With thousands of publicly traded companies and exchange-traded funds (ETFs) to choose from, Wall Street provides investors with no shortage of ways to grow their wealth. But among the many paths investors can take, few have proved more successful than buying and holding high-quality dividend stocks.

Just how good are dividend stocks? In The Power of Dividends: Past, Present, and Future, the researchers at Hartford Funds, in collaboration with Ned Davis Research, compared the performance of dividend stocks to non-payers over a 51-year period (1973-2024). What they found was a milewide difference in performance -- a 9.21% average annual return for dividend stocks vs. a 4.3% average annual return for non-payers.

Their analysis also showed that income stocks are considerably less volatile than the benchmark S&P 500.

Image source: Getty Images.

In other words, it's not a matter of whether or not dividend stocks make for a smart investment. It's simply deciding which income stocks can help you reach your investment goals.

Out of the 36 combined stocks and ETFs in my investment portfolio, as of the closing bell on Oct. 13, nearly half (17) were paying a dividend. One, however, has stood out as a can't-miss value amid a historically pricey stock market. Investors, say hello to the little-known, 14%-yielding, monthly dividend stock that I more than doubled my stake in recently: PennantPark Floating Rate Capital (PFLT +0.47%).

Business development companies have come under pressure

PennantPark is what's known as a business development company (BDC). BDCs are companies that invest in generally unproven small- and micro-cap businesses, known more commonly as "middle-market companies."

Recently, publicly traded BDCs have taken it on the chin, with some Wall Street analysts expecting them to pare back their supercharged dividend payouts. While fingers can't be pointed at any one specific issue, there are a number of factors that threaten to weigh on BDCs like PennantPark.

NYSE: PFLT

Key Data Points

For starters, there's the unpredictability that comes with President Donald Trump's tariff and trade policy. Though tariffs aren't directly applicable to BDCs, they can impact the unproven businesses that BDCs have invested in. If these uncertainties lead to trouble for small- and micro-cap businesses, it can have a ripple effect for BDCs, which invest in and/or lend to middle-market companies.

To build on this point, there are concerns that the U.S. might dip into a recession in the coming quarters. While the start of recessions can't be predicted with any accuracy, history tells us they're a normal and inevitable aspect of the economic cycle. The unproven companies BDCs invest in are prone to struggle during economic downturns.

But perhaps the biggest concern for BDCs, including PennantPark Floating Rate Capital, is the Federal Reserve's monetary policy. BDCs commonly use variable-rate loans, which means every rate cut by the nation's central bank will reduce the income they're able to net on their loan portfolios. With the Fed clearly in a rate-easing cycle, there's the threat of shrinking profits for BDCs in the coming quarters.

Yet in spite of these headwinds, I more than doubled my existing stake in PennantPark last week for a number of well-defined reasons.

Image source: Getty Images.

PennantPark might be the safest double-digit-yielding stock on the planet

While the high-octane dividend yields are what typically attract investors to BDCs in the first place, it's important to dig beneath the surface and discover what makes these companies tick.

PennantPark closed out its fiscal third quarter (June 30) with just a shade over $2.4 billion in its investment portfolio, consisting of around $240 million in common and preferred equity, and approximately $2.16 billion in its loan portfolio. This makes it a predominantly debt-focused BDC.

Despite the risks of investing in early stage/unproven companies, there are also rewards for BDCs. Since middle-market companies often have limited access to traditional banking and credit solutions, the financing they do receive from the likes of PennantPark tends to be at an above-market rate.

Think about this for a moment: Whereas Treasury bonds have been dishing out yields ranging from 4% to 5%, PennantPark closed out the June quarter with a weighted-average yield on debt investments of 10.4%!

However, the real advantage for PennantPark Floating Rate Capital can be seen its full name. Approximately 99% of its $2.16 billion loan portfolio sports variable rates. While the Fed being in a rate-easing cycle isn't a positive for BDCs, the nation's central bank is making slow, well-telegraphed moves. Since the Fed began hiking rates in March 2022, PennantPark's weighted-average yield on debt investments has expanded by 300 basis points.

Beyond these yield advantages, the company's management team has done an exceptional job of protecting invested principal. Including equity investments, its $2.4 billion is spread across 155 companies, equating to an average investment size of $12.6 million. This means no single investment is imperative to PennantPark's success or capable of rocking the boat.

Furthermore, all but $12.5 million of its $2.16 billion loan portfolio is first-lien secured debt. First-lien debtholders are at the front of the line for recovery in the unlikely event that a borrower files for bankruptcy protection.

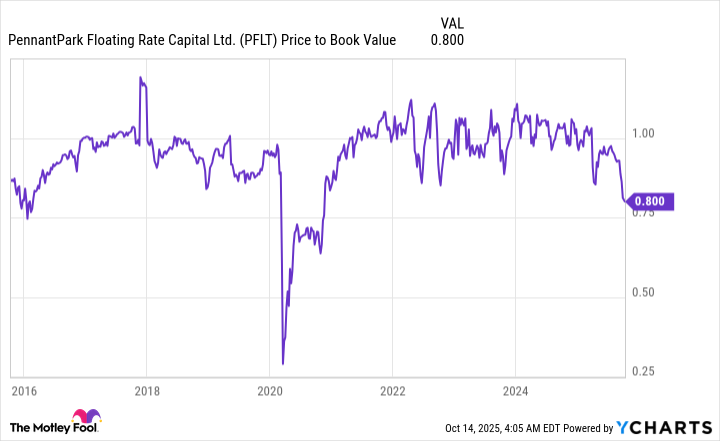

PFLT Price to Book Value data by YCharts.

The final piece of the puzzle that enticed me to more than double my stake in PennantPark Floating Rate Capital is its valuation.

BDCs typically trade within close proximity of their reported book value. Based on PennantPark's net asset value of $10.96 per share (as of June 30), its closing price on Oct. 13 represents a 20% discount to its book value. Discounts of this magnitude don't stick around for long -- especially for a company with a sustainable monthly dividend.