAI an incredible deal that Nvidia likely wasn't willing to make.

Nvidia is still the largest provider of artificial intelligence computing hardware by far, and I think we'll get some news on Oct. 16 regarding the strength of the demand for AI computing hardware. That's when Taiwan Semiconductor Manufacturing (TSM +0.61%) reports its quarterly earnings, and it will give investors a hint as to the strength of the demand for chips.

This could cause all AI hardware-related stocks to respond positively if TSMC reports great results, making Nvidia an intriguing stock to buy before Oct. 16.

Image source: Nvidia.

Strong AI demand can power Nvidia's stock higher over the next few years

One thing investors must keep in mind is that Taiwan Semiconductor is the world's leading chip manufacturer and is also the chipmaker for both Nvidia and AMD. So, just because TSMC reports strong numbers, it doesn't necessarily mean that Nvidia is still doing well. However, with Nvidia being a much larger customer than AMD, I think it will be safe to say that if TSMC is doing well, Nvidia is too.

We won't know for sure how Nvidia's third quarter went until sometime in November, but there are still signs of Nvidia's dominance everywhere. Many of the cloud computing companies are racing to build out data center capacity to meet the demands of their customers.

Nvidia's graphics processing units (GPUs) are best in class at high-powered general-purpose computing, and continue to be a top choice for many AI developers. Rising competition from custom AI accelerator chips from Broadcom could challenge Nvidia's leadership in the future, but for now, Nvidia is still the most prevalent computing hardware being used.

Regardless of which computing chip is favored by the AI hyperscalers at the time, AI capital expenditures are expected to increase dramatically over the next few years. This year, Nvidia expects total AI data center capital expenditures to reach $600 billion. That figure is expected to rise to $3 trillion to $4 trillion by 2030.

That's massive spending expansion, and will benefit all companies in the AI industry. With Nvidia being the largest market share leader by far, it will benefit the most, making the stock an intriguing buy right now.

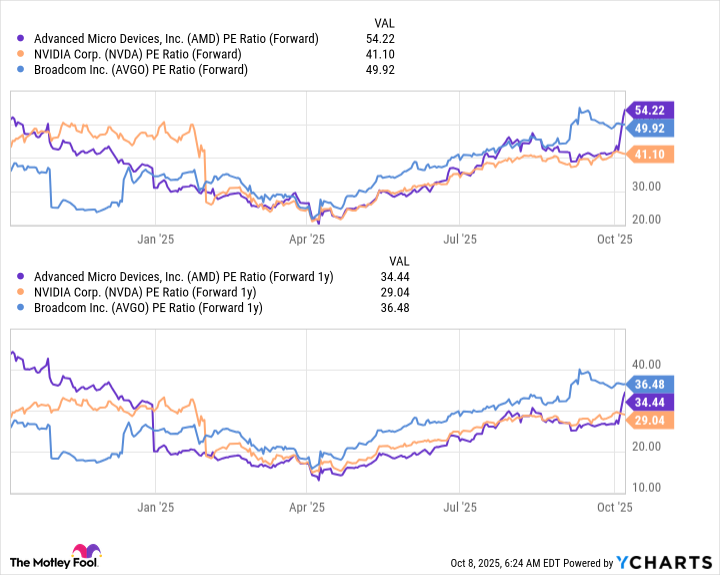

Nvidia's stock isn't as expensive as that of its competitors

Both Broadcom and AMD's stock have popped on news of chip deals with OpenAI; however, this pop has caused them to get far more expensive than Nvidia. When various forward price-to-earnings (P/E) metrics are examined, Nvidia still trades at a discount to its peers despite much better results.

AMD PE Ratio (Forward) data by YCharts

Both AMD and Broadcom have increased on news of a handful of sales; meanwhile, Nvidia is generating far more revenue each quarter than each of these announcements. Broadcom's deal with OpenAI had a value of $10 billion. AMD's deal has the potential to be worth up to 10% of the value of the company, or about $34 billion. During Nvidia's fiscal 2026 second quarter (ended July 27), its data center division alone generated $41.1 billion.

This shows that Nvidia is far larger than both of these long-term deals, and investors have no reason to panic. In fact, with massive AI demand on the horizon and Nvidia's discount to its peers, it could be considered an excellent long-term investment right now.

Strong language from TSMC on Oct. 16 about the long-term robustness of chip demand could be all Nvidia needs to see its stock soar, and I think scooping up shares before this event would be a wise move by investors.