Microsoft (MSFT +1.11%) is currently locked in a battle with Apple (AAPL +0.11%) to be the world's second-largest company. However, with results like the ones Microsoft just announced, Apple is clearly outclassed. Microsoft just announced some incredible results and put on a clinic for investors, but chief among its announcements was its $392 billion backlog in cloud computing.

A metric like that makes it clear that we're just in the beginning days of the artificial intelligence megatrend, and if you think that 2025 will be the end, you're mistaken. Microsoft's stock still has a ton of room to run, and if it can convert on its backlog, it will become one of the largest cash cows in the world.

Image source: Microsoft.

Azure is putting up incredible growth

At the core of Microsoft's cloud computing strategy is its cloud platform, Azure. Azure has become the building block for aspiring AI companies across the world, and Microsoft is scrambling to build out computing capacity to meet its massive backlog, which rose 51% year over year to $392 billion in its fiscal 2026's first quarter (ended Sept. 30). Azure delivered 40% revenue growth during Q1, which indicates a mismatch between backlog and actual growth.

At face value, this is a good thing. Microsoft Azure essentially cannot build out its computing capacity fast enough to convert this backlog. While these two numbers aren't that far apart, if we see the backlog rise at an even faster rate, some of the clients may become disgruntled and move to a different cloud platform. However, I think this mismatch is fairly healthy, as Microsoft also doesn't want to overbuild either.

Microsoft is sitting on a gold mine of future AI spending, and it will drive strong growth for years to come. But Microsoft isn't just Azure; it has other business segments as well that drive its results. The rest of Microsoft's divisions were a bit of a mixed bag, making its blowout quarter all the more impressive.

NASDAQ: MSFT

Key Data Points

Microsoft is doing quite well overall

In Q1, its Productivity and Business Processes business (which includes products like Microsoft 365, LinkedIn, and Microsoft Dynamics) saw revenue rise 17% year over year to $33 billion. That's larger than Intelligent Cloud's $30.9 billion run rate, although that division increased at a 28% year-over-year pace. This division is normally a pretty good indicator of economic growth, as it's tied to user licenses for base Office products. But it can also include subscriptions to platforms like Copilot, which integrates generative AI into everyday workflows.

On the downside, its More Personal Computing business only saw revenue growth of 4%, stemming from low OEM device sales and poor Xbox performance. This is a much smaller division, only contributing $13.8 billion to the total, so its poor performance didn't weigh on Microsoft's overall results too much.

All in all, Q1 was an excellent quarter for Microsoft, and it gave investors a lot to cheer for. It's hard to complain about a $4 trillion company growing revenue 18% year over year to $77.7 billion with diluted earnings per share (EPS) increasing 13% year over year.

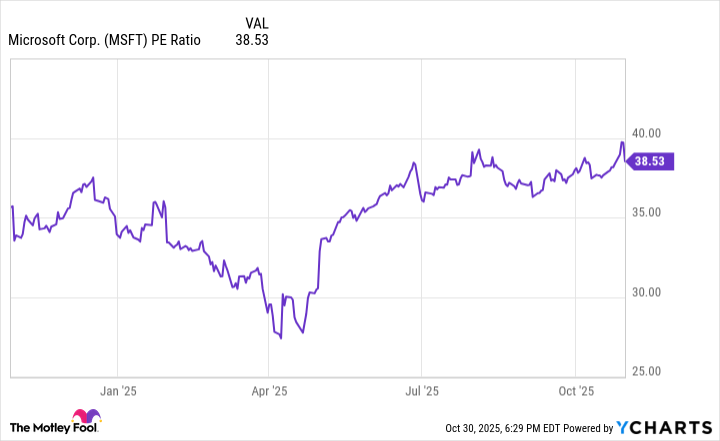

Microsoft proved its worth with the premium price tag, but is it too much? Following earnings, Microsoft's stock now trades for 39 times earnings, which is a much greater premium than its peers.

MSFT PE Ratio data by YCharts

For example, take Alphabet. It trades for 30 times earnings, and posted similar results to Microsoft, with revenue rising 16% (compared to Microsoft's 18%) and diluted EPS rising 35% (compared to Microsoft's 13%).

However, investors are more focused on cloud computing, as it's part of the backbone of the AI boom. With Google Cloud's revenue rising 34% compared to Azure's 40%, the market tends to favor Microsoft more. But, as an investor, you can choose which one of these stocks you'd rather own (or buy both).

Each is posting excellent results and is worth buying, but with Microsoft's far more expensive price tag, I'd rather own Alphabet.