For many investors, earnings season represents the pinnacle of each quarter. It marks the six-week period when a majority of S&P 500 companies lift the proverbial hood on their operating results, providing a barometer for Wall Street and investors to gauge the health of corporate America.

But a strong argument can be made that Form 13Fs filed with the Securities and Exchange Commission are just as valuable for investors.

A 13F is required to be filed no later than 45 calendar days following the end of a quarter for institutional investors overseeing $100 million or more in assets under management. It provides a clear portfolio snapshot that investors can use to determine which stocks, exchange-traded funds (ETFs), and select options Wall Street's smartest money managers bought and sold in the latest quarter.

Nov. 14 marked the 45-day filing deadline for 13Fs covering third-quarter trading activity.

Image source: Getty Images.

Although Warren Buffett is the most closely tracked of all billionaire asset managers, he's far from the only billionaire known to generate outsize returns. Billionaire venture capitalist Peter Thiel, the co-founder of PayPal Holdings and Palantir Technologies, as well as an early investor in Facebook (now Meta Platforms), has an impressive track record of spotting game-changing businesses.

What's particularly noteworthy is that Thiel was a seller of equities during the third quarter. The 13F filed by his fund, Thiel Macro, shows three stocks were pared down or sold in their entirety -- none of which is more prominent than the face of the artificial intelligence (AI) revolution, Nvidia (NVDA +2.92%).

Profit-taking is a logical reason to sell -- but may not be the only reason

Thiel's fund initially took a 246,893-share stake in Nvidia during the fourth quarter of 2024. Subsequent 13F filings show an additional 111,162 shares were added during the March-ended quarter, along with 179,687 more shares during the quarter ended in June. By the midpoint of 2025, Thiel Macro held 537,742 shares of Nvidia.

Thiel's purchases during the first and second quarters may coincide with the short-lived but steep sell-off Wall Street experienced during the latter half of March and early April. The unveiling of President Donald Trump's tariff and trade policy briefly spooked investors, providing a brief opportunity for investors like Thiel to scoop up shares of Nvidia below $100.

NASDAQ: NVDA

Key Data Points

However, Thiel's fund unloaded the entire position (537,742 shares) during the September-ended quarter. Had this stake been held in its entirety, it would have been worth approximately $100 million on Sept. 30.

The most logical explanation for selling Nvidia stock is to lock in profits. Thiel Macro historically holds positions in just a handful of publicly traded companies, with hold times that are often less than a year. In other words, Thiel has demonstrated a willingness to, at times, trade rather than invest, and isn't shy about locking in profits when the opportunity presents itself.

Nvidia's seemingly insurmountable market share lead in AI-data center graphics processing units (GPUs), coupled with the compute advantages of its AI hardware, has helped lift its stock to the top of the pedestal on Wall Street. But there may be more to Thiel's abrupt exit from Nvidia stock than just benign profit-taking.

Image source: Nvidia.

Headwinds are mounting for the face of the artificial intelligence revolution

While there's no denying that Nvidia's AI hardware can serve as the foundation for the long-term transformation of corporate America, there are several reasons to believe the near-parabolic ascent of its stock isn't sustainable -- and Peter Thiel likely knows it.

Although history has proved kind to some game-changing innovations, such as the internet, over long periods, it has been no friend to early stage hyped trends. Since the advent and proliferation of the internet three decades ago, every next-big-thing technology and trend has eventually navigated its way through a bubble-bursting event.

Yes, we're witnessing some impressive demand for AI infrastructure at the moment. Nevertheless, most businesses aren't anywhere close to optimizing AI as a technology, and many aren't generating a positive return on their AI investments. These are hallmarks that suggest the AI bubble is going to burst at some point. If and when that happens, arguably no company would take a more direct hit than Nvidia.

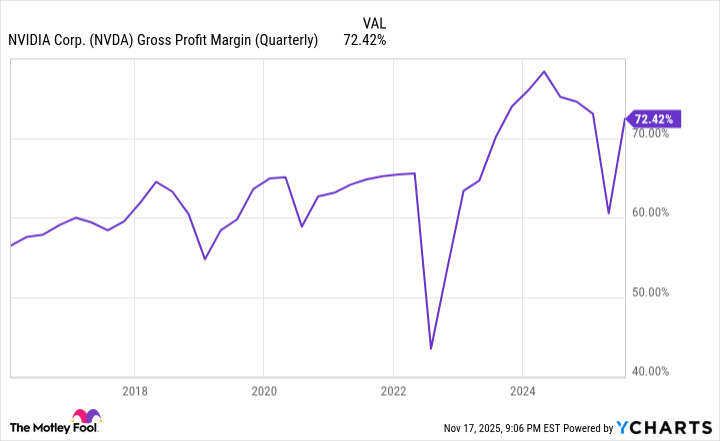

There's also the high likelihood that Nvidia will lose some of its competitive edge over time. Nvidia CEO Jensen Huang's plan to release a new advanced AI chip annually can ensure his company stays on top when it comes to compute abilities. However, the lower price points of rival AI-GPUs, coupled with a ramp-up in production from these external competitors, will work against the AI-GPU scarcity that's pumped up Nvidia's pricing power and gross margin.

Nvidia's gross margin is at risk of deflating as competitive pressures build. NVDA Gross Profit Margin (Quarterly) data by YCharts.

To add to the above, internal competition can be problematic for Nvidia. Many of its top customers by net sales (think members of the "Magnificent Seven") are internally developing GPUs for their data centers. Even though these chips can't match Nvidia's hardware on a compute basis, they're notably cheaper and not backlogged. There's a real possibility that these internally developed GPUs will occupy valuable data center space, delay upgrade cycles, and minimize the AI-GPU scarcity that helped lift Nvidia's gross margin above 70%.

Historical valuation concerns may have come into play for Thiel, as well. History has shown that companies leading the charge with next-big-thing trends typically reach their peak with price-to-sales (P/S) ratios of 30 or higher. Since the dot-com bubble burst, a P/S ratio range of 30 to 40 has served as a loose marker of when one or more industry-leading companies have reached bubble territory.

In early November, Nvidia's P/S ratio crested 30, which history makes clear isn't a sustainable valuation premium over an extended period.

Furthermore, the stock market is historically pricey. In late October, the S&P 500's Shiller Price-to-Earnings (P/E) Ratio topped a multiple of 41, which marks the second-highest reading during a continuous bull market when back-tested to 1871. Previous Shiller P/E multiples above 30 have eventually been followed by declines of 20% or greater in the benchmark index.

When the next bear market occurs, companies with premium valuations, such as Nvidia, may feel a disproportionate amount of the pain.